Gross Monthly Income is basically the total compensation you receive for a given month before all the open hands of life take their share (looking at you IRS).

Gross Monthly Income Is All Your Income Before Expenses & Taxes

Let’s say you have a full-time job. When they presented your salary of $60,000 a year, that was yearly gross income, or $5,000 monthly gross income ($60,000 / 12 = $5,000). You never actually receive $60,000 in a year. Your employer takes all the taxes out for you before you receive any of that money.

You have Federal Income Tax taken out, potentially state and local taxes, as well as FICA, Medicare, and other deductions, such as 401k deductions and deductions for your medical plan. After all of those deductions, you get your NET income, which is money that actually hits your bank account. If you are hourly, to calculate your gross monthly income, you first need to multiply your hourly rate by how many hours you work a week, then multiply that by 52 (number of weeks a year) and divide by 12 (months per year).

Gross Monthly Income = All The Money You Make You Make In A Month

Net Income = Gross Monthly Income – Taxes – Expenses

If you are self-employed or have side income, Gross Monthly Income would basically be everything you earned, in total “revenue.” I add revenue in parentheses because if you have a side hustle or business where you sell stuff, Gross Monthly Income would be AFTER you deduct the cost of those items or inventory (Officially called Cost of Goods Sold, or COGS).

Lots of Little Taxes To Be Aware Of

But wait! That $5,000 is unlikely to be your total Gross Monthly Income. If you have a savings account, you might have 1099 interest income (even in this paltry rate environment). You might also have a brokerage account where you had capital gains and side income from your part-time Lyft driving. To add to that, let’s say you got a $2,000 bonus at work and $1,000 for referring someone to your apartment building in the same month. Those items would then be added to the pool that is your Gross Income and would be subject to taxes and other deductions.

For example, this year, I opened an account at Schwab and CitiBank because they offered account opening bonuses. This resulted in me receiving $1,200, which would be added to my gross monthly income for the year. I will most likely get a 1099 early next year, which requires me to claim the income on my taxes.

People Use Gross Monthly Income To Sound Impressive

So, when you hear about people trying to increase their monthly income by working on a side hustle such as walking dogs or consulting work, they are trying to increase their Gross Monthly Income.

Think of it as a bucket that all of your sources of income flow into, and then holes in them that are taxes, deductions, spending, etc. Someone may make a gross monthly income of $20,000 in a month and brag on social media, but if their expenses are $19,900, they only made $100.

Many times, especially in our social media and the comparison-obsessed world, we look at a YouTuber, blogger, or “side-hustler” earning something crazy like $20,000 per month, and you think to yourself, “Wow! That’s like 5 times more than I make” Well, that $20,000 is their Gross Monthly Income. Then they pay a host of fees, share profits with their platform, and are on the hook for their own expenses, such as buying their own technology and professional subscriptions. Further, freelancers are typically responsible for paying their own health, dental, disability, vision, and other insurance fully out of pocket. I have a friend who owns her own graphic design business, and she pays $1,150 per month for health insurance, and that’s with a $5,000 deductible!

This isn’t to dissuade you from working for yourself or having a side hustle; it just shows you that the numbers people throw out as their gross monthly income can be misleading, especially when you are an employee comparing yourself against them. The grass isn’t always greener on the other side; there is always more to the story.

Reduce Taxes to Increase Gross Monthly Income

While it’s generally true the more you earn, the more you will owe in taxes, there are steps you can take to increase your take-home or net pay. Gross Monthly Income can be increased in ways mentioned above, such as working a second job part-time, having a passive income stream, receiving dividend income, etc. If you can maximize retirement savings accounts available to you, depending on your age and income limits (401k, deductible IRA, SEP IRA if you are self-employed), this will reduce your taxable income. If you can contribute to an HSA, FSA, or other pre-tax employer benefits, this will also help. For business owners, the options are even more copious. To reduce their taxable income, they can deduct mileage on their car, cell phone, internet, and many other costs.

Employers Calculate Taxes For You, Side Hustles Do Not

The other thing to keep in mind is to stop yourself from mental accounting. If you earn a total of $5,000 per month from your job, those taxes and deductions have already been taken out by your employer.

On the other hand, money paid by side hustles is gross. So if you earned $5,000 from side hustles, don’t think, “Woohoo! I can take that vacation trip or pay off the $5,000 credit card bill with this money”. Because that $5,000 is before taxes. You need to set some of that money aside for the IRS for the inevitable year-end taxes. You don’t want to get in trouble or end up in collections with the IRS, which will open a whole can of worms that will be hard to close.

Suppose you do not properly save enough of your gross monthly income for taxes. Luckily, the IRS does have a payment plan that you might qualify for but don’t rely on it. The best thing to do is to use a booking service like Quicken to help you set a portion of self-employment income, or even better, work with a CPA to help you structure a plan that not only keeps you on top of your taxes but maximizes your tax-efficiency as well.

