Unroll Me App Review – The Best 5 Minutes for Your Email’s Inbox

This Unroll Me App Review is going to show you why you should spend 5 minutes every month using this tool to clean up your email inbox. At the end of each month, your inbox will be writing you a thank you letter.

I wonder if it will send the thank you via email or snail mail?

Well, today we will talk about Unroll Me and really just how easy it is to use!

What is the Unroll Me App

To start off this Unroll Me app review, let’s answer a couple of questions as to what the tool does and who the company behind the tool is.

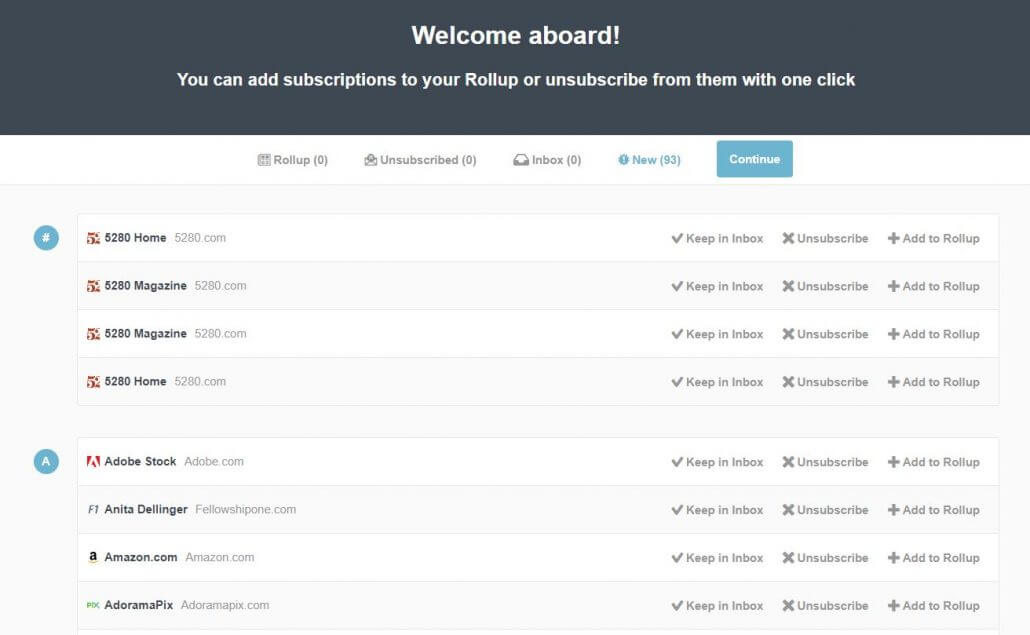

Unroll Me is a free service that allows you to easily (an understatement) unsubscribe from all of those pesky email subscriptions.

After signing in, the algorithm scans your inbox looking for e-commerce emails. Once found, the application lists them out allowing you to decide what to do with the subscription.

Who Is Unroll Me

Slice Technologies is the parent company that owns Unroll Me. They are able to make Unroll Me a free service because they collect data on the e-commerce emails you get. They use this data to, “build an anonymized market research products that analyze and track consumer trends.”

Slice says they strip all of the personal information (name, email, address, or anything else that could identify you) from the data collected. The technology behind Unroll Me is designed to determine if the email is personal or e-commerce. The algorithm completely ignores the personal emails as it searches your inbox.

You can read their blog for more information to see what the data is used for. Some of the research they post is actually pretty fascinating but I am a nerd when it comes to data.

How to Use the Unroll Me App

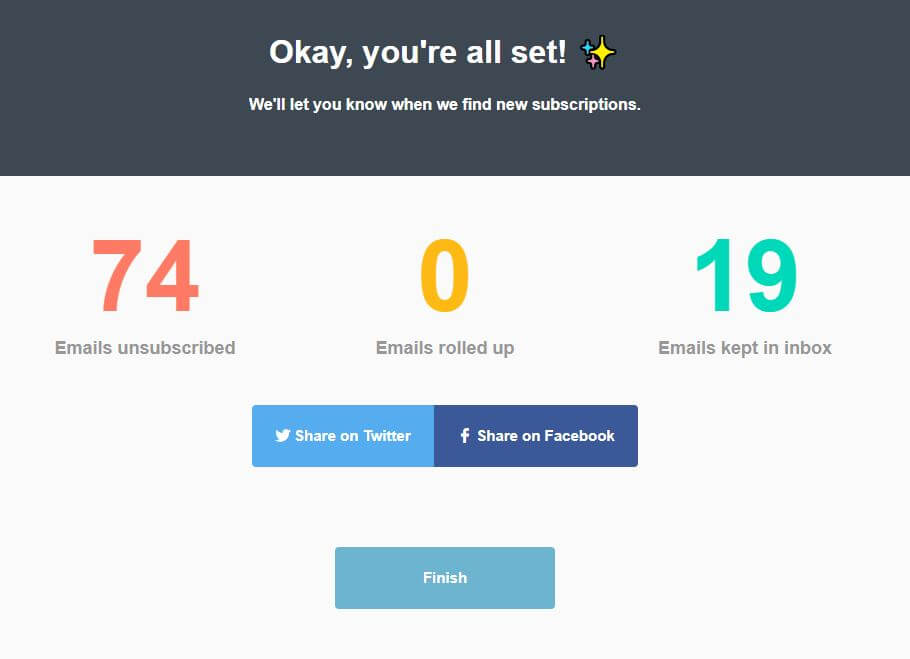

It literally took me five steps and less than five minutes of my life to unsubscribe from 74 subscriptions. I really could not believe that I was done already!

Choose your email provider and click through the prompts.

The algorithm will run. It searches through your inbox for subscriptions and then spits out a list of them.

Click either ‘Keep in Inbox’, ‘Unsubscribe’, or ‘Add to Rollup’ (I’ll explain that later) for each subscription on the list.

Success!

Was that not super easy? I know! Right?!?!

Oh! I mentioned I would talk about what ‘Add to Rollup’ is. The Rollup is a single email that Unroll Me will send to you at the end of the day. This email will consist of all the content from every email that is a part of the Rollup from that day. I have not personally tried this yet but they say the Rollup email is very digestible and easy to read.

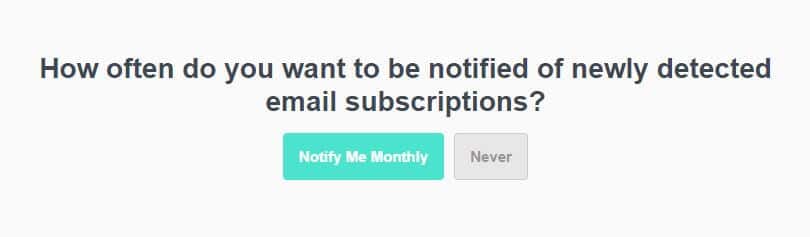

One final tip. If you would like, you can have Unroll Me notify you on a particular schedule to check for more subscriptions that were not in your inbox at the time. I decided to do the monthly reminder.

Why Unsubscribe?

We now live in a world where we are completely submerged by advertisements. The design of these advertisements is to tempt us to spend our hard-earned money on materialistic items.

