That means the average person spends $54.63 eating out a week or $218.52 a month on just eating out. Unless you have a side-hustle that makes you lots of money. The obvious answer is to eat in!

What About Eating In?

Most people think they can easily quit dining out, and start cooking delicious meals. Here’s the thing with cooking for yourself, the movies get it wrong.

It’s not always a romantic and soothing experience.

Often times it’s a “Crap, I need to eat. What should I cook?” experience that you pray to the food gods you have the right ingredients in your fridge and clean dishes.

Let’s face it, we are busy in our lives and don’t have the time to visit the store every day buying fresh ingredients for a new recipe we found on the internet.

In fact, according to the Harvard Business Review, researcher Eddie Yoon over two decades collected data as consultants for consumer packaged goods companies. He found that:

15% of people say they LOVE to cook

50% of people say they HATE to cook

35% of people say they are ambivalent about cooking (mixed feelings)

If you’re one of the people that hate cooking, you should create a meal plan to make it as easy as possible.

Plan a week in advance what you’re going to eat for each meal and know how to cook it. This way you’ll have the ingredients and can plan accordingly for time.

However, not all plans work out.

Introduce The Peanut Butter and Jelly Theory

When meal plans fail, let me introduce Peanut Butter and Jelly sandwiches, otherwise known as a PBJ.

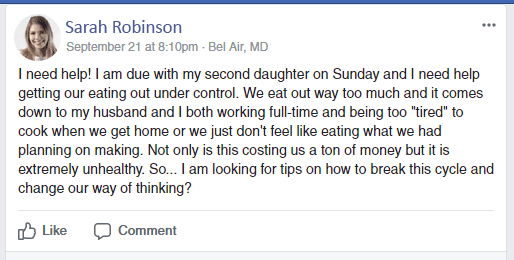

Let me first admit that I have an addiction to commenting on Finance forums, Facebook Groups, and Blogs. The mechanics of building wealth are simple and I’m always happy to remind people that things are often more simple than they appear. Like how I responded to this comment and created “The Peanut Butter and Jelly Theory”.

I get it, you want to start saving money on food and you’re looking for suggestions from the personal finance community to help.

Answers ranged from getting a crockpot to make meals simple, cooking large meals on Sunday and eating leftovers throughout the week, to buying frozen meals that may not be great for you, but easy to prepare.

All of the responses skirted around the idea that a solid weekly meal plan is the best option to help you save money on food. However, sometimes these meals don’t work out for a number of reasons, and once you fall off the wagon, you can end up at the local McDonalds.

So I introduced the Peanut Butter and Jelly Theory. The cost-effective, quickest meal ever to keep your budget on track.

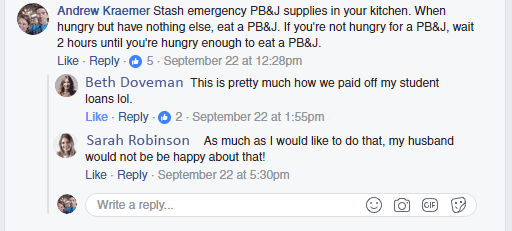

This is easily the most actionable thing you can do to start immediately saving on your food budget. In many cases when people eat out, it’s due to convenience because they don’t have anything at home to sound appealing. That’s when the Peanut Butter and Jelly Theory comes in handy.

“Stash emergency PBJ&J supplies in your kitchen. When hungry, but have nothing else. You can have a PBJ. If you’re not hungry for a PB&J, wait 2 hours until you’re hungry enough to eat a PB&J.”

Sometimes a PBJ isn’t exactly what you’re craving and your favorite restaurant sounds better, or your family would not be happy about that. Well suck it up, you’ll soon be out of debt and you can buy your family a jet ski. Everyone loves a jet ski.

Try the Peanut Butter and Jelly Theory

If you want to save THOUSANDS on food budgets, you should try the Peanut Butter and Jelly Theory! Meals cost less than $1 to make, you’ll save time and money. Most importantly, you’ll have a secret stash of PBJs to make and everyone is a stack of cash saved from eating out!

You’re welcome.

Disclaimer: Wallet Squirrel did not invent the Peanut Butter and Jelly sandwich, just an advocate of saving money. Wallet Squirrel was not sponsored by big PBJ corporations to promote their superior and delicious product.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Let me preface that I used to be a waiter so I understand the value of tipping, but as a customer, tipping is the worst! It’s psychological warfare at the end of every meal that results in either anxiety that you haven’t paid enough or havoc on your wallet for paying too much.

Then exactly how much too much and too little for a tip? Common restaurant adequate says a tip should be 15%-20% pretax, but then why does every restaurant leave the anxiety for the customer to decide how much to tip?

Let’s face it, an extra 20% of a $60 check is still a lot on your budget. That’s $12 the menu doesn’t mention.

This History of Tipping is Murky

From what I found in the Business Insider and Washington Post (and it’s a murky origin story) tipping originated around 17th century England where the word T.I.P. meant “To Insure Promptitude”. The upper class provided extra “allowance” to servers (lower class) to be given faster service.

This practice made its way to America after the Civil War when wealthy Americans started traveling back and forth to Europe. So we can blame them, and I do.

Tipping Today Just Allows Restaurants to Pay it’s Servers Poorly

Because servers receive tips, the federal tipped minimum wage for tipped workers is as little as $2.13 an hour because they receive tips to supplement the difference (source).

That’s kind of ridiculous, right! Restaurants are allowed to only pay their servers $2.13 an hour and expect servers to get the rest of their income from tips. So when you pay your bill, you’re essentially paying for the food/environment with your bill and your tip pays the waiter’s salary.

If you’re a waiter, the customer is actually your boss since they’re the ones that pay you. So every day, every hour, you have a different boss. Yikes.

How Much Do You Pay Your Server Then?

According to Google, yes I googled “How Much Should I Tip”. You should be paying your server 15%-20% of your pre-tax bill.

This Is Where The Anxiety Starts

Which one is it? Do I tip 15% or 20%?

What If The Server Was Bad?

If my bill is $100, does the server get an extra $20 just because they took my order and walked food back from the kitchen?

What if they were awful? We’ve all had bad servers who ignored us. They took a long time or brought us the wrong items with a rude attitude. Is that when you tip them 15% instead of 20%?

What about if the food was awesome but the service was terrible? ugh

Should I feel both angry at my server for bad service but feel guilty since they’re paid so poorly? How should I feel?