Wrap-Up, Gross Monthly Income is All The Money You Received In The Month Before Taxes & Expenses

So, now you know how to calculate your gross monthly income and how to increase it. Don’t let the thought that the more money you earn, the more taxes you have to dissuade you. True, it can kick you into a higher tax bracket. However, you need to take a look at what deductions and credits you can take advantage of.

Lastly, I am not a tax professional, so make sure you consult with your own tax person about your personal income situation.

Let’s start by saying that asking for a raise is a perfectly normal part of business life. It’s business 101 for managers. Yet, for employees, the idea of asking and affecting the status quo of your employee/manager relationship fills many people with anxiety-inducing paralysis.

Let’s destroy the “You vs. Them” dynamic and learn how to get your manager on your side when learning how to ask for a raise.

How to Ask for a Raise

First Things First – Prepare

If you are asking for a raise, you control when you ask. You have time on your side, so start doing your research and build your confidence.

Know Your Worth – Go through your responsibilities at work and ask can anyone else do this? Are you more uniquely qualified for essential tasks that set you apart? If they fired you tomorrow, what would it take for your employer to replace you? Take an objective look at yourself as how your employer sees you.

Create A List Of Accomplishments – Since your last raise, what have you accomplished? Did these accomplishments set you apart or go above and beyond your everyday responsibilities? Having this list of achievements could be key talking points. If your actions are helping improve the company’s productivity or increasing revenue, like starting a company blog, there should be more than a “good job.”

Use The Internet To Find Similar Salaries – Sites like Glassdoor and popular job boards regularly post salaries of similar positions in other companies. This easily accessible information can be a huge talking point in meeting with your manager. If your salary is lower than the listings your finding, your manager’s discussion should be on how to increase your salary to industry standard. Suppose your salary is higher than the industry average. In that case, you should be arguing how your responsibilities justify a higher pay or discuss title changes to put you in the next higher bracket.

When preparing for asking for a raise, try explaining what you do, your worth, and your accomplishments with a friend. If you can adequately explain what you do to a friend, you’ll be more prepared to explain it to your boss during your salary meeting sufficiently.

The Best Time To Ask For A Raise

Often people talk themselves out of something by saying it’s not the right time. However, when asking for a raise, anytime is the right time, after 12 months from your last raise.

Annual performance reviews and raises are ordinary meetings. If that’s not normal for your company, you should set up a yearly review with your manager to get feedback and create a forum for these discussions.

Particular Circumstances When To Ask For A Raise

After Completing A Big Project – If you just completed a big project, and it went well. It would help if you leveraged that win. It’s often a time to discuss bonuses or raises while spirits are high. It’s ingrained in humans to reward good behavior. Use that!

When Your Manager Is Happy – You will always get farther with happy people. However, when approaching your manager about a raise, make sure they’re happy with you and not simply happy about winning a golf tournament.

Set Up The Meeting

When you decide to ask for a raise, remember this is something you’ve been thinking about, but for your manager, it’s out-of-the-blue. If you ambush your manager, they may have a gut reaction to “NO” because it’s their job to maintain the status quo.

One of the more successful ways we’ve seen people approach their managers about asking for a raise is to start with an email to schedule a time to discuss, along with a few key arguments. An email is a controlled way to establish a future time to discuss salary, state a couple of big wins since your last raise, and most importantly, provides your manager time to mull over the idea.

Another benefit to sending an email to set up a time for a salary discussion is that you have the time to perfect the email. Take your time and make it concise. No need to send your manager a short novel on every reason you deserve a raise.

The primary goal of your email is to arrange a time to discuss your salary in person. A secondary goal is to mention your accomplishments, which you should only list 1-3 of these to keep the email concise.

Tips For Your Salary Meeting

Salary meetings don’t need to be adversarial. But rather a collaboration with you and your manager to get you to a salary you want. Here are a few tips on successful raise requests:

Don’t make it into a presentation – Your manager should already be aware of your accomplishments by working with you or highlighted them in your earlier email. It could be a simple paragraph “Hi! I wanted some time to discuss my salary as we haven’t met in over 12 months. According to Glassdoor and our competitor websites, here is the average industry salary for people in my position and responsibilities. I want to discuss how to get my salary closer to the industry average.”

Be Confident and Specific About Your Raise – Based on your research; you should have a specific number in mind to match similar positions at different companies. This number shows your manager you’ve done your research and gives them a firm number to work. Perhaps your number could be a little higher so you can negotiate down if needed.