These ads do not stop with commercials, billboards, or temporarily tattooed to the back of that guy’s head on the bus. Subscription emails also drown us every day with more temptation.

Using the ease of Unroll Me to unsubscribe from these emails trying to derail us from our financial goals allows us to stay focused. This is why you should unsubscribe to these emails.

Also, they are just annoying. Unsubscribing will also help keep your blood pressure down.

Final Take

To wrap up this Unroll Me app review I must say that I really enjoyed my experience with this tool to free me from those spammy email subscriptions.

Look, I understand if you are skeptical because of the data collection. You are entitled to have those feelings!

The algorithm design to strip out my personal information is what sold me to try out the Unroll Me app. I understand if you are still skeptical after hearing that. But hey! As a data guy myself, I do know this technology exists and it is pretty amazing.

Overall, this is a great free service. If you can get over the data collection thing, then I think you will enjoy it just like I did.

We all have the stress nightmare where your boss comes out of the blue and says “You’re fired”. That’s it and we spend the rest of the night in a panic. The problem is if it did actually ever happen, most of us don’t have a plan in case we do get fired.

Whether you’re thinking about losing your job due to stress, COVID-19, or any slew of reasons, it helps to have a plan. To lay out a blueprint, if this ever happened to me, here are 10 things to do if you lost your job and need money now.

Immediately Start

First, Take A Breath

It seems silly and not productive, but taking a breath is essential. People are let go or fired for a number of reasons and it’s not always a reflection of you or your work. Some things are just out of your control. Take an hour or take a day to let is sink it so it doesn’t consume you later.

1. Review Your Finances

Take a look at all the money you currently have. I personally use Mint to see all my bank accounts, credit card debt, and student loans all at once. You don’t need this, but make a list of every dollar in your possession. Look over your finances and get a feeling of how long you’ll last without a paycheck. It may not be pretty, but it’s something you absolutely need to know.

Know how much you need to spend each month, here is an example monthly breakdown:

Apartment & Utilities ($XX)

Food ($XX)

Car Insurance ($XX)

Cell Phone ($XX)

Internet ($XX)

Misc. ($XX)

PS. Also, consider health insurance as a cost. In most cases, your old employer would have provided this for you, but you need to talk to your HR to see how long this lasts. You may need to pick up supplemental health insurance until you get a new job.

Hopefully, you have some sort of Emergency Fund you can access if you lose your job. Your emergency fund will help cover rent/mortgage, food, and those expenses your paycheck normally covers. Most emergency funds should cover 4-6 months of expenses. If you don’t have an emergency fund, start saving up now but the following tips can still help.

I personally have an emergency fund I keep in a savings account, that will last me around 6-7 months. I know many people don’t have that. It took me 5 years to build. However it’s one of the best things I’ve ever done because it provides a mental safety net.

Let’s continue though as if you have $0 emergency funds.

If you just lost your job, you shouldn’t be watching Netflix, Hulu, or listening to Spotify. If you have any kind of subscription services that cost money regularly, you should cancel these until you get a job again. It may feel like a nice break watching Netflix between job applications, but you need to save all the money you can until you’re working again. If you feel this is too hard to do, consider using your parent’s or friend’s account temporarily to save money.

Needless to say, don’t make any crazy purchases thinking you’ll get a job next week when “you really try”. Until you have a signed contract with a company, I’d suggest avoiding the mall and any kind of gift ideas. If you can, cancel any flights, trips, running races, etc. Plus always ask if you can get your money back. It may not always be possible, but every little bit helps!

For me personally, I would cancel my gym membership ($73/mo.), cancel my Spotify account ($10/mo.) since there is a free version, and I’d probably quit investing in my brokerage account ($200/mo.) until I have a steady paycheck.

3. Ask to Defer Payments

During hard economic times, many companies are willing to work with you because they prefer late payments to nothing at all. Student loan services are often willing to reconsolidate loans or defer payments. Banks are sometimes willing to defer a mortgage payment or at least help with options. It often just takes a call and asks.

For me personally, I would call my student loan companies and ask to defer my payments until I get another job. That would save me $537/mo.

4. Budget and Eat At Home A Lot

One of the biggest ways people spend money is food and eating out. If you just lost your job, avoid going out to eat with friends (unless it’s a networking thing) or ordering in. It may not be sexy, but cold cut sandwiches, peanut butter and jelly sandwiches, and ramen got you through the dark years, it will again.

You know what you can cut to save money and you’ll see instant savings in your bank account. Remember one of the easiest ways of having more money, is not spending it!

One of the most popular tricks people use to limit spending is paying for food only with cash. The act of seeing the money physically leaving your wallet and the empty vacuum it creates, helps people be more selective with their purchases. I personally use credit cards because I enjoy the cash back, but I can’t argue with the success physical money has in limiting spending.

Start the Job Search

5. File For Unemployment

If you lost your job and actively seeking new work, you can file for unemployment. It varies state by state, but essentially you would file a claim with the Department for Labor and Employment and prove you’re actively looking for work every 2 weeks (depending on your state). Unemployment benefits will pay you a portion (likely small) of your previous salary. This is meant to help lessen the negative impact that unemployment has on the economy. It won’t be a glamorous option and you’ll meet some interesting people, but it will help.

6. Update Resume & Social Media Profiles

This is the time to update your resume with the latest accomplishments, promotions, volunteer efforts, jobs, references, etc. As you start the job search you want to make yourself look as good as possible. However, this isn’t limited to your resume. You should be updating your LinkedIn, Facebook, etc with the latest info so you’re casting a wider net for employers.

Don’t worry too much about how your resume looks, just that the information sounds grammatically correct and makes you look good! Many companies will force to you to copy all the exact same information into their often terrible online web forms. On the bright side, if your LinkedIn is up-to-date, you can always use their “one-click apply” to jobs posted on their site.

YouTube is also a great resource if you use it to better yourself now that you have free time. There are great exercise tutorials on YouTube, classes on coding (if you’re into high-paying jobs), and even brush up on software like Microsoft Excel. Use this opportunity to start a new job with a new skill set!

7. Tell Everyone You Know You’re Looking For A Great Job

It may feel embarrassing for you to tell anyone that you’re jobless. It’s a very vulnerable situation where you feel like something is wrong with you. There isn’t! It’s a normal thing, and job searching is a $200 billion dollar industry. People are constantly moving and switching jobs, you are now just one of them.

In most cases, when you tell people that you’re looking for a job, they want to help! They’ll often share new job openings they’ve heard of, or perhaps make recommendations to people they know in your industry. The fact is your chances of finding a new job dramatically increase when more people are on your team, helping you get a job.

I personally will change my LinkedIn page to “Looking for an Awesome Opportunity” and email my friends and family that I’m actively looking. More often than not, they will understand (because we’ve all been there before) and they’ll want to help!

Some of the best job search tips I’ve ever heard:

I recommend LinkedIn, Google Jobs, and Indeed for job postings. This is what most people use. I often avoid Craigslist.

Always use Glassdoor and read company reviews on how they treat their employees.

If you like a company, stalk their employees on LinkedIn to see if they went to the same schools you attended, clubs you’re in or charities you participate in. Ask them what it’s like there and ask for advice.

Have a salary in mind, knowing how much you need to cover all your expenses.