I recall a study conducted found that bad servers still received 15%-20% regardless of how good the service was because people felt it was the socially acceptable thing to do. No one wants to be a bad tipper, but should I tip poorly to save a bit of money and prove a point to the server? Would a bad tip even make a difference?

What if the server was awesome?

You plan to spend a certain amount of money eating out and even account for a 20% tip. Do you exceed your budget further if your server was fantastic? Should your server’s awesomeness impact your planned budget? Should they be worthy of more than a 20% tip of that you’re still paying off student loans?

Damn it Janet, you were so great that now my tip for you exceeds my monthly food budget.

Are you a bad person if you don’t acknowledge their above and beyond service or will they quit trying harder if people don’t tip more for the great service?

What About Tipping During Group Meals?

Now imagine eating out with a group of friends, each pays their own bills and it always ends with everyone deciding the tip for themselves. All while each of you judges each other’s tips. If you only tipped 15%, does that make you a jerk if everyone else tipped 20% – 25%?

On the other hand, are you a jerk for tipping more than everyone? Are you considered flaunting your money because you can spend more money than everyone else or does it make you more generous or charitable?

This Is Why I Hate Tipping!

Why does a nice meal out with friends have to end with awkward silences while everyone calculates percentages in their heads while they secretly judge the performance of the server? Ending in silent comparison of who tipped more, who was more generous, and who felt more charitable than the rest of the group.

I Now Tip 20% Regardless of Service

Tipping makes me so anxious that I’m just starting to tip 20% regardless of service (paying with my credit card). The server can refill my drink at the perfect time or pour hot soup on my head. Creating a baseline 20% tip in every situation saves me from unnecessary anxiety at the cost of a few extra dollars from my budget. Sorry budget.

Except Subway “Sandwich Artists”, I still don’t understand why they now have a tip jar. They literally walk along with me placing ingredients I select onto bread. Is tipping at fast food restaurants now becoming a thing?

If you also tip 20% regularly, here is a chart to help you decide what 20% would be when you’re looking over a menu because they don’t list the extra tipping cost on the menu.

20% Tip Per Cost of your meal

Check

20% Tip

$20

$4

$40

$8

$50

$10

$60

$12

$70

$14

$80

$16

$90

$18

$100

$20

If this seems like a lot of money to tip, you can always stay in and eat a Peanut Butter and Jelly sandwich. Save eating out when you know you can spend extra money on a 20% tip.

What do you tip your servers? There is obviously no right answer otherwise they wouldn’t leave the tip field on every check blank. I REALLY want to know. Do you judge your waiter every service or, like me, give them a flat fee regardless?

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

We are regularly becoming a cashless society with credit cards and digital transactions becoming the primary forms of money transfer. Even mega-company Starbucks continues to play with the idea of a completely cashless store, only accepting credit cards and mobile apps.

More and more people don’t carry cash anymore. When going out, we take our phone, ID, and credit card. With those, you can pretty much pay for anything. Even then, credit cards are becoming obsolete as phones nowadays can handle most payments.

As people continue their unknowing war on cash. The biggest winners are the four major financial institutions MasterCard, Visa, PayPal and Square. I find myself regularly reminding friends to continue to at least keep some cash on them for the following reasons.

FYI – I keep about $100 in my wallet at all times for these reasons. Again, please don’t rob me. I usually have (3) Twenty Dollar Bills, (2) Ten Dollar Bills, (1) Five Dollar Bill and the rest One Dollar Bills. Always stacked in order so I can quickly grab what I need.

In a cashless society, here’s why you still need cash

1.A Minimum Purchase on Cards – This is probably one of the biggest reasons why everyone should keep some extra cash on them. Most stores require a “minimum credit card amount” usually set at $5 to $10. This is because stores are forced to pay a 1.6% + $0.10 fee to process your credit card. The lower the price, the more it cuts into their profit.

If your store doesn’t have a “minimum credit card amount” it likely means they’re afraid to scare you away and prefer to absorb those extra costs for the extra convenience of their customers. If you don’t have cash, you’ll be required to buy extra things to surpass their minimum $5 or $10 credit card amount, and that’s not frugal.

2. Parking – If you’re frugal, you’re likely willing to park miles away to avoid paying for a parking spot. However, there are times that’s not an option. You’ll need to pay for a spot or worse a valet. If you’re stuck in a situation where a valet is your best option, it’s always easier to have the cash to hand over quickly.

3. When in a rush – There have been a couple of times I’m at a restaurant with coworkers and the server is swamped. The server is trying their best, but everyone is attempting to fit lunch in a 1-hour period. Rather than waiting for the server to process your credit card and return. It’s easier to lay down the cash and return to the office.

4. Soda Machines – It’s impressive to see the number of soda machines that now accept credit cards. However, it’s not yet universal implemented and many machines still only accept cash. In these moments when you absolutely need caffeine, carrying cash is handy!

5. Tipping – I’ve shared my thoughts on tipping before, and I now tip 20% for everything I do. Yet there are many situations, other than restaurants, that tipping is standard and credit card payments may not be an option.

One example was a Bike Bar I recently celebrated with friends (photo below of our Bike Bar). We paid the $234 through their online portal weeks in advance but that didn’t include the tip for our host. After a great trip, we tipped our tour guide with $40 because he went above and beyond. No one had a credit card processing machine on hand, and we didn’t want the extra hassle of finding our host on Venmo or PayPal. So we handed over cash, it’s still the easiest way to transfer money in person.

6. Special Discounts – This relates to #1 with the “minimum credit card purchase”. Many stores offer special discounts to people who pay with cash. This saves the store from paying a credit card processing fee and eating into their profits. Plus you save a few dollars when those savings are passed onto you.

7. When Your Credit Card Breaks – This is a thing. I’ve been at the grocery store many times with my credit card, and the “Chip” unexpectantly fails. Sometimes the card is dirty, sometimes the processing machine doesn’t like the angle of the card. Either way, it’s an embarrassing feeling to hold up a line while a tiny machine angrily honks at you. At times like these, having cash is a quick lifesaver and contingency plan to failing technology. It’s bound to happen, so being prepared helps!

Can you think of any other examples of when you might use cash over a credit card?

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Sadly it was not until my early 30’s when I started to mature with my personal finance moves. I guess I can say, “Better late than never.” but I still get a knot in my stomach every time I think about the time I wasted.

Today I want to talk about 10 personal finance moves I think every twenty-something should do right now. I am going to talk about what I wish I knew during and immediately after college. This article will be extremely personal, sharing examples of the mistakes I made along with a couple of right moves.

If you feel like you are following my twenty-year-old self, it is time to make some personal finance changes in your life.

