Today is day 67 of when I first started my latest Affiliate Website. The sad part is though I still haven’t “officially” launched the site yet. So I wanted to give you an update where I’m at currently, as someone who is trying to balance creating a website from scratch, and continuing to live life.

Where am I Currently With The Website?

The good news is the website is live with a great design and concept I still like. So far I’ve added a few products to sell on the homepage and I have one blog post done. Yes, only one….

The biggest thing with me is to figure out the processes I need to do to complete each task. Luckily I have done everything from adding new products to creating the style/look I want for the blog posts. Now that I have these throughout, experimented with and complete. To move forward, I just need to create content and fit it to the standards I’ve created thus far.

What’s Distracted me?

While I’ve had 67 days to work on the new website, in reality, I’ve only had about 2 weekends. This is because I do other things in my life in addition to my affiliate website. For example, I write regular content for Wallet Squirrel (this website), as well as write guest posts for other bloggers in hopes to gain links back to this site, Wallet Squirrel. This is where most of my free time goes, either to Wallet Squirrel or the new Affiliate Website.

Other things that have distracted me so far…

Workouts/Training – I’m signed up for a 10k race (called the BolderBoulder) in 3 months, a half marathon (Slacker Half) in 4 months and a 10-mile Tough Mudder in 6 months. So I’m daily working out and running. That takes up about 2 hours a day, every day.

Girlfriend – I very much like my girlfriend and need to spend time with her so she knows I’m alive.

Social Activities – I enjoy hanging out and visiting with friends and I still need to do these. However, I have limited myself to only going out on special occasions. Basically, if it’s some mundane excuse to go out to the bars, I pass. Yet if it’s going up to Breckenridge for snowboarding, I’m in. This has helped me not get into a rut of boring social activities and get some work done as well.

How The Other Guy is Doing

I started this Epic Niche Site Battle with Barnabas of SerialBoss. We continue to chat on LinkedIn to see how the other is doing. He’s in the same boat of feeling overwhelmed by two websites but we continue to make strides.

I expect to have my website completely launched and starting my marketing campaigns this weekend. Wish me luck!

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

The following is a guest post by Wendy of You The N

oise. Thanks for providing a bit more clarity on health insurance.

Health Insurance Considerations

The best way to safeguard yourself in a way which helps you to fully flourish is through proper diet and exercise. But even if you’re always on top of things in that regard, emergencies can injure you just as surely as illnesses can take you. There are recessive genetic problems which can arise, cancers that can come from the environment, and communicable diseases virtually everywhere.

It’s possible to avoid them, it’s possible to fortify your body against them, but these things aren’t always going to be avoidable. Especially if you’re the head of a household, or you’ve got children, it makes sense to get a healthcare solution. But this has gotten difficult in recent years. Though the “Affordable Care Act, ACA”, or Obamacare as it’s more widely known, was supposed to reduce the cost of health insurance, this didn’t end up being the case for everyone.

In many cases, health insurance premiums grew substantially. This has prompted many to seek other options. Sometimes they exist, sometimes they don’t. Single individuals have by and large been opting out, but this can be a bad idea.

Pragmatic Considerations

The question, “Do I need to pay the Obamacare penalty for being uninsured?” is a complicated one; consider what Healthcare.com says: “People who go more than three full, consecutive months without health insurance coverage are required to pay a tax penalty for that year. (Note: If you have health insurance for only one day of a month, it doesn’t count as a month without health insurance.)”

Technically, you may be able to avoid the penalty by having two months and a day of insurance; but probably not. Still, if you’re below $24k in yearly income, you likely won’t be penalized due to your lack of resources. If you’re doing reasonably well, however, you can expect a penalty between $600 and $2,000. The number of people in your household can be an influence in what you pay.

So from the beginning, opting out of a health insurance solution is going to cost you money in a legal sense; at least through the end of this year. But then you’ve got other collateral considerations. Say you cut yourself and need stitches. You may have to go to an Urgent Care facility, and you may find that they charge you more than you’d have to pay with the right insurance.

What happens if you’re in an automobile accident and get severely injured? Depending on who is or was at fault, you may end up having to foot the bill—and it can balloon into the hundreds of thousands of dollars very quickly. So if you haven’t acquired healthcare coverage yet this year, you’ve got until the 1st of October to do so. If you can source it cheap enough, you’ll save yourself a few hundred dollars. But if you can’t, then paying the penalty could be your cheapest option. Still, going without healthcare can be a risky proposition in modern times.

Difficult Decisions

Ultimately, you’ll have to decide for yourself how safe you feel without a healthcare solution. Some things can affect you in a way you didn’t expect—technology, for example, has a somewhat adverse effect on mental health. If you don’t have coverage, getting the help you need may be too costly, and it could really impact your life.

On the other hand, some nomads never have health care a day in their lives, and still, manage to live longer than anyone expects. There’s always that old guy with one eye, a limp, scars all over the place and a missing limb who goes by “Lucky”. Insurance helps make daily life less of a gamble. With tax penalties hiding around the corner, getting covered may be a cheaper option for you, too.

Special COVID-19 Update:

No one plans to get sick. It’s not something that’s at the forefront of our minds, but it helps to take steps to prepare for the unknown, just in case something like the COVID-19 pandemic happens. The coronavirus outbreak has brought up more questions than answers — but one thing we know is that it’s a good time to put measures in place to protect yourself and your family.

The CDC and WHO have given us precautions to avoid contracting and transmitting COVID-19, such as practicing good hygiene and following government guidelines on social distancing — two things that are proven to slow down the spread of the virus.