Make Money Fast When Your Jobless

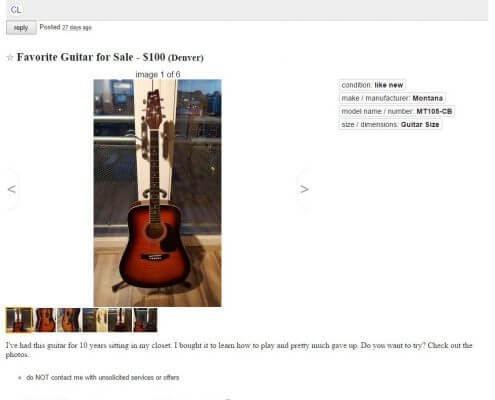

8. Sell Your Old Stuff for Extra Money

If you just lost your job and looking for extra money, consider selling your extra stuff on Craigslist or eBay. All that extra stuff in your apartment/house like old bikes or snowboards could make a couple of hundred dollars with a new family. That’s a lot of extra ramen noodles! Plus it’s a rewarding feeling getting rid of some of the junk in your life.

9. Write Articles For Money

I write all the time for a blog, but I discovered there are other places on the internet that pay you for writing! I’ve written a couple of articles on Seeking Alpha that pay $35 per article and $0.01 for every page view. It usually comes around $70/article in the long run.

With your new free time, this is probably one of the easiest ways to earn extra money while unemployed. You’ll have lots of extra time and most of the sites I listed pay between $50 – $100 per article.

For me personally, this is my plan. Spend my mornings looking for new jobs and my evenings writing articles. If I can write 1 article a night, at $50 per article. That’s an extra $1,500/month!

10. Side Gigs

We regularly talk about creative ways to make money, but some of the quickest ways to make extra cash are side-gigs. These are tasks that you can do anytime on different established platforms:

Random tasks in your city ranging from moving furniture to assembling IKEA (sites like TaskRabbit)

Many of these could be done in your afternoons while you spending your mornings (often the most productive time of the day) job searching for new opportunities.

Conclusion

Losing your job is incredibly scary, but there are TONS of resources here and online to help you find a new job and supplement your income. Hopefully, this helps make losing your job a bit less scary and aids in setting up your own backup plan!

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

That means the average person spends $54.63 eating out a week or $218.52 a month on just eating out. Unless you have a side-hustle that makes you lots of money. The obvious answer is to eat in!

What About Eating In?

Most people think they can easily quit dining out, and start cooking delicious meals. Here’s the thing with cooking for yourself, the movies get it wrong.

It’s not always a romantic and soothing experience.

Often times it’s a “Crap, I need to eat. What should I cook?” experience that you pray to the food gods you have the right ingredients in your fridge and clean dishes.

Let’s face it, we are busy in our lives and don’t have the time to visit the store every day buying fresh ingredients for a new recipe we found on the internet.

In fact, according to the Harvard Business Review, researcher Eddie Yoon over two decades collected data as consultants for consumer packaged goods companies. He found that:

15% of people say they LOVE to cook

50% of people say they HATE to cook

35% of people say they are ambivalent about cooking (mixed feelings)

If you’re one of the people that hate cooking, you should create a meal plan to make it as easy as possible.

Plan a week in advance what you’re going to eat for each meal and know how to cook it. This way you’ll have the ingredients and can plan accordingly for time.

However, not all plans work out.

Introduce The Peanut Butter and Jelly Theory

When meal plans fail, let me introduce Peanut Butter and Jelly sandwiches, otherwise known as a PBJ.

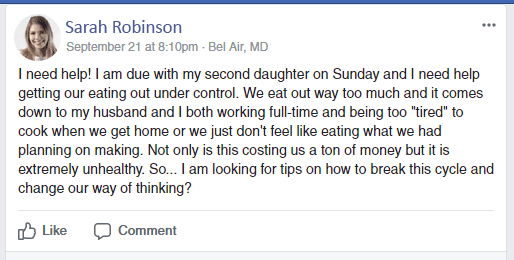

Let me first admit that I have an addiction to commenting on Finance forums, Facebook Groups, and Blogs. The mechanics of building wealth are simple and I’m always happy to remind people that things are often more simple than they appear. Like how I responded to this comment and created “The Peanut Butter and Jelly Theory”.

I get it, you want to start saving money on food and you’re looking for suggestions from the personal finance community to help.

Answers ranged from getting a crockpot to make meals simple, cooking large meals on Sunday and eating leftovers throughout the week, to buying frozen meals that may not be great for you, but easy to prepare.

All of the responses skirted around the idea that a solid weekly meal plan is the best option to help you save money on food. However, sometimes these meals don’t work out for a number of reasons, and once you fall off the wagon, you can end up at the local McDonalds.

So I introduced the Peanut Butter and Jelly Theory. The cost-effective, quickest meal ever to keep your budget on track.

This is easily the most actionable thing you can do to start immediately saving on your food budget. In many cases when people eat out, it’s due to convenience because they don’t have anything at home to sound appealing. That’s when the Peanut Butter and Jelly Theory comes in handy.

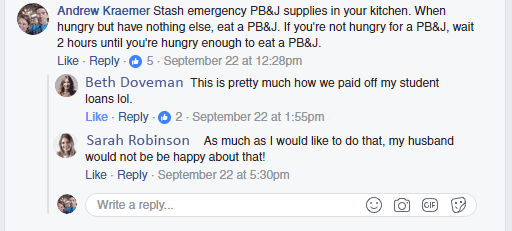

“Stash emergency PBJ&J supplies in your kitchen. When hungry, but have nothing else. You can have a PBJ. If you’re not hungry for a PB&J, wait 2 hours until you’re hungry enough to eat a PB&J.”

Sometimes a PBJ isn’t exactly what you’re craving and your favorite restaurant sounds better, or your family would not be happy about that. Well suck it up, you’ll soon be out of debt and you can buy your family a jet ski. Everyone loves a jet ski.

Try the Peanut Butter and Jelly Theory

If you want to save THOUSANDS on food budgets, you should try the Peanut Butter and Jelly Theory! Meals cost less than $1 to make, you’ll save time and money. Most importantly, you’ll have a secret stash of PBJs to make and everyone is a stack of cash saved from eating out!

You’re welcome.