My goal with this article is that anyone, young or old, learns something new to improve their own personal finances. It is your turn not to do what I did in the past!

1. Plan for your future major expenses

Boy did I fail hard on this! I was too caught up with living in the moment. I think a lot of us can be like this when we are in our twenties and it is something we should keep an eye out for.

Where did this hurt me? Purchasing a home. I should have been more aggressive in saving up for that down payment when my wife and I moved out to Colorado. Instead, I focused on materialistic items and experiences (which are important but it wasn’t the time) during our first couple of years out here.

Why did this hurt me? Prices shot up like a rocket in Denver. We could have bought our dream home five or six years ago. In the long run, this didn’t kill us but it did set behind. We ended up buying a good starter home. Which we recently we sold, making $90,000 off of it and were able to buy our dream home with that money. If we planned better we wouldn’t have had to pay the premium we did on our dream house.

If I could do it all over again, I would create a roadmap for myself with those major expenses we had coming up. For yourself, those purchases could be anything you know is coming for you such as a home, car, master’s degree, trips overseas, and so on.

With the roadmap, you should lay out how many years out you want to make the purchase and how much you need for each purchase. These measures will allow you to make a priority list as well as how much you need to put away each month for these. We just recently did this so we can buy a new car with cash in a couple of years.

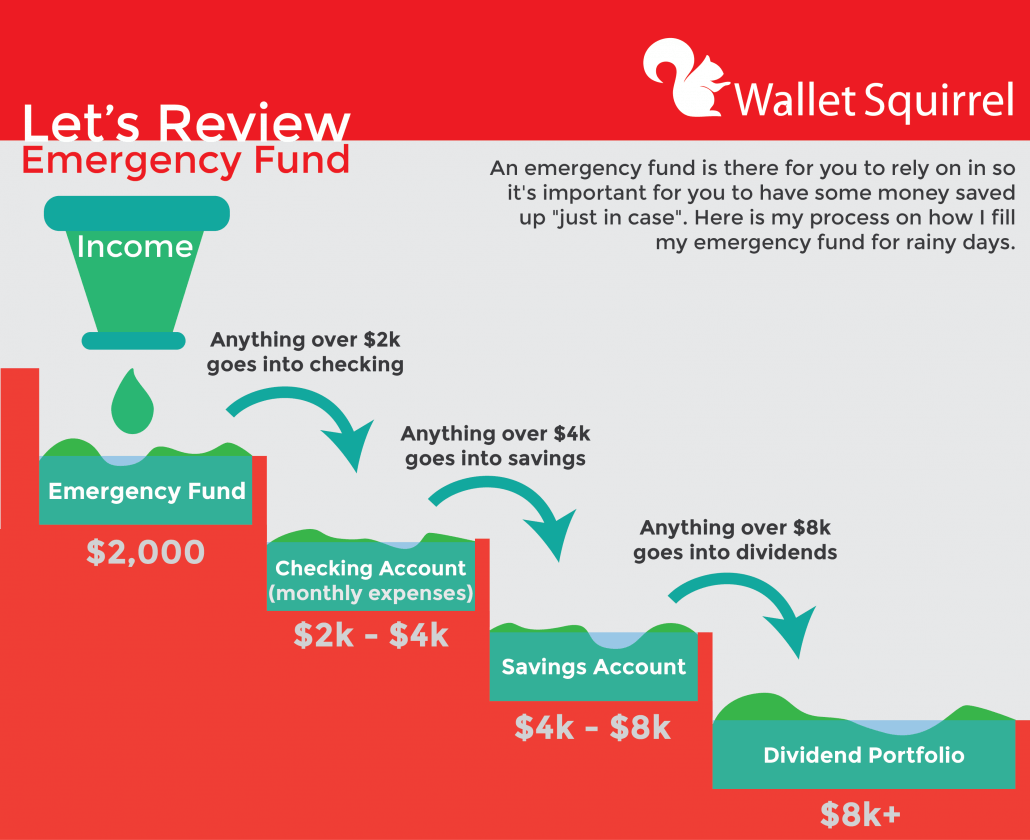

2. Have an emergency fund

The emergency fund is there for when life throws you a curveball. This curveball could include something horrible happening with your health, major car expenses, something going breaking your house, or even losing your job.

Many experts believe that you should calculate three to six months’ worth of essential expenses in your emergency fund in case you lose your job.

But Suze Orman (another financial expert) argues against the three to six-month number. She thinks you should save past the normal recommended number. In her interview with CNBC, she states, “You need to know that you are going to be secure.” This is why she recommends having eight to twelve months’ worth of expenses saved up.

I agree with Suze. Just out of college during the Great Recession, I struggled to find work. It took me nearly eight months to find a job that would somewhat support myself. Luckily, I was able to lean on my parents during this time. I couldn’t imagine going through that without an emergency fund or without anyone to help me.

Sadly, I did not learn from this experience. I continued in my twenties without an emergency fund. If a major expense came up such as a skiing accident or car crash, I would have been screwed.

My wife and I currently have twelve months of unemployment and two major house expenses saved up for emergencies.