Aside from those, you might want to proactively look into life insurance, especially if you have a family or assets to protect, or debt that might be passed on to others if you die. With some policies, you can opt into “living benefits,” such as a long-term care or accelerated death rider. If you meet the criteria, these riders allow you to access your policy’s payout early to cover medical expenses. – Katia Iervasi, Insurance Writer, Finder.com

Bitcoin is still currently the most popular cryptocurrency. It’s the “new” thing along with blockchain technology, even if the price has come down a bit. However, if you’re thinking of buying any cryptocurrencies. You should learn how they’re taxed. Because yes, you will absolutely have to pay taxes on cryptocurrencies.

Cryptocurrency Isn’t Actually A Currency

The IRS considers cryptocurrencies “property” similar to how it does for stocks or personal property. Which makes the idea of buying things with cryptocurrency an awful idea. Here’s why.

Say you want to buy a sofa with Bitcoin. To actually make that purchase, you’re actually making two sales. You technically are first selling your Bitcoin to convert it to money (sale #1). Then you’re using that money to make the purchase of something, like a sofa (sale #2).

So to the IRS you are selling your Bitcoin and need to pay the short-term capital gain tax (25%) if you held that bitcoin less than a year, or long-term capital gain tax (15%) if you held it longer than a year. Then you will have the cash to now buy the sofa where you will pay sales tax on the sofa to actually buy it.

*Note the capital gain tax is factored for someone who earns $75,000 annually. Your tax percentage will fluctuate based on your annual salary. We’re also assuming you’re paying the capital gain tax because Bitcoin is worth more than when you bought it.

So you’re paying tax when you sell Bitcoin and then again for the sales tax.

Cryptocurrencies Are Monitored

Since cryptocurrencies aren’t affiliated with any government they shouldn’t be monitored, that was the idea, right? Wrong, Bitcoin is monitored by the IRS…to a degree.

According to the IRS, all your Bitcoin trades should be reported to the IRS because you should be paying taxes on the buying and selling of all cryptocurrencies. Every single time. So if you’re thinking of using sites that accept Bitcoin, all those purchases need to be reported to the IRS. Every time you sell Bitcoin.

So every time you buy something from Overstock.com, which accept Bitcoin. Those transactions should be (often not) reported to the IRS since you’re essentially selling “property”. That can be a tax headache.

During the Bitcoin craze, the IRS felt that Bitcoin sales were being under-reported because they expect people to report their own Bitcoin sales. Each year from 2013 to 2015, only about 800 taxpayers claimed Bitcoin gains. If you don’t report these gains, you can later be audited by the IRS, which no one wants. So be careful and report your Bitcoin gains.

If you think Bitcoin provides anonymity, think again.

In November 2017 a California Federal Court ordered Coinbase, the popular platform to buy and sell cryptocurrencies, to turn over thousands of records of customers to the IRS. It requested a list of everyone who bought, sold, sent or received more than $20,000 worth of Bitcoins between 2013 and 2015 (source). This could later be anyone who bought/sold more than $600 worth of cryptocurrencies.

You can expect the IRS to continue to monitor cryptocurrency brokers in the future.

Tax Laws Haven’t Caught Up With Cryptocurrency

If these seem harsh on Cryptocurrency, it’s a debate currently going in a legislature near you. Cryptocurrency is moving so fast (Bitcoin $1,000 to $19,000 in 2017) that the tax laws don’t have time to catch up. Especially since a digital currency is considered “property” by the IRS, it’ll continue to cause taxation confusion and headaches if you try to think of it as a currency.

As Bitcoin and other cryptocurrencies gain momentum, more people will use sites like Coinbase or the new RobinCrypto to purchase these new cryptocurrencies in hopes the price will skyrocket. In doing so you need to understand the tax implications and your responsibility to report your cryptocurrency activity.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

If you’ve seen our little pop-up or emails, we made a deal with our readers. We promised if you signed up for our email list, we’d do a drawing and a lucky person would win $100 to start investing. We’re doing this!

Remember these pop-ups?

Why Are We Doing This?

Lots of websites do different give-a-ways to encourage people to join their email newsletter. We wanted to try this, but actually, do something cool.

We didn’t want to create a “90 Ways To Save Money” pdf to give away or anything like that for new sign-ups. Frankly it was overdone and in reality, the easiest way to save money is not to spend it. There, that’s my free pdf.

So I asked myself, what do our readers actually want. Well, they want more money to invest with and pay off bills. So what if we gave (PayPal) someone $100 to use to invest. If they used that money to invest, it would grow to a lot more than $100.

I liked this idea.

How The Competition Worked

It was easy, if you signed up for our email list at any point, and still a member by the end of 2017, you would be eligible to win. We would do a drawing at the end of 2017 (actually this week) and whoever was selected, we would PayPal you $100 to do whatever they wanted.

Yes, you could use that $100 to invest, pay down bills or buy new shoes. We obviously can’t control what you will spend that money on, but we will STRONGLY encourage you to invest it. Investing is cool!

I’m going to do something no one ever does. Share how many email subscribers they have. It’s a bit scary sharing this because if it doesn’t seem like a lot, you can easily judge us based on how many other people subscribe. So vulnerable moment, go!