Disclaimer: Wallet Squirrel did not invent the Peanut Butter and Jelly sandwich, just an advocate of saving money. Wallet Squirrel was not sponsored by big PBJ corporations to promote their superior and delicious product.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

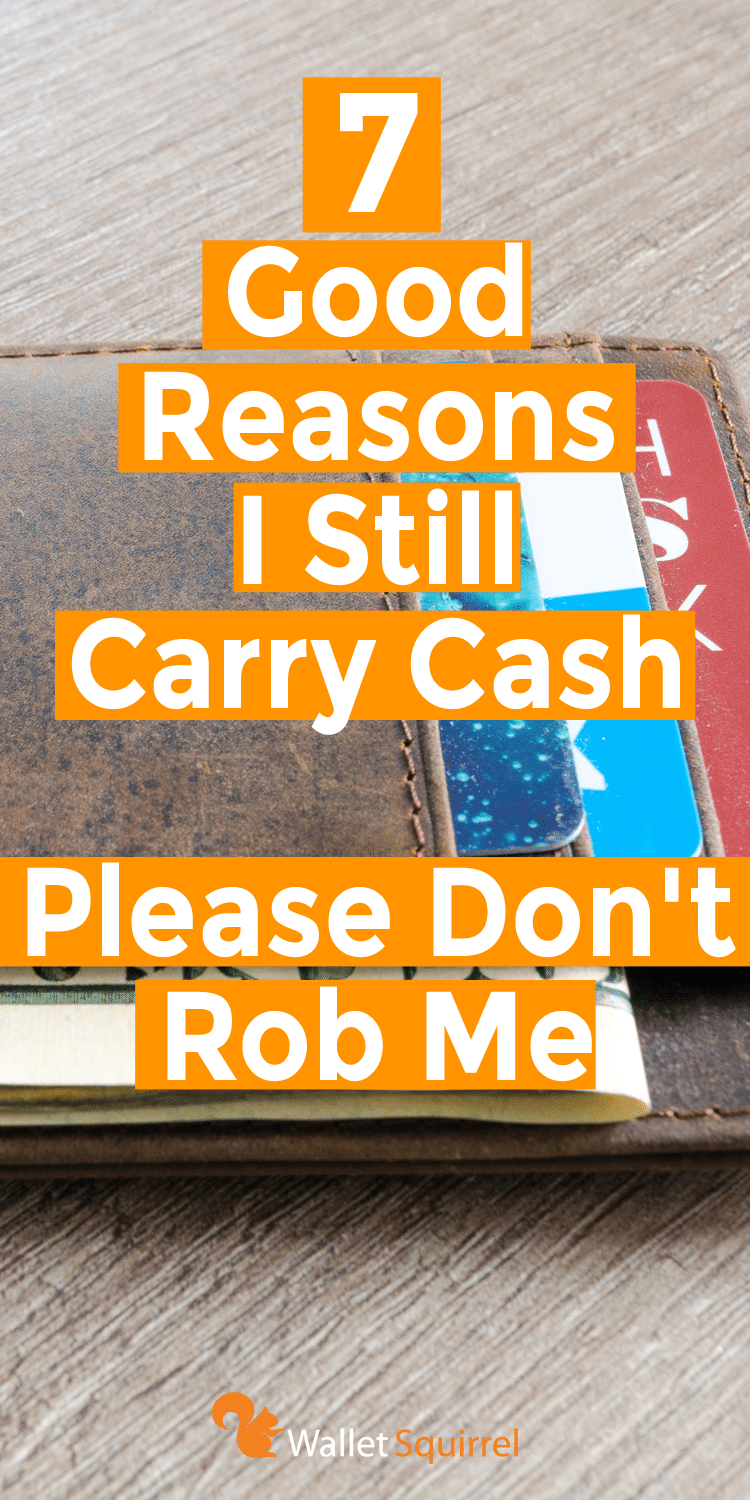

We are regularly becoming a cashless society with credit cards and digital transactions becoming the primary forms of money transfer. Even mega-company Starbucks continues to play with the idea of a completely cashless store, only accepting credit cards and mobile apps.

More and more people don’t carry cash anymore. When going out, we take our phone, ID, and credit card. With those, you can pretty much pay for anything. Even then, credit cards are becoming obsolete as phones nowadays can handle most payments.

As people continue their unknowing war on cash. The biggest winners are the four major financial institutions MasterCard, Visa, PayPal and Square. I find myself regularly reminding friends to continue to at least keep some cash on them for the following reasons.

FYI – I keep about $100 in my wallet at all times for these reasons. Again, please don’t rob me. I usually have (3) Twenty Dollar Bills, (2) Ten Dollar Bills, (1) Five Dollar Bill and the rest One Dollar Bills. Always stacked in order so I can quickly grab what I need.

In a cashless society, here’s why you still need cash

1.A Minimum Purchase on Cards – This is probably one of the biggest reasons why everyone should keep some extra cash on them. Most stores require a “minimum credit card amount” usually set at $5 to $10. This is because stores are forced to pay a 1.6% + $0.10 fee to process your credit card. The lower the price, the more it cuts into their profit.

If your store doesn’t have a “minimum credit card amount” it likely means they’re afraid to scare you away and prefer to absorb those extra costs for the extra convenience of their customers. If you don’t have cash, you’ll be required to buy extra things to surpass their minimum $5 or $10 credit card amount, and that’s not frugal.

2. Parking – If you’re frugal, you’re likely willing to park miles away to avoid paying for a parking spot. However, there are times that’s not an option. You’ll need to pay for a spot or worse a valet. If you’re stuck in a situation where a valet is your best option, it’s always easier to have the cash to hand over quickly.

3. When in a rush – There have been a couple of times I’m at a restaurant with coworkers and the server is swamped. The server is trying their best, but everyone is attempting to fit lunch in a 1-hour period. Rather than waiting for the server to process your credit card and return. It’s easier to lay down the cash and return to the office.

4. Soda Machines – It’s impressive to see the number of soda machines that now accept credit cards. However, it’s not yet universal implemented and many machines still only accept cash. In these moments when you absolutely need caffeine, carrying cash is handy!

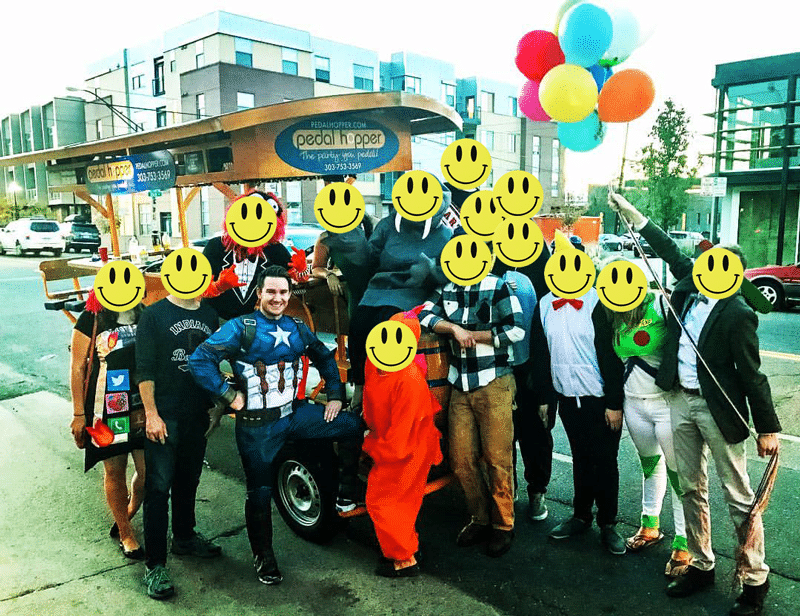

5. Tipping – I’ve shared my thoughts on tipping before, and I now tip 20% for everything I do. Yet there are many situations, other than restaurants, that tipping is standard and credit card payments may not be an option.

One example was a Bike Bar I recently celebrated with friends (photo below of our Bike Bar). We paid the $234 through their online portal weeks in advance but that didn’t include the tip for our host. After a great trip, we tipped our tour guide with $40 because he went above and beyond. No one had a credit card processing machine on hand, and we didn’t want the extra hassle of finding our host on Venmo or PayPal. So we handed over cash, it’s still the easiest way to transfer money in person.