Practice What You’re Going To Say – They say TED speakers practice 200 times before they present. For a compensation meeting, it’s more complicated because you don’t know how your manager will respond. However, you can still rehearse the main points with polish, such as “Why A Raise Now?”, “Why You Feel You Deserve A Raise?”, “How Can I Justify A Raise To My Boss?”.

If They Say No, Here’s What To Do

In the worst-case scenario, they say “no,” and that’s ok. The simple request of asking for a raise is a huge step in the right direction to increasing your salary. Here are a few tips if they say “no.”

Don’t Create An Ultimatum – Don’t force yourself into a corner by saying, “I’ll quit if you don’t give me this raise.” A manager may not have the resources in their budget to give you a raise. Then either quit to keep your word or lose credibility by staying. It’s best to ask for their reasoning and if you don’t like it, secretly start applying for other jobs.

Create A Plan For Another Raise Discussion in 6 Months – If your manager feels they can’t give you a raise right now, you should together set a hard time in the future to continue the conversation. This meeting gives you something to look forward to, knowing the conversation isn’t dead. Maintaining hard dates to continue a salary discussion keeps it top of mind for your manager. Remember, it’s always the squeaky wheel that gets cleaned.

Discuss Other Benefits That Can Make You Feel Rewarded – Perhaps there isn’t money in the budget to accommodate a raise right now. Other benefits may help you feel rewarded for your work.

Additional Vacation Time – Time off is a freedom that can be as beneficial as money. This benefit is sometimes far easier to grant employees when a raise isn’t in the budget.

Title Change – If your company can’t afford a raise, a title change may be a compromise. It’ll give you more prestige in your field and open up further salary increases down the road with a more prestigious title.

Work From Home Options – If more money isn’t an option, maybe you can work some of your hours at home. Working from home gives you additional freedom of spending time with your family and that time is priceless.

Make Asking For A Raise A Normal Thing

A raise shouldn’t be a “You Vs. Manager” ordeal. It’s a collaboration between you and your boss to give you’re the resources to feel appreciated for the job you’re doing. No manager wants to be the bad guy saying “No” to your raise, so find opportunities to work together to increase your salary to the industry standards you find on Glassdoor and adequately reflect your responsibilities.

For many people, asking for a raise is a terrifying experience, but it’s essential to know that raises are a normal part of business life. The mystery lies behind the closed doors where these discussions occur. Both you and your manager play their cards close to their chest while everyone wants to maintain the status quo. If you follow these steps, and with a bit of practice, you will master asking for raise.

There are always ways to make money outside of work, but asking for a raise is one of the easiest ways to make more money.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

One of the most significant determinants of what kind of car you will buy is your budget. So many people wonder how much car can I afford.

A good rule of thumb is not to exceed 10% of your take-home pay on a car payment.

If you are paying cash instead of financing it, setting your budget to a vehicle that would have cost 10% of your take-home pay for a car payment is also a good idea. This way, you are not depleting your resources by buying a car that takes up too large of a portion of your total wealth.

2. Your Needs

Your vehicle can be a critical component for your job or side hustle. Therefore, it is essential to consider how far your commute is, and if you drive it during your work, this becomes even more important.

3. How Big does it Need to Be?

Do you need a vehicle to carry around multiple passengers? Do you need space for hobbies?

As a general rule, everything is more expensive with a larger car. Even the tires are more costly for a higher weight rating. So you will want to take into account how often you will be carrying multiple people or extra gear with you. For example, do you need an SUV rated for eight people when you have a family of four?

4. Fuel Economy

It would seem that fuel economy is often viewed with too much importance or not enough importance when purchasing a new vehicle. Usually, fuel economy is at the top of the list of important factors when buying a car or barely makes the radar.

The reality is that fuel economy can impact the total cost of ownership of your vehicle. To get an estimate for the cost of fuel on your car, you can look at the mileage on your current vehicle, subtract how many miles were on it when you bought it, and divide by the number of years you have owned the car. Once you know the average miles per year, you can divide by the average mpg of the new vehicle and multiply by the current price of fuel.

For example: if you have driven your current vehicle 65,000 miles in 5 years. That is 13,000 miles a year, or 65,000 divided by 5. If the new car you are looking at gets 25mpg, it would burn 520 gallons a year or 13,000 divided by 25. If the gas price is currently $2.75 a gallon, you would be paying $1,430 a year in gas for the vehicle, or 520 times 2.75.

In comparison, a car with 35 mpg would cost $1,021 a year in fuel. The result is over a $400 savings. Over five years, this will amount to $2,000 in fuel consumption.

5. Amenities

With vehicles, there are tons of trade-offs. Getting more amenities within your budget will likely mean getting a smaller car. The practical advice would be to get the best platform you can afford and skip the amenities. That would likely lead to buyer’s remorse, and you will be right back in the dealership looking for a new car in short order.