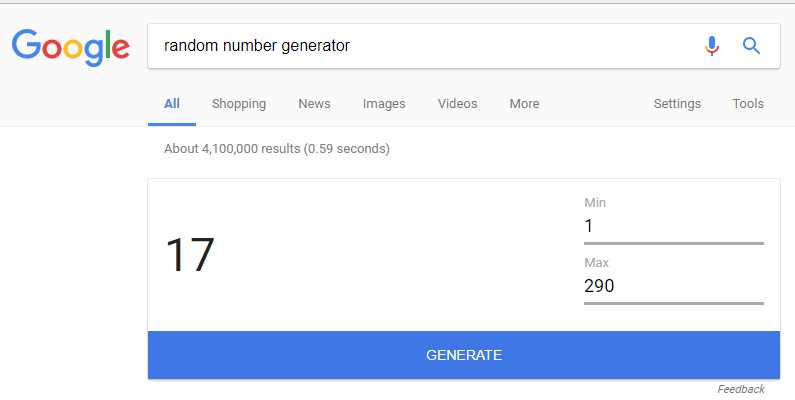

We currently have 290 email subscribers to Wallet Squirrel. All of them are eligible to win the $100!

To select a winner, I went to Mailchimp and reviewed the complete list of email addresses we had. This is how I discovered we had 290 email sign-ups. That is freaking awesome!!!!!

Then I went to Google’s Random Generator, basically, just typed “Random Number Generator” in Google, try it here! At the top of the page, there is a generator where you enter the min/max amount and hit “GENERATE. I got “17”.

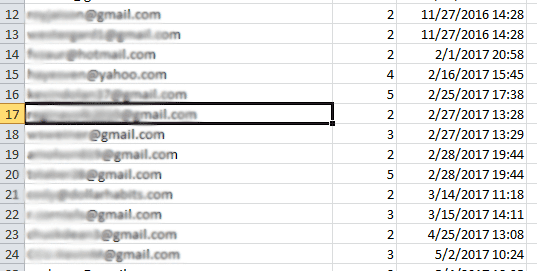

So at this point, I scrolled down Mailchimp’s list to locate number #17.

I’m now shooting them an email to let them know they won! Plus to see if this email works for their Paypal account. So check your email because I may have money for you!

Is The Competition Now Over?

Not even close, I REALLY like this idea. It’s a great way to encourage people to sign up for our email list and everyone gets a chance to win some money to do what you want (investing suggested). =P

In 2018, we’re doing this again but it’s for a chance to win $200 at the end of the year. Sign up and enter!

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

In the beginning of 2015 I paid off my credit card debt for the first time and started to learn about investing.

It was terrifying, but so totally worth it!

How I Perceived Investing As A Kid

Up until 3 years ago (I was 28), I knew NOTHING about investing. To me, investing was some insane, chaotic spree that made rich people rich and the middle class poor. I didn’t know how it worked, but I knew tons of people who lost money during the recession.

If you’ve ever watched any movie that talks about Wall Street or Investing, it’ll have your brain swimming in confusion trying to understand it. Were they just trying to make it look hard and impressive? (Yes).

I was terrified of investing, I just shut down anytime someone talked about investing and assumed they were a financial genius if they owned stock. Someone who had enough money to pay their bills, live their life and put something extra away investing for retirement was a financial god to me.

I Started to Learn About Money On My Own

Like I said before, at the beginning of 2015 (3 years ago) I paid off my credit card debt after paying countless $70 monthly payments. So once I paid it off, I wanted to use that $70 for something else, something reasonable.

I will admit my company did have a financial planner come into our office and talk about our 401(k) plan. While the company plan was pretty awful, the financial planner did a great job at terrifying me to death.

I will always remember their words “Running out of money in retirement is worse than death”

Well f*&k, that was more terrifying than Halloween. So I started to learn more about money and how it worked.

I started reading finance books like “Total Money Make Over” by Dave Ramsey. I consumed it in a day.

I started listening to finance podcasts. Not the hardcore stock analysis ones, but the more Investing for Dummies type of podcasts like “Listen, Money, Matters”. I LOVED that podcasts and in my mind, being surrounded by those announcers talking about money and finance as a regular thing, I began thinking of money in a different way.

After reading books and listening podcasts. I started to view money not as static thing to sit in my bank account, but more as income streams.

Understanding how much money I had in my bank account mattered less than how much I had coming in each month. That’s why investing became a fascination because it’s one of the most common income streams for people.

I Tried Investing $100 To See What Happens

On the podcast “Listen, Money, Matters” they raved about the investing app “Betterment” (Adam uses Betterment and did a review). They brought the Betterment team on the podcast and explained it and how it’s meant for people who know nothing about investing but want to start. That was me!

I remember how nervous I was signing up. I had to put in my info and social security number. I was convinced that I would immediately lose all my money straight away and because they knew my social security number, the IRS would start to hunt me down.

This was a legit fear I had.

Since I had so much anxiety, I only invested $100 to see what happened. I invested in a “moderate risk” portfolio which they automatically invested for me. All I did was put in $100 and waited to see what happens.

They say not to check it daily, but I did. Oh my goodness, for the first week I checked it hourly. I wanted to see EXACTLY how the stock market worked. After a week I limited myself to daily. So for 5 months, I checked my Betterment account every day, scruitinizing everything that happened.

However, I found that my money fluctuated. One day it went down to $99 then up to $102 and slowly kept rising. This helped me understand how the market moved (at least during those 5 months), how it worked and it slowly became less mysterious.

In fact, I started to notice little things like every once in a while, I would receive extra lumps of change in my account. Just a few pennies, but they were dividends. I received money just from owning certain stocks. I couldn’t tell which stocks with Betterment because it doesn’t show that amount of micro detail, but it was a great feeling.