6. Special Discounts – This relates to #1 with the “minimum credit card purchase”. Many stores offer special discounts to people who pay with cash. This saves the store from paying a credit card processing fee and eating into their profits. Plus you save a few dollars when those savings are passed onto you.

7. When Your Credit Card Breaks – This is a thing. I’ve been at the grocery store many times with my credit card, and the “Chip” unexpectantly fails. Sometimes the card is dirty, sometimes the processing machine doesn’t like the angle of the card. Either way, it’s an embarrassing feeling to hold up a line while a tiny machine angrily honks at you. At times like these, having cash is a quick lifesaver and contingency plan to failing technology. It’s bound to happen, so being prepared helps!

Can you think of any other examples of when you might use cash over a credit card?

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Let’s face it, we are in the age of digital media. Companies like Amazon and iTunes have made it so convenient for us to buy movies off their digital marketplace. We no longer need to go to the store to buy a physical DVD or Blu-Ray anymore. We can just buy a movie online and stream it instantly. However, do you actually own the digital movies you buy?

Let’s look at the most popular movie this year. Avengers Endgame is now available to purchase. You have the choice to buy the “digital movie” or a physical DVD/Blu-Ray. In both cases you’re actually buying a personal “license” to watch the movie, the difference is the format.

Yet, as you’ll learn, there’s a big difference between digital movies and the physical movies you’re used to buying.

4 Reasons you don’t really own digital movies you buy on Amazon

1. You can’t access your movie whenever you want

Whenever you want to watch a digital movie, you have two barriers to overcome. First, you need to have internet access on the device you want to watch, or thought ahead and have the movie downloaded to that particular device.

Then you also need to have Amazon’s proprietary software on that device to play the movie. Think app. Once you have those, you just need to pray your movie won’t be interrupted by constant buffering or their servers fail.

2. You can’t sell your movies or let friends borrow them

Ever been to a yard sale? You can usually find some awesome movie titles for sale. For the seller, it’s one of the easy ways to make money and you get an awesome movie to take home. Later, you can make a few dollars back when decided to sell it in the future.

However digital movies are now stopping this practice.

Your digital movie is directly tied to your account. You are not allowed to let friends borrow them or sell your movies once you’re done. Your movie is directly tied to your account. If a friend wants to watch a movie, they have to watch it on your account or buy the movie themselves.

3. Amazon can lose the movie rights or cancel your account at any time, and lose all your movies

If you read the long, lengthy Amazon agreement when you buy movies. They state that you can watch your digital movies as much as you want (subject to the limitations described in the Amazon Instant Video Terms of Use)

Those limitations stated in their agreement include “Amazon will not be liable to you if Purchased Digital Content becomes unavailable for further download or streaming.”. Meaning that Amazon isn’t responsible if the movies you bought suddenly and unexpectantly disappear. Doesn’t it feel like buying a digital movie is more like renting it for a long time until an unknown deadline when Amazon loses the rights? Something that doesn’t happen with an old DVD.

This has actually already happened to people. Consumer Reports found one such individual who purchased the animated film “Puss In Boots” from Amazon for $14.99 later to be told that due to “licensing restrictions, videos can become temporarily unavailable”. A situation where the typical movie lover can feel powerless.

Amazon can also cancel your account at any time with no warning, they’ve done it before. In April 2018 Fortune Magazine found hundreds of Amazon Prime account users had their accounts deactivated by Amazon for no reason.

All of those people’s movies and music which they “bought” were gone. They no longer had access to anything and with no warning. Amazon later said they removed people’s accounts for violating their return policy (returning items is a negative thing now?) and if people were accidentally removed, they were “encouraged” to contact Amazon to clear the matter.

So Amazon removed a bunch of people from their accounts and movies then informed them it was their responsibility to fix it. Ouch.

4. If Amazon goes out of business, you’re screwed

Remember when Myspace was a big deal? Tech companies like Amazon seem so large that they’ll be here forever but the fact is, they won’t. At least not as the same company they are now.

If Amazon does go out of business, everything you ever bought digitally is lost. Movies, Kindle books, the works.

The fact is, everything digital you buy from Amazon, technically remains theirs. When they’re gone, so is everything digital you bought.

Conclusion

Amazon and iTunes make purchasing digital movies incredibly easy, and at times even cheaper than actual Blu-Rays and DVDs. However, by giving up the physicality of a movie you can hold, you lose a certain amount of control of when and how you can watch digital movies.

You can’t sell them, lend them to friends, watch them without internet access (unless pre-downloaded) and you’re constantly at the mercy of Amazon and iTunes hoping they won’t deactivate your account, lose their movie licenses, crash their servers or go out of business.

That may be fine for most people, but it’s important to know digital movies work and how much control you have.

Personally, I always buy physical copies of movies becasue they typically come with a free digital code anyways. It’s the best of both worlds.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

I laugh because I’m going to hit on some of the age-old “renting vs owning” debates, with these lessons learned, but I won’t say which is better. Although you can probably tell from my comments throughout my letter. There are some things I wish I’d known, ideas I learned from renting experts like RENTCafé, and things I learned the hard way.

What I Would Tell My Younger Self About Renting

Dear Younger Self,

I’m 31 and still have never “owned” a home, but I have rented the past 5 years as an adult and 3 years before that in college, learning A LOT! Please make better choices than I/You did.

1. Always ask if there is a better price on rent. Many times there are deal or specials going on in an apartment complex that the leasing team doesn’t necessarily offer up front. However, a simple question of “can you do better?” will produce AMAZING results. I’ve received some amazing deals on apartments just because I asked that one simple question.

Also never quit asking that question, even when renewing your lease ask if they can do better. Sometimes, just sometimes they’ll come back with “I went to ask my manager and we can lower your rent for $100”. It never hurts to ask.

2. Maintenance is included in your rent, don’t hesitate to ask for needed repairs. I used to be so nervous about submitting maintenance requests not wanting to be a problem tenant. Even the small things like a slow leaking drain. I would go to the store to buy Draino to fix the drain myself. However, that’s not your responsibility. Maintenance is there to supply their own Draino to fix their building, it’s not your responsibility. Take advantage of your maintenance team for all those concerns. When in doubt, just ask your maintenance team about something and 9 out of 10 times, they’ll fix it.

3. When looking for Apartments, Studio Apartments are pretty great. To save you a couple hundred dollars, absolutely go for a studio apartment. They save you money, easy to clean and force you to assess what’s important enough to keep and throw away.

4. Location is everything. Think about those Uber receipts, where will you go every weekend and what personality type are you. If you’re a social person, you will absolutely hate living in the suburbs with a cheaper apartment. It’ll take you forever to get downtown to meet people and you’ll likely cancel plans to just stay home and avoid traveling. The extra money is worth it to live where you want to be.

5. Higher views are nice, but they don’t matter. Lots of apartment complexes make you pay extra the higher your apartment is. So someone on the 8th floor will pay more than someone on the 3rd floor. It’s not worth it, lots of times your blinds will be closed to block the sunlight glare on the tv. A better view only matters 5% of the time you live in an apartment.