My advice is to figure out which amenities will make you feel good about your car. Don’t prioritize ones that will feel good to show off to your friends because that won’t last. In a year or so, they will be old news. You shouldn’t need all the bells and whistles to feel good about your car. Warren Buffet purchased the most basic Cadillac they would sell him.

It is ok to prioritize features that will enhance your driving experience. For instance, adaptive cruise control makes driving less fatiguing and road trips more enjoyable.

6. Edge Cases

A little consideration you should make will be edge cases. One example of an edge case would be to haul lumber or large items that you would infrequently order. It may be convenient to have a large vehicle to accommodate these cases, but it likely would be cheaper to pay the store to deliver the items.

7. The Future

How will your needs change over time? It is prudent to plan on keeping a vehicle for at least five years. In that time, are you planning on having children? Do you think there is a possibility that your job might change? Do you think you will want to start a side hustle that relies on driving around? All of these things can impact which vehicle you should choose to drive today.

As the price of fuel fluctuates, it can have an impact on your budget. If you purchase a vehicle that is not fuel-efficient, the effect on your budget will be much more significant. The psychological cost at the pump will also go up because when your fuel costs are impacting your whole budget, remembering how bad of gas mileage your vehicle gets will sting.

It is all will about reducing buyers’ remorse. The transaction cost of switching vehicles down the road because you are not happy with your decision will cost more to your overall wealth than even whether you got a “good deal” or not when purchasing the vehicle.

8. Style

You will be spending a considerable amount of time in your car. If you are not going to, then it is probably time to re-visit the decision of buying a car at all.

People think of their cars as an extension of their identities. For better or worse, this seems to be the truth of the matter regarding vehicles. If you

9. Electric or Not

Should you buy an EV or a gas-powered vehicle? There are a few questions to consider for this.

Do you routinely drive further than the EV’s range?

Can you charge your car at home?

Do you qualify for tax credits?

What will the fuel savings be?

After answering those questions, the pros and cons of an EV should be a little more clear to you. At the end of the day, it will likely come down to preferences. It is hard to tell what the future cost of gas will be over the next few years.

Any trip you have to make that is longer than the EV’s range will be a little more complicated than a gas vehicle.

10. Latest Safety Features

With innovations made over the years from crash testing, the field is a lot more even than it once was for physical performance during a crash. However, there are many advances in technology for electronic safety features.

Some of these features are blind spot detection, lane assistance, coll

I know I have benefitted from cross-traffic detection when backing up my minivan before. The cameras could detect oncoming traffic where it was in my blind spot. Even if the scenario would have otherwise resulted in me slamming the brakes after backing a little and seeing the traffic, being alerted before I even saw the oncoming traffic reduced stress.

11. Get Pre-Approved for a Loan

When you walk into a car dealership, there are so many variables at play. Which car is the right one for you? How much car can you afford? Can you get financing at a reasonable rate?

By getting pre-approved for a loan, you can answer your budget questions and get suitable financing before you ever step into the dealership. You don’t have to tell the car dealer you have been pre-approved for a loan either. That way, you can see what they offer you as well. FICO dictates that it counts toward the score as one pull if your credit is pulled multiple times for auto loans in 14 days.

Another advantage to getting pre-approved for a car loan ahead of time is that it will allow you to correct potential errors with your credit score. For example, if you apply for a loan and tell you your FICO is much lower than you expected, they will provide you with a copy of the credit report. Then you can look into getting these things fixed.

If you were at the car dealership in their finance office after you have agreed to purchase a car, there is a high chance you will take an alarming rate to continue with the deal.

12. The Test Drive

Test driving a car will give you a better opportunity to understand what it is all about than any stats on a webpage or photos of it could ever do.

When you narrow your search down to 3 different cars, call the dealerships up and schedule a test drive for each of them on the same morning. The morning is better if at all possible because the dealership will not be as busy.

After the Test Drive

After you have done the test drive, you should feel much more confident that the car is the right pick for you. Since you are pre-approved for an auto loan, you don’t need to negotiate with the dealer. Instead, you can focus on negotiating the price of the vehicle.

Tyler Weaver is a real estate investor and blogger at Relentless Finance (https://www.relentlessfinances.com/). He has flipped over 50 homes and manages a real estate portfolio in the midwest. He strives to help others build wealth and add value to other’s lives through a constant pursuit of growth.

The average college graduate receives $1,847 worth of cash and gifts from family and friends. While it’s tempting to splurge all of it, your future self will thank you for spending it wisely. Don’t worry. With these 12 smart spending strategies, you’ll still be able to treat yourself while learning to be financially responsible.