Then I started to invest more and look at other stockbrokers (companies which you need to invest) like the Robinhood App (I still use Robinhood, here’s my full review on how it works). With Robinhood I could start to pick my individual stocks and it was amazing! I chose stocks that were on the safe side such as Apple, Realty Income and Johnson & Johnson that were well known and established. I knew if these companies tanked, there was something seriously wrong with our economy, so I felt comfortable.

I Wasn’t Addicted, But I Was Obsessed

After I learned how the stock market worked, I felt comfortable but wanted to see more gains than the couple of cents I had been earning. So I could have gone in two different directions. I could have started to invest in risky stocks for bigger gains (don’t recommend) or find new ways to earn money so I could buy more stocks. I did the latter.

I’m not advocating for a certain investing approach, but I do want you to see money as income streams rather than a lump sum. It absolutely changed my life.

Before I was happy with $2,500 in my bank account. It was more than any of my friends had. I now keep $4,000 in both my checking and savings account as an Emergency Fund and invest the extra money each month in my investment portfolio.

Knowing I have the extra money and extra streams of income each month gives me SO MUCH more confidence to know I’ll be OK if an emergency comes up or I want to go on a vacation. That piece of mind is one of the greatest feelings ever.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

I get the simple reason why we work, we want to make money to do the things we want to do. We trade time and energy for money. Then spend money on things to make us we need/want. This I totally get.

However, most of us are trading time and energy for money and still unhappy.

In fact, over 52.3% of Americans are unhappy at work.

This is crazy! In most cases if something makes you unhappy. You quit doing it! Yet most of us go to work every day at places we don’t want to be.

Are we idiots?

Are You Unhappy With Your Job?

I was recently asked if I was unhappy with my job? I was a little surprised a co-worker asked me this. Their reasoning was that I USED to be extremely happy and excited about everything, now I was more monotone or lacked the excitement I used to have.

Honestly, I was a little pissed. No one wants to be told that they lack anything. Yet in reality, I was madder at myself that I let it show that I was unhappy. I’m part Irish, I’m used to bottling up my feelings and not tell anyone that anything is wrong.

It made me ask myself if I was unhappy with my job? It was pretty scary.

What Does Unhappiness at Work Look Like?

If you ask yourself “Are You Unhappy At Work?” it’s not an easy answer. So I started to create a list of signs that would force me to see the truth.

Do I hate waking up in the mornings and coming in for work?

Do I feel I have no future at the company I’m at?

Does the day fly by or drag on?

Do I get excited about new projects or is it dread?

Am I doing the same thing over and over or is it new and exciting?

How do I describe my job to new people?

Does Jenny in Accounting ask if you’re unhappy at work? WTF

Dang, I totally answered yes for quite a few of these. So do I quit my job now or start looking for a new one? I freaked out just writing this list.

Does it even matter though if I hate my job? Whether I hate it or love it, I still NEED it. I have bills to pay and the money I make can buy things that make me happy. Should something I do 40 hours a week need to make me happy?

Well, yes….. Your job should totally make you happy. It absolutely should. However, before you quit you should answer the same question I’m now asking.

What Would Make You Happy At Your Current Job?

The other day I pulled a senior co-worker aside and asked them “What do you think I should do in 2018 to improve the company, goals, vision, etc?” I was expecting some generic answer like things to help the bottom line. However, he surprised me entirely.

One of the best questions I’ve ever been asked was “What do you want to do that makes you happy?”.

Holy Cow! It’s a simple question, but one I’ve never been asked before. I couldn’t actually answer right there and there though. I told them I had to think about it and I’m still thinking about it.

What would make you happy at your current job?

Most people say better pay, but that’s a reward, not necessarily something that affects your everyday duties. What would you change in your day-to-day duties that would make you happier?

That’s currently what I’m thinking about. What would you say?

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Happy Thanksgiving (American readers)! However, if you’re an international reader, Thanksgiving in America is just a day where people are reminded to be thankful for everything we have and celebrate with eating lots of turkey and pie. Usually surrounded by friends and family.

However in this Thanksgiving post, I wanted to be reminded of how far I’ve come, and our readers, in understanding finance. Because it wasn’t long ago (only in 2015 I paid off $6,000 of credit card debt) that I knew NOTHING about finance and started learning. So I found some interesting finance facts to remind myself of how far I’ve come.

10 Fun Finance Facts

Student Loans are in the trillions of dollars and two of five student loan accounts become delinquent within the first five years of making an attempt to pay student loan payments (source). I have auto-deduct on my student loans, it helps A LOT!

Nearly 30% of Americans don’t have at least 3 months of money to get them by if something happens (source). Personally, my Emergency Fund has 3 months of cash I can tap before I start pulling from my investment accounts to get me by.

In the days of the pilgrims (see thanksgiving themed fact) a US Dollar was called a “buck” because the pelt of a male deer was worth a dollar (source). I didn’t know this before!

Did you know Walt Disney every year for the holidays gave his housekeeper stocks of Disney? By the time his housekeeper, Thelma Howard died, she amassed a $9.5 million dollar fortune (source). Be nice to housekeepers and thankful for everyone doing these thankless jobs!

Don’t take investment advice from celebrities. I’m thankful I never have. The Rapper 50 Cent in 2011 started tweeting about H&H Imports (stock ticker HNHI), an investment he owns and told people to invest. Although his tweets are now taken down, he made $8.7 million from his comments on the penny stock (source). Can’t imagine his followers did as well.

If you’re having a bad day, just remember Ronald Wayne. Ronald was a third co-founder of Apple along with Steve Jobs and Steve Wozniak. Ronald sold his 10% stake in Apple in 1976 for $800. That 10% stake is now worth more than $35 billion (source). I’m thankful not to have that guilt on my conscious. Remember buy/hold!