6. It’s OK you don’t remember your Leasing Agents name, they’ll be gone in 6 months. Every time I apartment shopped, I created a great relationship with the Leasing Agent for the building. However, every time I did, 6 months later someone new would replace them. All that goodwill built up is instantly gone. The turnover rate for these positions is incredibly high.

7. Roommates are amazing, but living on your own is way better. I spent 3 years living with 2 amazing roommates (one of them was Adam). It was great to come home every day and chat with each other about our day and hang out. So I thought about living by myself would be lonely, it wasn’t. Living on your own is awesome! Once you live on your own, you’ll never go back! Lol

8. Constantly call your utilities to ask for better deals, there usually are. Once a year I call Xfinity for my internet and ask for a better deal and every year they find me one. Again it never hurts to ask.

9. You’re not likely to get your entire deposit back no matter how well you clean. I’ve been in apartments where I kept it spotless and even my parents helped clean when I moved out. However, no matter how well you clean, some apartment inspector will ding you for the smallest things and keep all or part of your deposit. While it’s not worth the effort of cleaning, you should still do it. Just know your deposit is likely gone.

10. Neighbors suck, so invest in earplugs, eye masks, and moderately noised fan. No matter where you go, you’ll have neighbors that every once in a while play music too loud or launch laser lights into your apartment as an afterthought (it happens). Unless this happens all the time, a set of earbuds, eye mask, and a fan to help drown out the noise are essential and help you avoid confrontations while your neighbors are drunk. It’s much better to speak with them in the morning.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

I live in an 8 story apartment building located in downtown Denver, Colorado. I choose to live here because it’s within walking distance to work and I always wanted to try downtown living with quick access to restaurants, bars and the plethora of city activities. However, I quickly learned that apartment buildings as an adult are very similar to college dorms as a freshman.

Yes, some apartments are nice, expensive and selective, but I don’t live there. I live in a regular apartment building where people are loud on the weekends and like to pull the fire alarm. Ugh!

Fire Alarm goes off

Literally the first weekend I moved into this apartment building, the fire alarm went off at 11:20 pm (that should have been a sign), I was still up and I freaked out, like nearly had a panic attack. I was in a new environment I wasn’t yet comfortable in, full of flammable boxes and everything I owned was moments away from going up in flames, literally.

Initially, I thought it was just a joke someone pulled the alarm because I’ve never been in a real fire before, but this building’s alarm was screeching. Deaf people down the street could hear it. So I popped my head into the hallway and sure enough, I saw smoke.

Fudgsicle (I don’t cuss a lot). This building is going to burn.

What’s important enough in my life to save

In this moment, the fire alarm is blaring, I see smoke and I’m covering my ears, trying to think what I should take with me. What do I save?

It’s funny to think about, everything I own is in a 582 square foot studio apartment. So I went from one end of the apartment immediately assessing the value of everything in a snap judgment.

Bookcase (Let it Burn) – It only has books, movies, and expensive art supplies. I can rebuy those later. Bye, bye first edition of the Harry Potter books.

Bed (Let it Burn) – Beds cost a ridiculous amount of money and I don’t want to pay for another one but it’s crazy to try to save a bed, no matter how comfy. Bye, bye bed.

TV & Gaming System (Let it Burn) – Funny how important buying a big tv is or how much time you spend watching Netflix, but in a moment like this, you’re so easy to leave it behind. These are replaceable, you can always get a new one. Bye, bye Xbox One.

Clothes (Took 2 Pairs of Clothes) – If everything was going to burn down, I would need a few sets of clothes to get through the next couple of days. I literally pictured myself going through the insurance claims over following weeks, so I wanted some clothing I could get by in. I grabbed some shirts, socks, pants, boxers and a jacket.

Kitchen (Let it Burn) – Who am I kidding, I barely cook. There is absolutely no food or kitchen appliance/utensils that I would want to save. Sorry Chef Ramsay, bye, bye kitchen.

Computer (Take the Computer) – I pretty much live my life through my computer for both personal and work stuff. While you can always buy a new computer, it was the documents on it that held the importance. Since it’s such a big part of my life, plus I imagined I would need it for any paperwork I needed to submit to the insurance. So the computer came with me.

Golf Clubs (Let it Burn) – I wouldn’t have time to play while drowning in my tears over my burnt apartment. Goodbye putters.

Hiking Bag (Let it Burn) – I actually considered taking the hiking bag with me. It already had all my hiking gear in it. Like my tent, sleeping bag, supplies and even some MREs. Everything I figured I would need to live in the street for a bit. However, I decided against it because I would probably crash with a friend. I was really iffy on this, but the bag can burn.

Firebox of important documents (Took with me) – All my important documents like my car title, social security card, passport and everything are kept in a fireproof lockbox, a very heavy lockbox. So while I figured it would likely survive a fire, I was paranoid and threw it in my duffle bag.

Wallet, Keys, Phone (Took with me) – These were probably the most important because they were the first thing I thought of. Especially the wallet (ID, credit cards, cash). Anything I didn’t have I could bye. So these came with.

Lastly, since I knew everything in my apartment would burn, I snapped a few photos from different angles on my phone so I could show my renter’s insurance everything they needed to reimburse me more.

So in a span of 3 minutes, while the fire alarm was blaring, I assessed the entirety of my life assets and deemed them worth saving or not. Isn’t that crazy to think about?

When I left my apartment, the most important things I owned was a set of legal documents, a computer, my phone, 2 set of clothes and my wallet. That’s it. It really makes you wonder what’s important enough in your life.

How the night ended

I grabbed my duffle bag full of the most important “things” in my life and took off down the hallway. Since I was still new, I had no idea where the stairs were. Luckily building codes require them to be posted around the elevators. So taking the stairs, I excited outside along the sidewalk with the rest of my 200 apartment residents. Then the fire trucks came.

Fireman charged through the doors and disappeared leaving everyone moseying around and chatting amongst ourselves. Conversations could be overheard of “dumb drunk people” to “did you see smoke, I saw smoke”.

We were left on the sidewalk with no information for 20 minutes before we heard the fire alarm go off and the firemen exit the building. We were given the all clear and started to walk in. As I passed, I could hear the building manager speak to some other tenants explaining that someone on my floor came home drunk and attempted to cook on the stove, filling the apartment and our floor with smoke.

Silly drunk people.

Seriously the fastest way to assess your life’s stuff

While I went back to my apartment a little angry for the whole ordeal. I was bewildered that I was currently holding everything important in my life.

Likewise I discovered what wasn’t important and how easily I thought “oh, I could always just buy another one”. All of my “stuff” had a price tag and was so easily replaced. It forced me to wonder what is actually important in my life. What can I get rid of and what do I actually need. Also what new stuff do I actually need to buy and would I actually save it in a fire? If not, do I really need it?

Of course, I don’t ever recommend you wait till your house/building is on fire to do a life assessment, but it is a challenging exercise to wonder what handful of your things you would save in a fire.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

We’re all about trying new ways to save money (and time) on Wallet Squirrel. Here is one of my latest attempts to save both during my regular lunchtime meals. In short, this my story on how I replaced my lunches with a $2.36 Huel meal replacement shake for a week for a Huel Review.

First – What Is A Meal Replacement Shake?