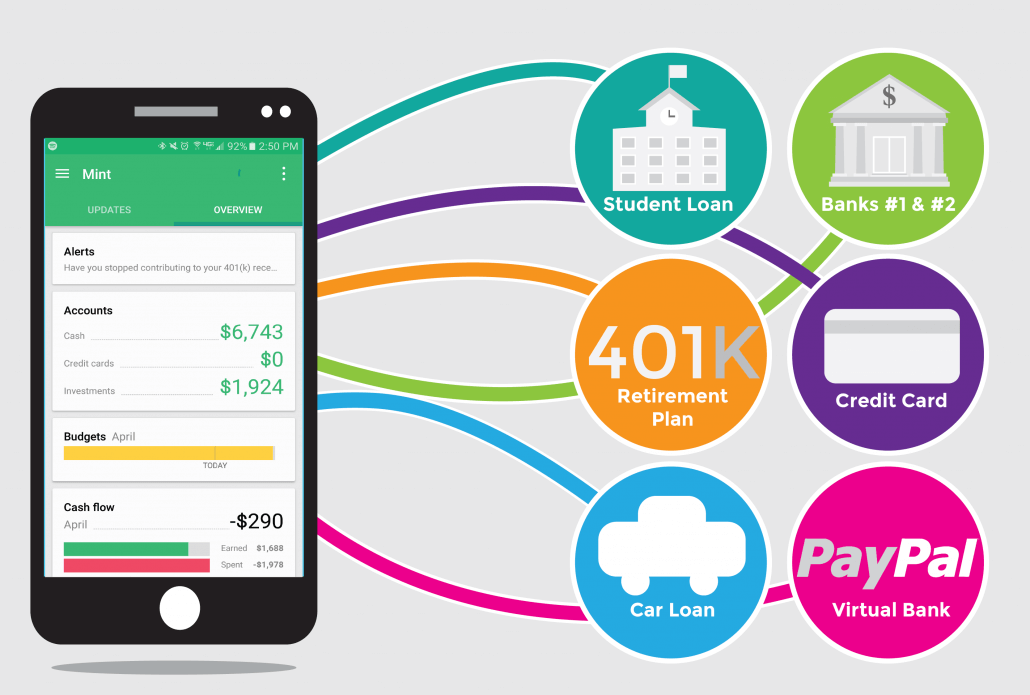

Your personal finance cannot be successful without a strong budget. Budgeting has become so easy with amazing apps such as Mint or Personal Capital. There really is no excuse for you not to be keeping a budget.

Setting up a proper budget will require way more time than what we have but we can take a 30,000-foot overview of it today. Basically, the goal is not to spend more money compared to what you make each month. You will want to layout your net income along with your monthly expenses and savings goals. Those savings goals along with any concrete monthly expenses that you cannot skip out on such as mortgage or utilities are the highest priority. From there you need to adjust those other expenses so your total does not go above your net income.

The difficult part, at least for me, is to stick to that budget (we will talk about this next). I am a foodie that lives in a foodie city, it is easy to lose focus and go over budget on the ‘Eating Out’ budget line.

It is so easy to spend on frivolous things nowadays. Man, there are some awesome materialistic things to purchase out there! You should see my shoe collection from when I worked in retail after deciding to leave landscape architecture. What a waste of money those purchases were!

This is where the budget comes in handy. You know how much you will make, save, and spend each month. Live within this budget, stay focused on this budget, and you will live within your means.

If you are feeling the urge to spend on frivolous things ask yourself this question. “Do I want or need this item?” Most of the time the answer will come back that you want the item, not need it.

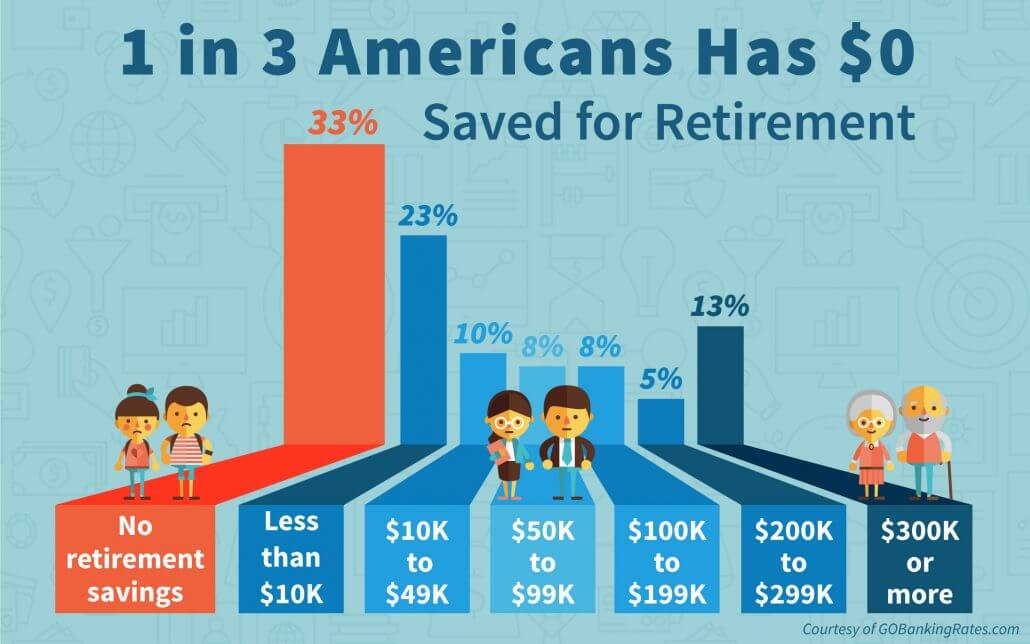

5. Start your retirement fund now!

In the first couple of years outside of college, I was the victim of immature thinking, “I’m young! Retirement is so far out! I do not need to save for that yet!”

Please do not be that person! Start saving now if you have not already! This will set you up for personal finance success in the long-term.

Fidelity says that by the time you turn 30 you should have saved up what half of your annual salary is (Investopedia). So if you are making $50,000 a year, you should have $25,000 saved up for retirement.

My wife and I did get back on track once we moved to Colorado after I got my first ‘big boy’ job and my wife got her teaching position.

I put off paying my student loans as long as I could. Big mistake. After almost seven years, I still had that original debt plus interest. I keep seeing friends on Facebook posting about how they just paid off the last bit of their student loans. Boy, do I envy them.

Get those student loans paid off as soon as possible to free up all of that interest money you are sinking into them. That interest money you save could go towards your retirement, your financial freedom.

7. Build up that credit score

This is an area that I excelled at. I was able to start building up credit back in college with student loans as well as an emergency credit card. Then when my wife and I moved out to Colorado, I was able to continue to build on top of this foundation. Over the last 12 years since starting my credit building I have only missed a handful of payments and now carry no credit card debt or car debt. All of this has led me to have an exceptional score!

There are some people who argue that a credit score is pointless if you shoot to be debt-free. This is a statement I can agree with if you either plan to never own a home or you have enough cash to buy a home outright. For most of us though, our credit score will be very important for us to buy that home. My wife and I both have excellent credit scores. Because of this, we were able to lock in a 3.25% interest rate for our latest home. This will save us thousands in the long run.

Have patience for the big goals. In today’s world, we are conditioned for instant satisfaction. I am very guilty of this. I used to think too short term such as, “I have to earn that money now!” Keep focused on your long-term goals which will make you happier.

Currently, my wife and I are planning to travel to France for our 10-year anniversary. I have been tempted to make purchases for our new house that would disrupt this plan. These short-term purchases would provide quick happiness but it will not be the same as the memories France will provide. I still get happiness from the Pacific Rim trip I took nearly twelve years ago.

Do not fall into this trap. Play the long game.

9. Invest

Speaking of the long game, I have started investing again with the Robinhood App. This investing is on top of our retirement fund. This is intended to earn extra money through dividend investing.