1. Buy Discounted Gift Cards for Big Purchases

Courtesy Unsplash

If you’re going to make a big purchase like a new TV or laptop, consider buying a discount gift card to save money! Raise is one of many online marketplaces connecting people looking to sell their unwanted gift cards. You can score gift cards at stores you regularly shop in for up to 30% off.

2. Shop Through Cash-back Apps

Courtesy Unsplash

Back in your parent’s day, there were coupons. Today there are cash-back apps. So whether you’re buying work clothes, new electronics, or stuff for your apartment, these apps help your graduation money go further by giving you a portion of your total sale back. Check out Rakuten, Ibotta, Fetch Rewards, and MyPoints, to name a few.

3. Keep Control Over Your Spending

Courtesy Unsplash

While $1,847 is a lot of money, it can be gone before you know it if you’re not careful. Research has found that people tend to overspend when using debit or credit cards. If you’re starting to feel like your spending is out of control, try shopping with cash. You’re more likely to think twice about what you’re buying when you have to count out the amount due, which leads to less spending.

4. Set Yourself Up to Cook at Home

Courtesy Unsplash

Now that your college meal plan is gone, you’re going to find that food will be one of your three biggest expenses. The average American spends over $200 a month eating out! There’s nothing wrong with eating out here or there, but eating out every day and grabbing expensive coffee every morning is sure to bust your budget.

By taking $200 of your graduation money to buy an inexpensive coffee maker, pot & pan set, and other small kitchen items, you’ll be setting yourself up for not just healthy eating but responsible spending year-round.

5. Consider a Season or Annual Pass

Courtesy Unsplash

Are you a frequent visitor to an amusement park, museum, ski resort, or board game cafe? Consider buying an annual pass instead of sporadic day tickets to save money over the course of a year. Ask yourself these 2 questions to determine if you could save money with a season/annual pass to your favorite spots: How many visits do you need to go to break even on the pass cost? Will you actually go that many times? After doing the math, you might find it’s actually more economical to buy a season pass.

6. Set-up An Ergonomically Correct Home Office

Courtesy Unsplash

With work from home here to stay in some form, setting up a proper workspace must prevent painful and costly neck and back injuries. A survey from the American Chiropractic Association reported a surge in neck and back pain since people moved en masse from a home office to working from home.

Consider purchasing an ergonomic keyboard and proper desk chair. To keep more of your graduation money in your pocket, “raise your computer monitor to eye-level with boxes or books if you can’t buy a new desk,” said says Dr. Peter J. Scordilis, a Certified Chiropractic Sports Physician at Scordilis Family Chiropractic. “Whatever desk chair you use, make sure your feet can touch the floor and that you’re reducing stress on your back by keeping your knees at 90 degrees.”

7. Start an Emergency Fund

Courtesy Unsplash

Things are going to happen. Your car will get a flat tire, your phone might break, or your laptop stops working. Adulthood is full of unexpected expenses. Your future self will thank you for saving for a rainy day. Putting some of your graduation money into an emergency fund starts your financial future on the right track. It decreases the need to ask your parents for money or use high-interest credit cards to cover unexpected expenses.

8. Tackle Your Debt

Courtesy Unsplash

I know. Who wants to pay bills? But it’s the reality of becoming an adult. The cycle of debt can cost you thousands of dollars or more over time. It’s time to start paying down any credit card debt you may have incurred in college. Check out the back of your credit card statements to see exactly how much your purchases will end up costing you when you only make the minimum monthly payment.

9. Pay Down Your Student Loan

Courtesy Unsplash

According to the Federal Reserve Bank of New York, the average student loan monthly payment is $393. Before you know it, you’ll be required to start making those payments. Set aside some of your graduation gift money for the first couple of payments to ease into this reoccurring expense. The sooner you pay off your student loan, the sooner you’ll free up that money for other things in your life.

10. Start a Savings Account for Big Purchases

Courtesy Unsplash

Now that you’ve graduated, you’re probably going to want to buy some of those things you couldn’t afford while in school. It might be a dream vacation or a brand new car.

But it would be best if you had a plan. Start a sinking fund in high yield savings account with a portion of your graduation money. Determine how much you need for these things, and then you add a little more to the pot specifically for that expense every month. If your sinking fund meets the minimum requirements for a high yield savings account, be sure to put it there so your savings make a little money for you.

11. Invest in Yourself

Courtesy Unsplash

Now is the time to invest in yourself. The ROI will pay dividends for decades to come. Whether it’s a class to learn a practical skill like cooking or car repairs or a certification related to your career, now’s the perfect time to invest in new skills.

12. Put Your Money to Work

Courtesy Unsplash

After moving into your first apartment, funding your emergency fund, and paying off credit card debt, consider investing any remaining graduation money in the stock market.