These are shakes that contain all the nutrients you need in a meal. Everything we’re supposed to eat as humans to be healthy, but all contained in a shake. No more worrying if your meal is healthy or balanced, you have scientifically measured powder you mix with water and that is the meal of the future.

These really started to become more and more popular lately thanks to Gamers who didn’t want to waste time cooking. They wanted a fast and easy method to eat so they could get back to gaming with little effort. Plus if it was healthy, they would have more mental capacity and energy to continue gaming.

This movement resonated with a lot of people of today’s generation that also wanted an easy, ready-to-go meal replacement shake so they could continue their busy lives.

Are Meal Replacement Shakes Good?

Does it matter? If you’re drinking a nutritionally complete meal and for far cheaper ($2.36 per meal with Huel) than a regular meal. Does taste matter?

For most people, it’s still an issue. To these people, no it does not taste good! These meal replacement shakes are far from tasting good. At best you get bland and yes, that is best!

What Type Of Meal Replacement Shakes Are Available?

For this, I had to do some research. Normally I’m all about Hot Pockets, Pizza Rolls, and Ramen Noodles, so basically anything else on the planet is more nutritious for me than these. However, if I was going to go all in with a meal replacement shake, I wanted the best. During my research, I looked at 2 different meal replacement shakes that came highly recommended.

Each of them had a loyal fan base and both fairly nutritional shakes, but I leaned towards Huel because it had a bit more protein per meal. Here is my one week Huel Review.

Huel Review: Here’s My Story Trying It For A Week

Pre-Huel Review – I spent about a week and a half researching Huel, reading reviews and listening to YouTube testimonials. I finally decided on Huel (located in the UK) and ordered off their website. I ordered 2 bags (28 meals) of their vanilla flavor. This is their recommended amount to buy your first time. Since it was my first time ordering, they gave me a free shaker and t-shirt. In total, it was $66.00.

I receive them in the mail about 2-3 days later, it was really fast delivery! I assume they have a distribution center in the US somewhere, otherwise, that was very quickly delivered from the UK.

I read on many of the reviews that people went to the extreme and replaced all of their meals with Huel for a week. That’s intense! In doing this, it took some time for their body to adjust to the alternate food source. They described some very embarassing gassy situations.

Sorry guys, I’m not doing that. I’m only replacing my lunches. I walk home for lunch every day with limited time to eat. I thought I’d substitute my lunches for this meal replacement shake to save both money and importantly time (also dishes).

Day 1 (it was rough) – It was the weekend so I tried I decided to try Huel early. I read the brochure that says 3 scoops is equal to 1 meal. So I throw 3 scoops into one of the shaker containers I already have and fill it with water. I didn’t think it mattered. The shakers I’m talking about have a metal wire ball that sits in the bottom and bounces around when shaken to additionally stir more of the protein mix in the water. I shake for about 2 minutes and take a drink.

AHHHHHHH, it was the weirdest taste of my life!

My face scrunched into a ball, shrinking as small as possible to hid from the strange taste of the Huel. I sat there motionless hoping it would all go away. In doing so, I tried to realize what was so off about it.

It didn’t have ANY flavor, it was the blandest thing I ever tasted! However it was the chunks of congealed powder that was the grossest thing ever. The powder clumped together in the water forming dry chunks of grit that caused my throat to revolt.

I just couldn’t deal with the chunks. It was the texture that got to me, texture wouldn’t wish it on my worst enemy. I was determined to finish it though, it was only Day 1. I kept taking drink after drink while working on something else to take my mind off it. In the end, it took me 4 hours to finish my first shake because my sub conscience wanted to delay the inevitable as long as possible. I seriously considered quitting this entire Huel review.

Day 2 – (it got better) – The next day was a Monday, so I came home from work and knew I had to try again. This time I had to do something about the chunks, I couldn’t take them anymore (YUCK)! So I threw the 3 scoops of powder, added water and dumped ice into a blender. I read ice helped in some other reviews. Then I let that concoction blend for a full minute. I’m sure 15 seconds would have been fine, but I wanted revenge at this point.

I poured the blended goo into the shaker they gave me. This shaker didn’t have a metal mixing ball like my others, but it did have a plastic mesh to help capture the large chunks of the powder from being drank. I appreciated this….

It actually wasn’t bad at this point. There wasn’t much favor but a complete lack of chunks really won me over. At this point, I realized maybe I could make it.

Day 3-7 (easy peezy) – The following days were easy and time-saving. I came home, set up the blender, added ice/water/powder, and poured it into my Huel shaker to drink. I began to finish the drink under 30 minutes (while doing something else). It wasn’t too bad and I eventually got used to the odd taste.

It’s not the worst thing in the world.

Moving Forward

I will probably continue to use Huel as my backup lunch option, like Peanut Butter and Jelly Sandwiches, when I have nothing else in my fridge after this Huel review, but it’s such a good option that’s quick and cheap. My only hang up is I regularly have to wash the blender and single Huel shaker after every use. My goal was to have zero dishes for the ultimate meal replacement.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

If you’re anything like me, you forgot entirely that libraries exist in our world of Amazon and Apple Books. These companies have made it so easy for us to instantly buy books & audiobooks that traveling to our local library doesn’t even cross our mind as an option.

I’m totally one of those people that bought books/audiobooks from Amazon and other stores. Honestly, it was fantastic and I would continue to do it if I had an infinite supply of money. However, like you, I don’t. Thinking about it, here are all the reasons I bought books/audiobooks in the past.

Reasons Why People Buy Books/Audiobooks

Owning a book is special – When you read a book that has a significant impact on you, it’s comforting knowing it’s always on hand to revisit again.

Never have to return a book you own – No late fees, ever.

You can lend it to others – Ever have a book that you want to share with others? Sharing books is a great feeling, letting others experience what you did.

Availability – Especially digital copies of books are always available for sale, you never have to wait till someone returns a book. The instant access to a book is very convenient.

Convenience – There are bookstores everywhere and online, they outnumber libraries. Although apps like “Overdrive” make it easier to borrow books from the library online, we’ll talk about that later.

Libraries are sometimes gross – I live downtown Denver, many of the city’s homeless utilize the library as shelter during the day. I think many libraries do around the country. People unfortunately often feel uncomfortable around these disadvantaged individuals and refuse to go to libraries for this reason.

Reasons Why People Borrow Books at the Library

It’s FREE to borrow books – This is a big freaking reason! People, like me, who want to save money should consider this reason as to why to give libraries a second look.

How Easy It Was To Get A Library Card Now-A-Days

I haven’t had a library card in years, I wasn’t even sure how hard it would be. Yet when I walked into our downtown library there was a large “Get A Library Card” sign, so I followed it.

I literally handed them my driver’s license, they copied the info and gave me a library card. The whole process took less than 5 minutes and I was told I could borrow up to 100 books at a time. 100 books seemed a bit much, I just needed one.

You Can Borrow Library Books/Audiobooks Online Now (It’s Called Overdrive)

The main reason I got a library card, and the reason you should too is the app “Overdrive”. Overdrive is an app on both the Apple App Store and Google Playstore that lets you connect you with your library’s online book collection. It allows you to borrow books & audiobooks online so you never have to visit a library. You’re just utilizing their online collection of books.