The goal is to start earning a significant amount of income off of dividends.

My personal goal is to eventually make $1,000 or more a month just off of dividends. As you can imagine, this goal will take a while to achieve because it will take a lot of dividend stock ownership to make a large impact but eventually things should start snowballing very well.

I wish I had started this back in my twenties. Just the Apple stock that I should’ve would’ve could’ve bought in college would be worth over $200,000 today.

10. Keep learning about personal finance every day

You should never stop trying to learn about personal finance. There is always something new to learn. This is why you should try to read a couple of books each year about personal finance or just finance in general.

Either way, life is boring when you are not learning new things every day. Might as well make those new things something that will get you to financial freedom sooner. You could even start a blog about the new things you learn and earn extra money explaining them to other people.

For me personally, I bought myself an Amazon Kindle. I read every night now because of that bad boy. You can even connect it with your local library (if they provide the service) to check out free ebooks. Learning something new is never wasted time.

Time to Make Your Personal Finance Moves!

All of my friends call me the old man, mainly because I am the oldest of us all. Well, it is your turn to learn from this old man and the financial mistakes he has made.

If you feel like you are making any of these mistakes, as I did, it is time for you to make a change with your personal finances. Do not waste away the time as I did, you do not get that time back. Time will just keep moving forward, leaving you behind.

If you are looking to earn some extra money and need some ideas on how to do that, then check out our Creative Ways to Make Money page. Here Andrew and I provide 70, yes 70, ways you can make money outside of your 9 to 5 job. We even test these out for you so you can easily figure out what side hustle is best for you.

Last week we had our article about how I started a company and why it failed horribly get featured on Rockstar Finance. That was really fun for our traffic that day. During the day a gentleman asked a very good question and I feel like my response needed more. So here I am writing an article to elaborate on my initial response to his question.

Basically what Adam was asking is if I have developed any good strategies to keep my life balanced after what I learned from my failed business adventure.

The simple answer is, “Yes I have!” Let’s dig deeper though.

Priorities

Of course, there is a lot of stuff I want to work on or do but that is not possible. Time is limited. That is just the reality of life.

What I have done is created a list of Priorities that are the most important things to me. I then only focus on those items throughout the week. These are items that will get me to where I want to be in life.

So how is my time split up? What are my priorities that I want to fit in on a daily or weekly basis? Let’s list them out.

Time with my wife (daily)

Time with my son (daily)

Time with close friends (weekly)

Work full time (daily)

Time in the mountains (weekly)

Exercise (daily)

Reading (daily)

Wallet Squirrel (daily)

Sleep (daily)

Practicing software development (weekly)

As you can see, there is A LOT going on here!

Curious as to how I balance it all? You should probably read on to find out.

Practice

I want to start off by telling you that it took me a while to figure out what methods worked best for my particular situation. It will also take you time to fine-tune your schedule to fit in with your priorities every day. There is no one solution that will fit everyone’s schedules. Sadly, that is just the truth.

My goal today is to help lessen those growing pains.

To get started you need to just start doing something. Jump right in with a schedule. You will need to be open to being flexible. Once started, you will quickly learn that your schedule is rough. It needs to be smoothed out with time and experience. Kinda like how a rough ball of clay can be turned into a beautiful piece of pottery.

Unlike a piece of pottery though, your schedule will never be solidified. I am finding that my evening schedule is having to change as my son is starting to go to bed later. This means I will most likely have to start working a little later into the night. GREAT…

Plan Ahead

Overall, I have a series of overarching goals that I want to accomplish for 2018. Every Sunday evening I like to put together a weekly to-list of smaller goals that are going to get me closer to those goals. Doing this helps me figure out what I need to accomplish for the week and then I can start planning what I am going to do on each day of the week.

I like to use the Tick Tick to-do list application. It allows me to create a to-do list every week then put those tasks on a calendar. I can literally plan out my whole week down to the minute. I don’t recommend you doing this though. Leave in some breathing room between events/tasks because not everything goes to plan.

The thought around this concept is to take 15-30 minutes every night to prepare for tomorrow. This includes everything from the Plan Ahead section you just read. Also, you should do the following.

Prepare your breakfast, lunch, and outfit for tomorrow.

Sounds silly but this saves A LOT of time when you are waking up at 4:30 in the morning to work out.

Look at what you did today.

Take a look back at what you got done, what you did not get done, and what you can learn from today to make tomorrow better.

Get a good night rest.

This means exercise, turn off the phone, and have a proper diet.

Get Creative

Sadly, I could not think of another title for these concepts that started with a ‘P’. To be honest, that was a total accident.

Anyways, you need to get creative with your time to make more time. For me, I was struggling to find time to work out 5 days a week. I tried to do it after work but I was being pulled in different directions once I got home. Then I tried to do it after my son went to bed but then I would be wide awake till late in the night resulting in me being super tired in the morning. Finally, I found a solution. Now I get up every morning at 4:30 to work out for 45 minutes.

I know, I am crazy. But, hey! It works for me!

You need to find what works for you by not being afraid to experiment and failing.

If you have a long commute, is there a way you could take mass transit instead to get work done? Can you bike to work to get in some exercise? Looking for more time to work on your new blog, get up in the morning an hour earlier.

Conclusion

Well, I hope this answers your question better Adam and for the rest of you. I hope you are now ready to get your highest priorities done every day.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Several years ago I decided to start my own landscape design company.

At the time I was working as a designer for a landscape materials company on the East side of Denver but the work environment was brutal. So, after 18 months of working in a hostile environment and dealing with a daily commute that sometimes took over two hours, I decided to move on. I wanted to go work for myself, leading to the start of Olson Landscape Design.

Boy, that did not go well.

Let’s explore as to what caused my business to horribly fail.

Most of it was caused by me being extremely naive in what it takes to run your own business. Today, I want to share with you what naive Adam learned from this experience so you do not have to find out the hard way.

Time

There is no downtime when you are self-employed, especially if you are just getting started off.

Think of it this way. Remember the times when you were little and it just snowed outside. What was one of the first things you wanted to do once you got to go outside and play? That is right! BUILD A SNOWMAN!!!

This might have just been me but I remember how hard it was to get that first snowball started. It would just glide on top of the snow as you pushed it, trying to get it to accumulate more snow. The smaller the little snowball was, the harder it was to gain momentum to get the snowball to start getting bigger and bigger.

Well, getting a company off the ground is the same way. It takes a lot of time and effort to get the ball rolling. There are no set times as to when you are working. The job needs to get done whenever you can get it done.