Investing is one of the best ways to put your money to work for you, as the number of years you’re investing in the stock market matters. If you start investing $250 a month at the age of 22 and keep investing $250 a month until the age of $65, assuming an annual investment return of 8%, you will have more than $1 million in investments when you retire. Now, if you decide to wait to start investing until you’re 30 years old, well, that final number at age 65 goes down to just $539,088.23. It’s almost cut in half.

Go ahead and open your 401K through your employer or a Roth IRA through a brokerage account. The sooner you get started, the sooner you start making money from your money.

It’s time to take ownership of your finances and put your graduation money to work. You can do it—best of luck, Graduate!

It is very important that you look after your financials and plan for your future accordingly to protect your financial future. There are a few ways you can go about this while keeping in mind the sort of lifestyle you are hoping to achieve and maintain.

There is obviously your pension plan, which you do have to keep one eye on to make sure that it is on track for paying out the kind of money you would like it to. Despite a wealth of free information, like this from the USA Gov website, not many people know enough about their own pensions and what to do to make their financial future more secure.

In addition to this, there are other things you can do to help your financial future be what you want it to be.

Plan ahead

Make a plan of how you want to live in the future and work out the kind of outgoings this will create. Of course, you are unlikely to be able to work out the rate of inflation accurately, though there are places you can go on the internet where a rough guestimate is available. It may give you an idea of the sort of income you will require.

Start a saving fund

Start a saving fund. This can be in the form of another pension or as a separate savings account or other investment, and skim off any earnings you feel you can afford into it. If you are lucky enough to have had a pay rise but could live quite comfortably on the earnings you had before, perhaps putting the difference aside into a savings account may be the first step you need. Alternatively, starting a side hustle and putting the money away can offer the same results.

Make a strategy to pay off debts

Start making a strategy to pay off any outstanding debts or loans. You may find this easier to manage if you consolidate all your loans and credit cards into one, and you may save a bit of money in the process on interest payments. See this article for information on how your credit score could affect you.

Create your plan for retirement

Create your plan for retirement, work out when it is you are likely to retire and how much money you will have by then versus how much money you will want to have by then so you can start working towards your financial future.

Put your plans into action

Putting your plans into action is the final part, though you will have to keep track of how well you are doing and be prepared to change any of your plans as time goes on.

Obviously, there will be a time in life, albeit a short period, for example, where mortgages are paid off but income from employment is still present, when you may find that you have a little more money than previously. Make the most of these times, be money wise and invest what you can for your future.

Final thoughts

The best way to go about your financial future is to plan it out and then work out what you want to happen. Once you have done this, you will be able to work backward to make sure that you hit every goal you need to hit to get to your desired destination.

Your entire life changes the moment you have kids. While most of us understand that becoming a parent will mean less sleep and lots of diapers, we drastically underestimate the amount of kids shows we will watch. Show let’s explore the 9 best Disney Channel shows that us parents won’t hate!

Your favorite shows will be replaced first by cartoons, then live-action kid’s programs, and finally by tween and teen sitcoms. The good news is that The Disney Channel has several kid-friendly shows that parents won’t dread watching too.

Watch these 9 Family-Friendly Disney Channel Shows to Bond with Your Kids

If your family is like mine, one of your favorite ways to relax at the end of a long day is to gather on the couch, turn on the TV and watch our favorite family-friendly shows. And before you start worrying about screen time, you can take a deep breath and relax. Shared viewing experiences, in moderation, can actually be a positive thing.

There are many benefits to watching TV with your kids, including opportunities to discuss your family’s values, having some family bonding time, and turning screen time into quality time with your child.

According to The Child Mind Institute, watching your kids’ favorite show along with them not only “brings you closer to your child at a time when they are becoming less likely to confide in you, but watching together can spark conversations about subjects or issues that they otherwise might not feel comfortable discussing with you.”

Many kid-friendly shows lack storylines or characters that adults can connect with. As a mom of two kids, I’ve had great luck finding fantastic family-friendly shows on The Disney Channel that the whole family can enjoy.

The Best Disney Channel Shows for Families: Sitcoms

While the Disney shows that you knew and loved as a kid, like “Boy Meets World” and “Doug,” are long gone, there are now plenty of series that are ready for the next generation to enjoy. No Disney Channel? No problem! Many of these shows are on other platforms like Disney Plus, Netflix, Prime Video, and the Disney Now app.

Here are nine shows from The Disney Channel that are kid-tested and parent-approved! So grab a bowl of popcorn and enjoy some couch time with your kids.

1. Tricked

Best for families with kids of all ages.

Who doesn’t love mind-blowing magic and hilarious hidden camera pranks? Well, this series combines both of them in one program that your entire family will enjoy. Watch as YouTube personality, and magician Eric Leclerc amazes kids and adults through his magic on the streets of New York and Canada. You’ll be in awe of his creative and amusing antics like floating popcorn, a chalkboard that solves math problems and creating friendship bracelets in his mouth.