I hate coins, but I’m thankful they add up! In 2015, the TSA (the people at airport security lines) collected $765,759.15 in loose change. This is the money people just left behind in those long lines and x-ray machine bins. They get to keep it all too (source)!

Buy and hold stocks are a thing. As of January 2013, there were 16 people left in the world who were born in the 1800’s. If they invested (and held) in the stock market, US stocks had increased 28,000% during their lifetimes (source). I’m thankful to start buying and holding so young. I could totally live to be a hundred.

46.1% of Americans will die with less than $10,000 in assets (source). This factoid haunts my dreams. I’m thankful I have more than this currently.

In 2011, US charitable giving was $298 billion. That’s more than the GDP of all the countries in the world, except 33 of them (source). That’s pretty awesome and something to be thankful for!

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

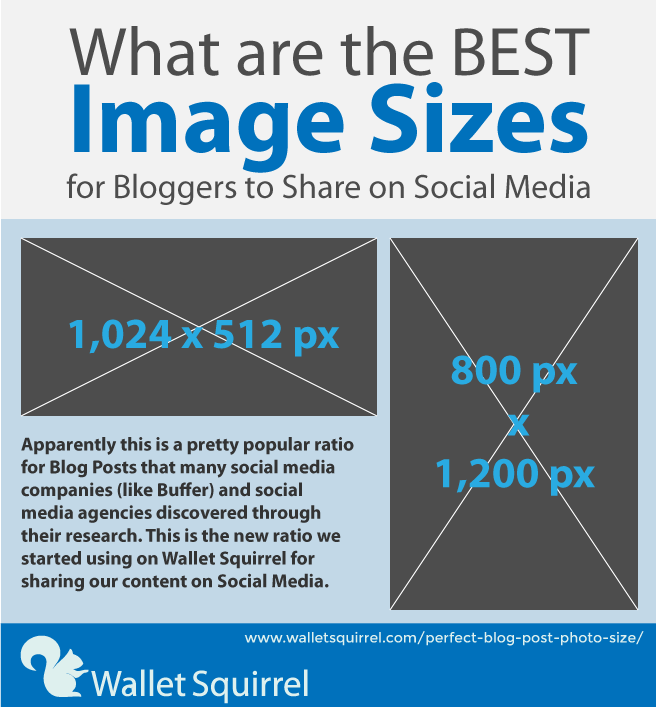

Oh my goodness, blog post photo sizes were SO confusing before I wrote this post. If you look through our older posts, they were all over the place because we made what looked pretty at any size. Now we have the data on the perfect blog post photo size for sharing on social media.

The Perfect Blog Post Image Size

Forget burying the lead, the new dimensions we’re using for our future blog posts are:

Horizontal – 1,024 x 512 px

Vertical – 800 x 1,200 px

Quick article right? Keep reading if you want to know how we came to this perfect ratio of social media and blog magic.

Apparently, this is a pretty popular ratio that many social media companies (like Buffer) and social media agencies came to through their research. I’m focusing on the ideal image size for sharing articles and photos, but if you want the ideal image size for every social media photo spot like profile photos and cover images, check out Omnicore Agency’s infographic.

We Did the Math: Ideal Image Size by Social Platform

I’m focusing on the 4 major social media channels, Facebook, Twitter, LinkedIn, Pinterest. Yes, there are Instagram, Google+, Tumbler, etc. Yet most bloggers don’t use these because they’re not great platforms for sharing articles, images and posts. So we’ll focus on the big 4.

No matter what size you actually upload to any of these platforms, it’ll automatically be scaled to whatever social media platform you’re using. Here is what they scale to.

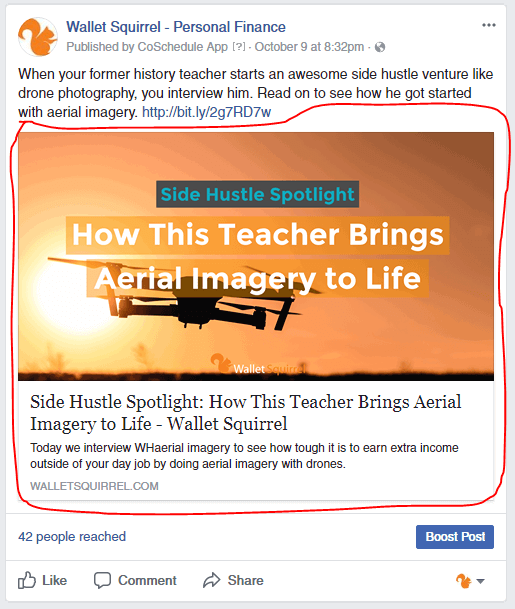

Facebook Shared Link – 1,200 x 628 px

Whenever you add a URL to Facebook, it will create a “shared link” post. This will add your message in the text box above and below use the URL you submitted to automatically a Facebook article that uses your featured image as the post image. It’ll look like this:

To get the most out image size (bigger is better) out of your shared article link, you’ll want your Facebook photos to be 1,200 x 628 px. If most people find you via Facebook, maybe it’s worth making all your blog post images this size to get the most image dimensions and Facebook real estate.