I did not realize this. I had other projects that I wanted to be working on as well and blending these different projects together did not work well.

Something else I did not know yet is that I had lost my passion for the profession. I was soon to find this out.

Passion

I had been trying to get my foot into the landscape design business for many years by the time I attempted to start Olson Landscape Design. It was a tough time because the Great Recession had hit the industry really hard. For several years after I graduated college in Landscape Architecture, I had applied for around 200 jobs. All of those applications led only to a 10-month long internship and then a full-time position at the hostile landscape materials company in Denver.

Simply put, I had gone through a lot of crap.

By the time I got around to starting my own business, I did not realize that I had lost my passion for landscape design. The will to continue to work when I did not want to was completely gone.

Passion is what you need to keep the drive. It is tough working at the hours of the day that is inconvenient when you have zero passion. I recommend taking a look in the mirror to really ask yourself if you truly do have a passion or not. Be honest with yourself.

Self-Confidence

I have always struggled with self-confidence issues. It is really tough to let go and accept that you are in fact awesome with amazing ideas. I also worry WAY too much what others think which plays into my self-confidence issues.

For me, as a young designer, I did not believe in my skills. I worried too much what the contractors thought about my designs. These issues compounded themselves that kept me from reaching out to potential clients as often. Obviously, this resulted in a lot of lost business.

In the end, this was the major issue that did not allow Olson Landscape Design to take off.

I had another designer friend who started his own business at the same time as me with similar experience. He had that confidence in himself which allowed his business to take off. The last time I talked to him he had his own construction crew. It was awesome to hear!

Official Stuff

I had no issue with designing a logo, setting up the website/blog, getting started with new designs. What really got me was all of that administrative stuff (setting up an S Corp, taxes, payroll, cold calling, and so on).

I knew that I would have to take care of all of this stuff before I got started. The issue is I did not know how far underwater my head was. To get this stuff done took a lot more commitment and I did not understand this. Remember, I told you I was super naive before getting started.

Anyways, now I know that there is all of this boring stuff I need to keep track of and how to do it best. It does not bother me anymore that my eyes have been opened.

Wrapping Things Up

Olson Landscape Design lasted for about 10 months until I decided to go back to school for my masters in Software Development and Program.

I am a better person because of this experience. It helps me on a weekly basis while working on my latest entrepreneur project, Wallet Squirrel. I am not as naive as I once was because my eyes have been opened.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

If you’re anything like me, you forgot entirely that libraries exist in our world of Amazon and Apple Books. These companies have made it so easy for us to instantly buy books & audiobooks that traveling to our local library doesn’t even cross our mind as an option.

I’m totally one of those people that bought books/audiobooks from Amazon and other stores. Honestly, it was fantastic and I would continue to do it if I had an infinite supply of money. However, like you, I don’t. Thinking about it, here are all the reasons I bought books/audiobooks in the past.

Reasons Why People Buy Books/Audiobooks

Owning a book is special – When you read a book that has a significant impact on you, it’s comforting knowing it’s always on hand to revisit again.

Never have to return a book you own – No late fees, ever.

You can lend it to others – Ever have a book that you want to share with others? Sharing books is a great feeling, letting others experience what you did.

Availability – Especially digital copies of books are always available for sale, you never have to wait till someone returns a book. The instant access to a book is very convenient.

Convenience – There are bookstores everywhere and online, they outnumber libraries. Although apps like “Overdrive” make it easier to borrow books from the library online, we’ll talk about that later.

Libraries are sometimes gross – I live downtown Denver, many of the city’s homeless utilize the library as shelter during the day. I think many libraries do around the country. People unfortunately often feel uncomfortable around these disadvantaged individuals and refuse to go to libraries for this reason.

Reasons Why People Borrow Books at the Library

It’s FREE to borrow books – This is a big freaking reason! People, like me, who want to save money should consider this reason as to why to give libraries a second look.

How Easy It Was To Get A Library Card Now-A-Days

I haven’t had a library card in years, I wasn’t even sure how hard it would be. Yet when I walked into our downtown library there was a large “Get A Library Card” sign, so I followed it.

I literally handed them my driver’s license, they copied the info and gave me a library card. The whole process took less than 5 minutes and I was told I could borrow up to 100 books at a time. 100 books seemed a bit much, I just needed one.

You Can Borrow Library Books/Audiobooks Online Now (It’s Called Overdrive)

The main reason I got a library card, and the reason you should too is the app “Overdrive”. Overdrive is an app on both the Apple App Store and Google Playstore that lets you connect you with your library’s online book collection. It allows you to borrow books & audiobooks online so you never have to visit a library. You’re just utilizing their online collection of books.

So Overdrive becomes a free Amazon where you can download books and audiobooks for free!

The only drawback is each library has a limited selection of books (still fairly big) and limited copies of those book licenses available. So your local library may have “Harry Potter & the Sorcerer’s Stone” but they may have only 5 copies. If those 5 copies are already “borrowed” you can be added to a waitlist and notified by email when it’s ready. Otherwise, if it’s available, you can download and listen immediately.

Cost Savings Over A Year

This is a significant re-discovery for me because I’ve been going through audiobooks like crazy lately at work. I put my headphones on and listen to some awesome books while working.

Recently I’ve been going through 2-3 books a month via audiobooks while working. Considering most Audiobooks on Amazon are around $25 (usually cost more than reading), those costs add up. If I were to listen to 3 books a month for a year, that would be $75 per month or $900 for the year. That’s crazy!

So now I use my library card and “overdrive” to listen for free. Sometimes they don’t have the books I’m craving at the moment, but I’m happy to find new ones in their collection. It makes me a bit more creative with my audiobook selections but I’m happy to be flexible in order to save money. Wouldn’t you? =)

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Today I want to help give you ideas to improve your life. Because of this, here are 16 daily habits that will improve your life.

Let’s get to making life better!

1. Get Good Rest

You probably already know this but I am going to tell you again anyway. GET SLEEP!

It is clinically proven that your brain does not function as well when you do not get a good healthy amount of sleep. Sleep plays a critical role in…

Immune function

Metabolism

Memory

Learning

These are just some of the roles that sleep helps. There is other vital functions sleep helps out with. (Harvard).

To me, it seems pretty obvious sleep is important. So make sure you get enough of it!

2. Excercise

Need help getting better sleep? Exercise helps with that.

Not only does it help with your sleep patterns but exercise is one of those things that really help your physical health.

Exercising is one of those daily habits that will improve your life. I know it is tough but it is crucial!