2. Raven’s Home

Best for families with kids age seven and up.

This Disney Channel gem stars Raven Symone in a spinoff of “That’s So Raven.” This show shares the story of two single moms, who are also best friends, as they move in together to raise their children. The two moms have very different parenting styles, which pay off when dealing with three kids under one roof.

The show does a great job of incorporating modern challenges to allow families to discuss their values and priorities. Kids and adults will enjoy the hilarious antics and realistic scenarios.

3. Liv and Maddie

Best for families with kids age seven and up.

Liv and Maddie Rooney are teenage twins who are complete opposites. Maddie is a student-athlete, while Liv is a famous actress and singer. Dove Cameron from “The Descendants” fame plays both characters, amazingly. However, Liv and Maddie aren’t the only reason that your entire family will love this show. All of the characters in the series are hilarious and loveable.

The storylines are lighthearted, relatable, and totally entertaining. While Liv and Maddie are the stars of the show, their mom’s character will leave you all laughing hysterically with her comedic delivery.

4. Coop and Cami Ask the World

Best for families with kids age seven and up.

Coop and Cami Wrather are a brother-sister duo who have created the successful online show “Would you Wrather.” The savvy tweens harness the power of social media as they poll the show’s audience with this or that questions to make all of their decisions. From what they will eat for dinner to whether their mom should date the school principal, they always follow through with the results of their surveys. With a strong emphasis on family relationships and friendship, kids will enjoy the show’s events and characters, while the heartfelt and funny content will amuse parents.

5. Just Roll With It

Best for families with kids age seven and up.

Part sitcom and part improv, this family comedy series on The Disney Channel is like no other. The actors on the partially scripted show have arrived to film with their lines memorized in front of a live studio audience. Everything goes along as planned until the foghorn blast, and the audience gets to choose what happens next. No matter what the audience decides, the actors have to just roll with it and make it happen without any preparation.

The scripted portion of the show includes a heavy emphasis on themes that include blended families, step-parents, and other relatable issues that parents will appreciate. The series takes inspiration from “Whose Line Is It Anyway” and “Choose Your Own Adventure” books, and the result is an entertaining and engaging show that you’ll all enjoy.

6. Bunk’D

Best for families with kids age eight and up.

This popular series is the type of show that Disney is famous for. “Bunk’D” occurs at Camp Kikiwaka, where the CIT’s (Counselors in Training) are the main characters in the show. As you can imagine, a kid’s summer camp provides the perfect backdrop for tons of family-friendly episodes covering topics like roommates, rival campers, and mysteries in the woods.

7. Ride

Best for families with kids age eight and up.

American teenager Kit Bridge’s entire world changes when her family moves to England. Her father’s been hired at Covington Academy, an elite boarding school that she now attends. “Ride” is a funny, heartfelt series that focuses on the relationships and challenges that we all face as we navigate changes in our lives. Filmed in an actual castle in Northern Ireland, you will enjoy the scenery as much as you enjoy the series. Chosen by Common Sense Media as one of their top picks for families, this Disney Channel show is sure to become one of your family’s favorites too.

8. Secrets of Sulphur Springs

Best for families with kids age nine and up.

A new original series, “Secrets of Sulphur Springs,” is full of family-friendly mystery and drama. Set in the fictitious town of Sulphur Springs, Louisiana, the show tells the story of middle-schooler Griffin Campbell. The boy and his dad have moved into the supposedly haunted Tremont Hotel, which is full of adventure, including time travel, ghosts, and an unsolved disappearance.

The mildly spooky show has enough suspense and mystery to captivate adults and kids at the same time while avoiding blatantly scary scenes. The veil of secrecy surrounding the story’s events provides a sounding board for discussing the importance of forgiveness and honesty.

9. Sydney to the Max

Best for families with kids age nine and up.

This modern family comedy series follows the lives of tweenager Sydney, single father Max, and grandma (Caroline Rhea) as the three generations navigate life together. The plot follows outgoing Sydney as she struggles to understand why her overprotective dad throws down so many rules and guidelines for her to follow.

Embedded into the show are flashbacks to the 90’s showing Max and his mom navigating many of the same situations that Sydney is currently experiencing today. The show’s premise helps kids see that parents faced the same challenges growing up and that they really do understand what they’re going through.

Conclusion

While parents traditionally tend to avoid kids’ shows due to annoying songs and cheesy actors, these Disney Shows are actually enjoyable to watch together and present a comfortable way for parents and kids to talk about sensitive topics.

With a wide variety of options from sitcoms, mysteries, dramas, and reality shows, you’re sure to find something that your family will love and perhaps become part of your family’s weekly routine.