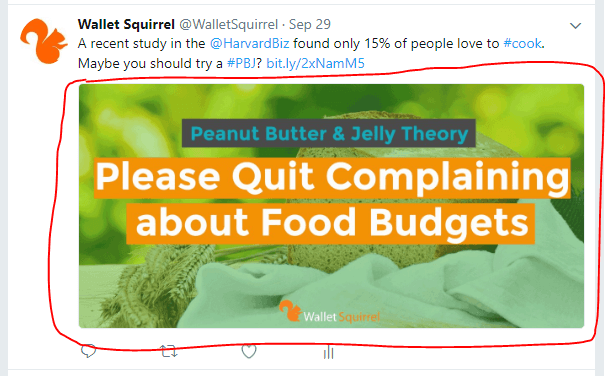

Twitter Shared Link – 1,024 x 576

Twitter has over 313 Million active users a month. If you’re not on twitter you likely don’t exist. So if you want to exist on Twitter, you REALLY need to use images to convey your ideas and share your articles. Tweets with images get 2x more engagement than those without.

If your adding images to your tweets you want to use the right sized images to get the most real estate for your tweets because a regular tweet only last 18 minutes. Twitter uses a 2:1 ratio and 1,024 x 576 px is ideal. This is what the photo will look like when it’s selected otherwise, Twitter will minimize it to 506 x 253 px in the Twitter stream looking like this:

LinkedIn Shared Link – 552 x 368 px

Unlike Facebook and Twitter, LinkedIn will only allow you to add one image per post. So you can get creative having one image made up of multiple images or use one good image. Either way the ideal ratio for LinkedIn according to a moderator on LinkedIn’s help forum, the ideal size for image uploads is 522 x 368 px.

Anything larger than that will be automatically cropped for the image preview to fit their maximum width and height. Your actual image won’t be cropped if selected for full view, but most people only look at the image preview.

Pinterest Shared Link – 600 x 900 px

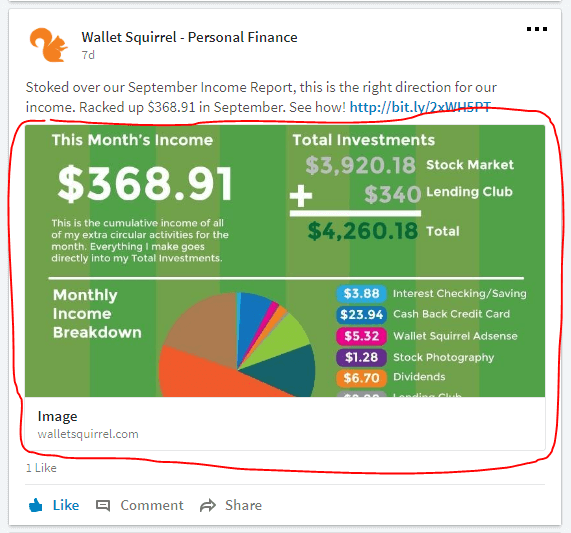

People are regularly raving how great Pinterest is for driving traffic to their website. I’m hoping to try this as stated in my recent income report because 90% of Pinterest pages are external links to people’s websites.

Pinterest has said that the best aspect ratio are images with a 2:3 ratio. This could be 600 pixels wide by 900 pixels tall or 800 pixels wide by 1,200 pixels tall. You get the idea. However, the actual Pinterest feed on the main page and on boards shows pins with a width of 236 px and adjustable height.

Conclusion

We’re going to start using the perfect blog post image size to help us get more real estate from social sharing, what image size do you use for your blog post images?

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Ultimate Lottery Guide – What to do if you Win the Lottery

After the recent big lottery wins, people have been searching for what to do if you win the lottery. The odds are only 1 in 175 million, but it has to happen to someone right. Everyone imagines it and it’s fun to think about, but if it actually happens, here’s what to do according to the Ultimate Lottery Guide.

1. Sign your Ticket

Many people buy Lottery Tickets and stash them in their wallet or purse knowing that it’s their lottery ticket. However, a Lottery Ticket is only owned by whoever has signed the actual ticket. So ALWAYS sign your tickets when you get them. It confirms ownership and the ticket must be signed in order to claim the lottery winnings anyways.

2. Tell No One

It’s big and wonderful news, but you need to think ahead to all the potential long lost relatives, friends and random people that may soon be sitting in your front yard wanting to be your best friend. You don’t want to be the bad person telling everyone “no” so avoid the awkwardness and tell no one. In 1984, Lottery Winner Mike Wittkowski received more than 1,000 letters at his home from strangers trying to tug at his heartstrings to receive money.

It might be fun initially to have 15 minutes of fame, but you may regret it months or years later when people you never met are ringing your doorbell. Stay quiet about it and don’t tell anyone until you come up with a plan with your financial team. The plan should deal with how to handle friends/family/strangers request for money and how to deal with the sudden fame/money.

3. Take Your Time

There is no rush to turn in your ticket during all the hype, you have between 90 days to 1 year from the day of the drawing to turn in your ticket. Each state is a bit different so check them out. You have some time to take a breath, let the hype die down, and get your team of financial experts together before you claim your prize.

Powerball, you have 90 days to 1 year to claim your prize depending on the state via Powerball’s website.

Mega Millions, you have 180 days to 1 year to claim your prize depending on the state via Mega Millions website.

4. Seek Financial Advice & Hire Finance Professionals

Hiring the right professionals will help you collect the most money from your lottery winnings, help understand tax rules and take care of the gritty details so you don’t have to. Like will you take the lump sum of cash or 30-year annuity? Consider these financial professionals for your finance team.

Financial Planner – They will help you set up a plan for your new wealth. They’ll help you understand the benefits of taking the lump sum versus annuity and they will work with you to set up your goals, analyze your assets and set up a budget so you can make the most out of your money and not blow it. A study of lottery winners in Florida found 70% of winners spent all of their lottery winners within 5 years of winning. Don’t be one of these people, consult with a financial planner. To find a good Financial Planner check out the CFP (Certified Financial Planner) Board for a list of Certified Financial Planners in your area.