Not more than three months ago I started having horrible lower back pain that was affecting my life. Why? I had gotten that far out of shape. About a month ago I started getting up at 4:30 AM to exercise before work. Boom! Now the back pain is gone!

3. Wake Up Early

I know, this goes against #1 but it works well with #2! So let’s just go with it.

You really should get your day going early. This allows you to take control of your day rather having your day control you.

I have noticed that my productivity at work has gone up since I start getting up early to work out.

Are you one of those people that wants to wake up early but just cannot. I understand. Check out this article where I talk about how to do just that.

4. Eat Healthily

Back to the whole health thing that we mentioned in the exercise section. Health is key! If you want to go enjoy what you love doing, you need it.

To be upfront with you, I love a greasy hamburger with a side of fries and a beer for dinner. Sadly, we cannot do that every night and to be honey we should not be eating like that every week. Why not? Well because pizza has to fit in there somewhere.

In all seriousness though. Moderation is the key when you are trying to eat well. This is a more realistic goal and helps keep you from binging if you do relapse.

My wife and I eat about five really good meals each week. The other two we let things go. I have cut out MOST of the sweets and only have a beer as a special treat here and there.

Since starting this diet, that really is not a diet, I have lost almost 15lbs. Pretty crazy right?

5. Slow Down

This will look different for everyone. For me, I like to ponder the world in the shower.

Others might like to do yoga or meditate or go for a walk.

Why is this important? This quiet time really allows you to sort things out. Do you have something from work stressing you? Are you stumped about a life problem?

Taking some time to yourself is just what you need to work through these moments. Or maybe you just need some time to clear your mind.

6. Plan Your Day

To get the most out of the day you really should plan it. I use a to-do list app called Tick Tick that helps me plan out my day’s activities to the minute.

By having this plan in place I become more focused. My ADD does not kick in when I have everything planned out with what I need to work on.

7. Focus on High Leverage Activities

I always get overwhelmed when my to-do list gets too long. It is always tough to figure out where to start.

Awesome news! I can help you if you have the same issue as I do. Start with the tasks that are going to give the most bang for your time. Focus on those tasks with the biggest reward.

8. Learn New Skills

There is so much for us to learn in our lifetime. The time to start learning all of it is now!

Never stop learning!

Choose skills that are going to get you farther in life. These skills might get you farther in your career, financially, relationships, or whatever else you might think of. Just make sure the new skill is something important and will help you with your life goals.

9. Read

A great way to learn those new skills is by reading. Try to make a goal to read a new book every month.

One month I like to read a fun book then next one I read something that will teach me a new skill. This month I am reading an amazing book about habits by Charles Duhigg called ‘The Power of Habit’.

Go ahead and read away. Then apply it to everyday life!

10. Surround Yourself With Doers

One reason I love Andrew being my best friend is that he is a doer. His actions push me to do more. It also helps that we are so darn competitive to one-up each other.

Just so you know…I am winning… 🙂

By surrounding yourself with doers, you are allowing them to push you forward. We, as humans, naturally tend to match their performance.

Also, who wants to hang out with people that are always dragging you away from your life goals?

You do not want to always be dreaming because of the people you surround yourself with. You want to be celebrating the accomplishments with the friends that make you a better you.

11. Reflect & Evaluate

It is always good to stop, look into the mirror, and give yourself a good evaluation.

Are you heading in the direction you want to be? If not, this is the time to figure out how to get back on course.

Remember, be honest with yourself.

12. Laugh & Smile

Laughing and smiling brings joy to your life. What does joy bring? Joy brings energy!

People will want to be around that energy you bring into their life.

13. Be Positive

Negativity is no fun. No one wants to be around the person that is always negative.

Lately, I have noticed more and more negative thoughts from people. Most of the time this negativity will get you nowhere.

Just let it go and get back to living your life.

14. Enjoy the Outdoors

Who does not love getting some sunshine? Get outside, walk around, and breath in the fresh air!

Yes, this is another health daily habit.

No, this is not hard to accomplish. Every day on my lunch I go for a 30-minute walk outside. It is amazing how much more energized I feel afterward!

If I can do it, so can you.

15. Love

What is better than having an awesome life? Having an awesome life with someone you love.

I am very fortunate to have met the love of my life 10 years ago. I cannot imagine life without her.

Do not let that type of love escape your grasp.

16. Have Fun

To simply put it…

Love your life. Play. Don’t be too serious. Goof off.

Don’t let others ruin your fun.

Find others to be around that enjoy life as much as you can.

What Did I Miss?

I am sure I missed out on a lot! Comment below to tell us about any other daily habits that will improve our lives.

Does this sound amazing? Again, if you really want to learn how to change your habits, I highly recommend reading ‘The Power of Habit’. This book looks at habits from a scientific perspective as to what is really going on in the brain and how you can change it.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

The following is a guest post by Wendy of You The N

oise. Thanks for providing a bit more clarity on health insurance.

Health Insurance Considerations

The best way to safeguard yourself in a way which helps you to fully flourish is through proper diet and exercise. But even if you’re always on top of things in that regard, emergencies can injure you just as surely as illnesses can take you. There are recessive genetic problems which can arise, cancers that can come from the environment, and communicable diseases virtually everywhere.

It’s possible to avoid them, it’s possible to fortify your body against them, but these things aren’t always going to be avoidable. Especially if you’re the head of a household, or you’ve got children, it makes sense to get a healthcare solution. But this has gotten difficult in recent years. Though the “Affordable Care Act, ACA”, or Obamacare as it’s more widely known, was supposed to reduce the cost of health insurance, this didn’t end up being the case for everyone.

In many cases, health insurance premiums grew substantially. This has prompted many to seek other options. Sometimes they exist, sometimes they don’t. Single individuals have by and large been opting out, but this can be a bad idea.

Pragmatic Considerations

The question, “Do I need to pay the Obamacare penalty for being uninsured?” is a complicated one; consider what Healthcare.com says: “People who go more than three full, consecutive months without health insurance coverage are required to pay a tax penalty for that year. (Note: If you have health insurance for only one day of a month, it doesn’t count as a month without health insurance.)”

Technically, you may be able to avoid the penalty by having two months and a day of insurance; but probably not. Still, if you’re below $24k in yearly income, you likely won’t be penalized due to your lack of resources. If you’re doing reasonably well, however, you can expect a penalty between $600 and $2,000. The number of people in your household can be an influence in what you pay.