So Overdrive becomes a free Amazon where you can download books and audiobooks for free!

The only drawback is each library has a limited selection of books (still fairly big) and limited copies of those book licenses available. So your local library may have “Harry Potter & the Sorcerer’s Stone” but they may have only 5 copies. If those 5 copies are already “borrowed” you can be added to a waitlist and notified by email when it’s ready. Otherwise, if it’s available, you can download and listen immediately.

Cost Savings Over A Year

This is a significant re-discovery for me because I’ve been going through audiobooks like crazy lately at work. I put my headphones on and listen to some awesome books while working.

Recently I’ve been going through 2-3 books a month via audiobooks while working. Considering most Audiobooks on Amazon are around $25 (usually cost more than reading), those costs add up. If I were to listen to 3 books a month for a year, that would be $75 per month or $900 for the year. That’s crazy!

So now I use my library card and “overdrive” to listen for free. Sometimes they don’t have the books I’m craving at the moment, but I’m happy to find new ones in their collection. It makes me a bit more creative with my audiobook selections but I’m happy to be flexible in order to save money. Wouldn’t you? =)

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Today’s post is contributed by Amy Nickson, a passionate writer on finance. Amy is a professional blogger whom has started her own blog and also works as a contributor for the Oak View Law Group. Please share your opinions by commenting below.

10 Ways to switch to a minimalist lifestyle to make the most of money

Living a minimalist lifestyle has many benefits; it offers more free time, more money in the bank account, and a meaningful way to live the life. Once you adopt a minimalist lifestyle, it will change the way you live your life. Such a lifestyle can change the idea of spending a day, finding happiness, and fulfilling a dream.

However, adopting a minimalist lifestyle is not easy; it is a total transformation of lifestyle.

Most of us have materialistic mindset; therefore, living a minimalist lifestyle can be difficult at the beginning.

However, nothing is impossible; you can try to adopt the simple living mantra to understand the differences between living life with a lot of stuff and living with less.

Keeping in mind that most of you are a beginner when it comes to living a minimalist lifestyle, I am sharing some easy ways to help you to adopt it.

Minimalism is simplifying everything in your life

“Simplifying everything in life” – What does it mean? Well, it means you need to simplify your entire lifestyle including the diet, stuff, debt, health, home, and time.

Sounds scary! Here are 8 easy tips, which can simplify your lifestyle without taking a lot of stress.

1. Write down your minimalism goals

Since living as a minimalist is not easy; you have to be focused on it consistently. Thus, it is important to write down the motive of living a simple life. If debt problem is the main reason you want to simplify your lifestyle, then note it down. Similarly, you can write down other problems that are the reasons behind adopting the minimalist lifestyle, it can be getting no free time for family, feeling stressed out after work, failing to save money, wasting food, and craving for stuff.

If you think it is too difficult to keep going with the minimalist lifestyle, write down the goals. It will motivate you to follow your changed lifestyle.

2. Donate the extra things

Living with unnecessary things often overwhelm us, especially things that are extra. You should find out the extra things and keep them out of your sight. If you don’t need them for at least a month, then you should donate them to people who need them more than you. Once you start living with less stuff, your life will become blissful and less burdened.

Travelling is for refreshment, not for becoming a fashionista. People often take stress regarding the packing for their trip. If they are going for a 4-day trip, they usually pack for 8 days, which is wrong. Pack for 2 day for a 4-day trip. Wash clothes, dry them and wear the same clothes while on a trip. Instead of concentrating on dress up, enjoy the trip wholeheartedly. Carrying less baggage can allow you to move more freely and feel relaxed.

4. Declutter your home

A clean home is blissful. A home full of clutter makes you stressed, irritated, and busy all the time. Thus, you should try to make your home clutter-free, as much as possible. Though the task is not easy, yet you can give it a try. Make your home clutter-free, step by step. Start with your living room, kitchen counter top, bed room, dining space, etc. One day, you will find a neat and clean home with stuff that is necessary.

5. Simplify your style

If you are not a fashion blogger, who needs a lot of stuff to come with fashion tips, then you must try to simplify your everyday style. Don’t go mad with watches, shoes, dresses, bags, jewelry, accessories, etc. Honestly, you know how much is too much. So, show your commitment to other more challenging things in your life instead of wasting money and time on getting dressed up.

6. Go back to the basic

We all are now tech savvy and think all the gadgets are making our life simple. Yes, some are useful, but some are just making your life complicated. How?

The phone is not a necessity; you need to call someone in an emergency. But, now you have a smartphone with sufficient data. You are doing nothing but surfing the phone all the day. A basic phone is enough to contact someone. I agree that smartphone makes our life easier like easy banking, paying money by offering easy banking digital wallet, easy booking, etc. But, it also makes us engaged all the day and you don’t have time to talk to the person who is sitting just beside you.

It is way better to use such gadgets when in need. Enjoy some time with your dear ones to feel alive.

7. Cut down the cable cord

Now cable operators charge about $100 a month for 500 different channels. Out of all the channels, you watch only 7-10. I don’t know why do people pay so much money for things they don’t need at all. Simply pay for channels that you watch mostly and cut down the expenses for those unseen channels.

8. Simplify your meals

Having food is necessary, but thinking what you should eat at breakfast, lunch, and dinner for every day is not necessary. Set the meals for the whole week and rotate it. You will able to eat all the meals that are necessary to intake without wasting time at the grocery store.

9. Build an emergency fund

Financial problem is no doubt one of the biggest stress givers. If you don’t be good with money, it will always create problems. Most of the times, an emergency makes people financially stressful. To fight back with the emergency, people use some easy solutions like using a credit card, taking out a loan, borrowing money from 401(k) fund, etc. All these are financial blunders.

Why commit these painful financial blunders when you have an easy solution to combat with uncertain emergencies. What is the solution? The answer is keeping an emergency fund. Yes, by building an emergency fund, you can cope up with every unforeseen financial challenges without incurring additional debts. You just need to set aside a certain amount into an emergency fund. After a certain time, you will have enough money for any unforeseen emergencies. It will reduce your financial stress to a great extent.

10. Practice frugal living

Frugal living and minimalist living go hand in hand. Frugal living is all about living life in a meaningful way. Frugal living encourages to live within your means. By doing so, you can afford to live a life that you always wanted to live. Living frugally unlocks the world of financial prospects. It will help you save money, pay off debt, fund your children’s education, build a retirement fund (see Andrew’s Investments), plan for a trip, and so on.

Novice minimalists should avoid living an extreme minimalist lifestyle

Living a minimalist lifestyle has many benefits, but you shouldn’t live it in an extreme way. By living an extreme minimalist lifestyle, you will lose the focus and feel demotivated soon. So, you can read books on minimalist living to adopt a minimalist lifestyle in a proper way. The proper guide to minimalist living is important to live with less stuff while feeling delighted. Take small steps to adopt the new lifestyle with less stuff, less debt, and less worry.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Unroll Me App Review – The Best 5 Minutes for Your Email’s Inbox

Unroll Me App Review – The Best 5 Minutes for Your Email’s Inbox Unroll Me App Review – The Best 5 Minutes for Your Email’s Inbox

Unroll Me App Review – The Best 5 Minutes for Your Email’s Inbox