Tax Attorney -There will be a lot of tax (state taxes/federal taxes/gift taxes/corporate taxes and other taxes) issues that come up about Lottery Winnings. Hire a good lawyer to help you with this. To find a good lawyer, check out the reviews on LegalZoom, RocketLawyer, LawTrades and Avvo for lawyers in your area that are highly recommended and have experience handling large sums of money.

To give you an idea, the government will withhold 25% of your winnings before you even touch it. Then, of course, you’ll have to pay State Taxes as well. Maybe even Municipal Taxes depending where you live. The rest is paid at tax time where the IRS will tax you in the top income bracket at 39.6% (source). In the end, you’ll be taxed nearly 40% on those initial winnings depending on your state.

Accountant – This is the person who will have a good idea how much of the lottery winnings you’ll need to set aside to pay off all the taxes. They will help plan throughout the year on the best ways to mitigate taxes and keep the most of your money. Plus with that amount of money, you’ll want someone handling all your taxes for you. To find a good Accountant, check your local Society of Certified Public Accountants directory to find a certified Accountant to help with your needs.

Estate Attorney – They will help you with structuring and protecting your assets. They assist people in drafting and implementing legal documents, such as wills and trusts. It’s good to have a plan for your assets in the event of your death. Who will your money go to and/or should a trust be set up for your heirs. As mentioned with finding a good Tax Attorney, check out the reviews on LegalZoom, RocketLawyer, LawTrades and Avvo for lawyers experienced with wills, trusts and large sums of money.

5. Claim your Prize – Anonymously

Here’s the deal, Big Lottery wants to promote you and share with the world that a real, regular person won the lottery. Often times state law mandates sharing your name with the public. However, you can claim your prize anonymously a couple of different ways.

6 States allow you to remain anonymous – Delaware, Kansas, Maryland, North Dakota, Ohio and South Carolina.

4 States allow a trust to claim your prize – Colorado, Connecticut, Massachusetts, and Vermont will allow a trust, usually, a trustee (typically a lawyer) to claim the prize without disclosing the name of the lottery winner.

2 States allow you to remain anonymous IF – Illinois and Oregon have made exceptions to making lottery winners names public if the winners demonstrate a high risk of harm by revealing their name.

If you’re not in one of these states that allow you to claim your lottery winnings anonymously. Do what this guy did and hold the check over your head when you receive the lottery winnings.

You can also sign your first name with your first initial to make it harder for people to track you down.

You may also want to get off social media like shut down all your accounts if you win the lottery. This may sound extreme, but keep in mind that people will start searching for you online, going through all photos, friends, where you work and personal details. They may try to stake out at your favorite bar or harass your friends to meet you.

6. Create a middle man for money request

If people hear about your new winnings, you’ll likely have people from all over asking for money. Addressing all of these can be overwhelming and potentially depressing. Consider setting up a middle man to say “no” for you.

When a long lost friend comes out of the blue asking for money, or with a really great investment idea. Send them to your “middle man”, usually a lawyer, who could review all potential investments for you. You can say that they are better at investing than you, which may be true. So they can say “no” and you don’t have to feel bad telling your friend or anyone no. This will save your sanity and emotions from being the bad guy and help not waste your time/money on bad investments.

7. Pay Off All Your Debt

If you do anything with your money first, it should be paying off all your debt. You are entering a new phase of your life and it should be started off debt free.

Even if you go broke in a couple years, you’ll least have all your debt paid off to pick up your life where you started off.

8. Avoid Sudden Lifestyle Changes

While you shouldn’t be doing anything until you can physically hold the money, even after that you should avoid sudden lifestyle changes for the first 6 months. Buying that Ferrari or Land Rover, second house for your entire family, extravagant vacations can all feel like a nice reward for all your hard work, but these impulse buys could quickly deplete your lottery winnings.

Consider instead renting an apartment in that cool neighborhood you want to live in or doing an exotic car rental for a day to try different sports cars. It’ll take you awhile to understand what you want. Find out what really makes you happy before you go on a spending spree and work with your financial planner to set a budget for frivolous things to buy so that you’re still maintaining a nice nest egg for your family in the future.

9. Live within a budget

Ideally, you should only be spending the interest you’ve made off the lottery winnings. If you do this, you’ll never run out of money. The annual interest of a $100M or more lottery winnings will be more than enough to live off of the rest of your life. Especially with a good financial planner.

Otherwise, work with your Financial Planner to set up a budget live within and understand how long your money will last with your current spending habits.

10. Protect your Assets

Consider getting Liability Insurance to help with potential lawsuits against you. With your newfound money, you will be a target for anyone wanting your money. Liability insurance will help for trip-and-fall lawsuits, personal injury claims against you like libel and slander, and freak accidents. This provides an additional layer of security.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Growing Twitter followers organically is NOT easy. It is a hard, grueling process, where we just reached 500 Twitter Followers but we could have done it so much easier and faster. Here is how we reached 500 twitter followers and lessons learned for the next 500.

First, 500 Followers isn’t THAT impressive

I’m not saying reaching 500 twitter followers is the best you can ever do. It’s just a nice milestone I would like to highlight as I tweak my Twitter strategy. Some of the top Twitter stars have MILLIONS of followers on Twitter.

For example, some of the top Twitter Influencers like Katy Perry has some 99.5 million, Justin Bieber at 96 million and Barack Obama closes in on third at 89 million (source).