So from the beginning, opting out of a health insurance solution is going to cost you money in a legal sense; at least through the end of this year. But then you’ve got other collateral considerations. Say you cut yourself and need stitches. You may have to go to an Urgent Care facility, and you may find that they charge you more than you’d have to pay with the right insurance.

What happens if you’re in an automobile accident and get severely injured? Depending on who is or was at fault, you may end up having to foot the bill—and it can balloon into the hundreds of thousands of dollars very quickly. So if you haven’t acquired healthcare coverage yet this year, you’ve got until the 1st of October to do so. If you can source it cheap enough, you’ll save yourself a few hundred dollars. But if you can’t, then paying the penalty could be your cheapest option. Still, going without healthcare can be a risky proposition in modern times.

Difficult Decisions

Ultimately, you’ll have to decide for yourself how safe you feel without a healthcare solution. Some things can affect you in a way you didn’t expect—technology, for example, has a somewhat adverse effect on mental health. If you don’t have coverage, getting the help you need may be too costly, and it could really impact your life.

On the other hand, some nomads never have health care a day in their lives, and still, manage to live longer than anyone expects. There’s always that old guy with one eye, a limp, scars all over the place and a missing limb who goes by “Lucky”. Insurance helps make daily life less of a gamble. With tax penalties hiding around the corner, getting covered may be a cheaper option for you, too.

Special COVID-19 Update:

No one plans to get sick. It’s not something that’s at the forefront of our minds, but it helps to take steps to prepare for the unknown, just in case something like the COVID-19 pandemic happens. The coronavirus outbreak has brought up more questions than answers — but one thing we know is that it’s a good time to put measures in place to protect yourself and your family.

The CDC and WHO have given us precautions to avoid contracting and transmitting COVID-19, such as practicing good hygiene and following government guidelines on social distancing — two things that are proven to slow down the spread of the virus.

Aside from those, you might want to proactively look into life insurance, especially if you have a family or assets to protect, or debt that might be passed on to others if you die. With some policies, you can opt into “living benefits,” such as a long-term care or accelerated death rider. If you meet the criteria, these riders allow you to access your policy’s payout early to cover medical expenses. – Katia Iervasi, Insurance Writer, Finder.com

In the beginning of 2015 I paid off my credit card debt for the first time and started to learn about investing.

It was terrifying, but so totally worth it!

How I Perceived Investing As A Kid

Up until 3 years ago (I was 28), I knew NOTHING about investing. To me, investing was some insane, chaotic spree that made rich people rich and the middle class poor. I didn’t know how it worked, but I knew tons of people who lost money during the recession.

If you’ve ever watched any movie that talks about Wall Street or Investing, it’ll have your brain swimming in confusion trying to understand it. Were they just trying to make it look hard and impressive? (Yes).

I was terrified of investing, I just shut down anytime someone talked about investing and assumed they were a financial genius if they owned stock. Someone who had enough money to pay their bills, live their life and put something extra away investing for retirement was a financial god to me.

I Started to Learn About Money On My Own

Like I said before, at the beginning of 2015 (3 years ago) I paid off my credit card debt after paying countless $70 monthly payments. So once I paid it off, I wanted to use that $70 for something else, something reasonable.

I will admit my company did have a financial planner come into our office and talk about our 401(k) plan. While the company plan was pretty awful, the financial planner did a great job at terrifying me to death.

I will always remember their words “Running out of money in retirement is worse than death”

Well f*&k, that was more terrifying than Halloween. So I started to learn more about money and how it worked.

I started reading finance books like “Total Money Make Over” by Dave Ramsey. I consumed it in a day.

I started listening to finance podcasts. Not the hardcore stock analysis ones, but the more Investing for Dummies type of podcasts like “Listen, Money, Matters”. I LOVED that podcasts and in my mind, being surrounded by those announcers talking about money and finance as a regular thing, I began thinking of money in a different way.

After reading books and listening podcasts. I started to view money not as static thing to sit in my bank account, but more as income streams.

Understanding how much money I had in my bank account mattered less than how much I had coming in each month. That’s why investing became a fascination because it’s one of the most common income streams for people.

I Tried Investing $100 To See What Happens

On the podcast “Listen, Money, Matters” they raved about the investing app “Betterment” (Adam uses Betterment and did a review). They brought the Betterment team on the podcast and explained it and how it’s meant for people who know nothing about investing but want to start. That was me!

I remember how nervous I was signing up. I had to put in my info and social security number. I was convinced that I would immediately lose all my money straight away and because they knew my social security number, the IRS would start to hunt me down.

This was a legit fear I had.

Since I had so much anxiety, I only invested $100 to see what happened. I invested in a “moderate risk” portfolio which they automatically invested for me. All I did was put in $100 and waited to see what happens.

They say not to check it daily, but I did. Oh my goodness, for the first week I checked it hourly. I wanted to see EXACTLY how the stock market worked. After a week I limited myself to daily. So for 5 months, I checked my Betterment account every day, scruitinizing everything that happened.

However, I found that my money fluctuated. One day it went down to $99 then up to $102 and slowly kept rising. This helped me understand how the market moved (at least during those 5 months), how it worked and it slowly became less mysterious.

In fact, I started to notice little things like every once in a while, I would receive extra lumps of change in my account. Just a few pennies, but they were dividends. I received money just from owning certain stocks. I couldn’t tell which stocks with Betterment because it doesn’t show that amount of micro detail, but it was a great feeling.

Then I started to invest more and look at other stockbrokers (companies which you need to invest) like the Robinhood App (I still use Robinhood, here’s my full review on how it works). With Robinhood I could start to pick my individual stocks and it was amazing! I chose stocks that were on the safe side such as Apple, Realty Income and Johnson & Johnson that were well known and established. I knew if these companies tanked, there was something seriously wrong with our economy, so I felt comfortable.

I Wasn’t Addicted, But I Was Obsessed

After I learned how the stock market worked, I felt comfortable but wanted to see more gains than the couple of cents I had been earning. So I could have gone in two different directions. I could have started to invest in risky stocks for bigger gains (don’t recommend) or find new ways to earn money so I could buy more stocks. I did the latter.

I’m not advocating for a certain investing approach, but I do want you to see money as income streams rather than a lump sum. It absolutely changed my life.

Before I was happy with $2,500 in my bank account. It was more than any of my friends had. I now keep $4,000 in both my checking and savings account as an Emergency Fund and invest the extra money each month in my investment portfolio.

Knowing I have the extra money and extra streams of income each month gives me SO MUCH more confidence to know I’ll be OK if an emergency comes up or I want to go on a vacation. That piece of mind is one of the greatest feelings ever.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!