Obviously, I am not an ex-president or pop singer, so I’ll stay within the Personal Finance world. Which among them, most Personal Finance Bloggers I’ve seen on average have around 1,500 Twitter Followers. Wallet Squirrel is 1/3 way there!

What I learned getting to 500 Twitter Followers

I am still fairly new to Twitter, so I did a lot of research to understand what Twitter was about and how people are gaining mass followings. Here are the top 20 things I learned from research and experience.

1. Get a Schedule Tool like Buffer or HootSuite to schedule tweets when you’re not around. Tweeting consistently will tell your audience that you’re engaged and visible. I use Buffer and love it.

2. Start following other people in your niche, or who you’re interested in. People feel obligated to follow you if you follow them. Following someone is providing value to them, and people typically want return that value to you. However if you’re following someone Katy Perry, she’ll likely not follow you back. I’m still waiting on Taylor Swift…

3. Regularly Retweet others content. For the same reason as above, people typically feel appreciative when you Retweet their content and will likely follow you since you have similar tastes.

4. ALWAYS add photos in your tweets, it’s regularly proven that tweets with photos are engaged by more readers than plain text. People like photos, use a gif and get even more engagement. I personally don’t always use gifs, I’ve learned photos work just as well. I just make sure to use some type of graphic.

5. Use the Hashtags! That’s the point of Twitter, people can follow certain keywords and your tweet may be among them. Twitter shows you the popular keywords if you want to hop on a current event, otherwise sometimes making up funny hashtags reaches a more engaged audience.

6. Sometimes just ask for a Retweet, it seems silly but people who enjoy your content are happy to help you out if you ask.

7. Don’t use a logo as your profile image. Twitter is a conversation platform, people engage more with people’s faces as profile photos rather than faceless logos. I just updated my Twitter Profile Pic.

8. Promote your Twitter account on your other social media platforms and blog. While Wallet Squirrel’s Twitter is 500 Followers, Facebook actually brings in the most traffic for us monthly. So we can ask our Facebook users to follow us on Twitter every once in awhile.

9. Reference people/companies from your blog posts in your Tweets. We get way more engagement when we specifically reference people in our Tweets. Usually when I comment on other people’s blogs, I’ll send out a Tweet referencing them saying nice article. I did this in “What I Learned from Commenting on 30 Blogs in a Week“.

10. Use Follow Buttons on your website so people can share your content. So far NO ONE has done this through our page buttons, but maybe in the future. I’m on the fence about this one, but maybe when we get more traffic.

11. Tweet Inspirational Quotes from Warren Buffett or your favorite philosophers. It seems silly, but sometimes it hits someone right when they’re feeling down. I need to do this more.

12. Pin your best tweets to the top of your Twitter Profile. When new users look at your Twitter Profile, they’re going to look at your top tweets to see what kind of personal tone you use. Pin your best tweets up top to give the best impression. I’m going to try to pin my monthly Income Reports up top.

13. Ask your email list to follow you on Twitter. This can be a simple “PS please follow me on Twitter so I can have more follower than my mother” comment.

14. Tweet the same content multiple times. Each Tweet last 15 seconds on average and then disappears forever. What if your perfect audience wasn’t reading at that time? Retweet messages that you think are beneficial. Some of the top Twitter influences do this all the time.

15. Always reply to tweets that reference your or direct messages. If someone takes the time to mention you then you should give them some kind of thank you or recognition. It’s polite and really well received in the community. I try to thank everyone publically who retweets my tweets.

16. Always thank users for Retweeting your content. I mentioned it above, but it deserves its own line item.

17. Don’t send a massive amount of tweets in a short period. If your tweets are filling up people’s entire screens over and over, they’ll get aggravated and unfollow you. You should constantly be tweeting but spread them out.

18. Don’t stop Tweeting. People who regularly tweet are considered to be more engaged and get more followers than those who tweet once every two weeks.

19. Tweet snippets of your articles. Instead of tweeting “5 Ways Millennials Waste Money”, you should break it into 5 different tweets each sharing 1 of the reasons. Giving value in your tweets is better than taglines any day.

20. Be a real person. Don’t spam your Twitter account with “READ THIS” and all of your stuff to read/sell. Remember that you’re talking to real people. Use words and tones as if you were talking to a group of your friends. People WILL notice.

My Short Failed Twitter Experiment

In February I told myself that I would tweet 16 tweets a day for a month to see what would happen. In February I had previously sent 111 tweets, had 338 Twitter Followers and was following only 29 people.

I did 2 weeks of it until I was exhausted. I only sent out my own tweets and it was all promotions garbage. I hated every second of it. So I cut back to 5ish tweets a day and started a mixture of retweets, some promotional content and new content. I told myself I would do this until I got to 500 Twitter Followers and reevaluate if Twitter is worth it.

It took 4 months, ugh. Growing Twitter Followers is hella hard.

Today I’m at 513 Twitter Followers (151% increase) having sent 646 Tweets (581% increase) and now following 184 Twitter Followers (634% increase). Calculating the math to it, it seems like the increase in people who I follow had a significant impact, related to lesson #2.

Conclusion

While I originally went into this experiment hating Twitter, I’ll admit it’s grown on me. It’s an effective communication tool for short concise messages. I can’t knock that.

During the last 4 months of focusing on Twitter, I’ve learned a lot. So I’m daring myself to get to 1,000 followers in the next 4 months. Think it’s possible?

Lol Not with my current stats. I’ll have to up my game and stick to these 20 lessons learned. Any additional suggestions?

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!