These were originally written for a trivia night with friends, but they went over so well that I wanted to share with you 37 amusing facts about money you should absolutely know. I will specify, these are money facts about the United States of America currency.

Take a moment to memorize one or two of these facts about money to impress your friends in the future! It might even help you win a trivia night.

1. In the $1 bill, there are lots of secret meanings hinting at the 13 original colonies

You may have never noticed it before but there are lots of little Easter Eggs hidden in the complex design of the $1 bill. They all revolve around the number “13”. (source)

There are 13 steps on the pyramid

13 vertical bars are placed on the shield

There are 13 horizontal stripes on the top of the shield as well

The symbolism continues with 13 stars on the eagle

Extreme detail was used to place 13 leaves and 13 berries on the olive branch on the eagle’s talons. The other talon holds 13 arrows

There are 13 stars above the key on the Department of Treasury seal

2. On the $5 bill, all 50 states are listed across the top of the Lincoln Memorial

However, if you want to read them you will need a magnifying glass. (source)

3. How slang terms about money like “buck” were formed

Here is a breakdown of some of the origins of words we associate with money today. These are often based on historical societies that influenced the way we refer to money (source)

Buck – Back in the day, people used the skin of deer as trade and barter for goods/services. Each skin was referred to as a “buck”.

Fee – this comes from the German word for cattle “vieh“

Shell Out – At one point, Native Americans used shells as currency, and later European colonists adopted the phrase “Shell Out” meaning “to pay”.

Salary – Adopted from the Romans, soldiers at one point were paid their wages in salt. The Latin word for salt is “salarium“. That phrase over time originated “salary”.

Dollar – A Czechoslovakian town called Jachymov minted its own silver coins in 1519, and those coins were called “talergroschen”. The slang or short form of these were called “talers“. This spread across Europe and today, many nations name their currency with some variation of “taler“. For instance, in the United States, we call our currency “Dollars”. Pretty cool right! (source)

4. People underestimate how valuable loose change can be, in 2018 the TSA collected $960,105 in loose change

All that loose change thrown in the bins as you roll through security often gets forgotten and left behind. However, it all adds up and it’s consistently a lot. Making this one of the more impressive facts about money. (source)

2017 – $866K

2016 – $867K

2015 – $765K

2014 – $674K

2013 – $638K

5. One of the grossest facts about money, like bacteria gross

This feels obvious, but something we don’t often think about, “just how many people handle your money before it comes to you…”. Basically, money can contain lots of germs, most of these are harmless but some $1 bills have been known to contain traces of salmonella and E.coli, making this one of the grossest facts about money. However, it seems that older bills (which are cotton-based) usually contain more containments while newer, glossier polymer-based $1 bills remain a little cleaner. (source)

6. The $1 bill is the most circulated bill in the United States

In fact, 48% of the money printed by the US Bureau of Engraving and Printing is just the $1 Bill. Primarily because it is the most common bill, but also because the average lifespan of a $1 bill is just 18 months. Oftentimes you can take a worn-out bill to your local bank and they’ll replace it for you. (source)

7. There is more Monopoly Money printed every year than real money

If you take the combined value of all US money printed each year, it’s between $696M – $974M (most is just to replace old worn money). Yet Parker Brothers reported that the combined fictitious value of their monopoly money, meaning add up all of their orange $500 bills, yellow $100 bills, purple $50 bills, green $20 bills, blue $10 bills, pink $5 bills, and white $1 bills, that combined fictitious value is $30 Billion. That’s with a “B”. So nearly 30x as much monopoly money than US bills created every year. (source)

8. There is an ATM machine in Antarctica

In fact, there are ATM machines on every continent in the world. It just seems strange that there is an ATM in Antarctica. However, there are actually 2 of them. Both operated by Wells Fargo at McMurdo Station, the largest science hub on the continent. That makes this one of the “coolest” facts about money. (source)

9. By law, living presidents can’t have their face on US Currency

This is issued by Congress in 1866, and for the most part, has held true. In the past, usually, only monarchies had the faces of their living presidents. Typically the only time living presidents have been featured on coins is during commemorative coins. George Washington was famous for not wanting his face on US Currency because Kings often put themselves on coins. He thought his face on currency was too much like the monarchy. (source)

10. Benjamin Franklin & Alexander Hamilton are the only Non-Presidents featured on American bills

Mr. Franklin and Mr. Hamilton were important founding fathers of the United States of America, but they are the only non-presidents to show up on US paper currency. Franklin is featured on the $100 and Hamilton on the $10. (source)

11. The phrase “In God, We Trust” wasn’t written on US currency until 1957

The change was approved by President Dwight Eisenhower on July 30, 1956, and put into effect the following year. The phrase actually replaced the previous phrase on US currency “E Pluribus Unum” meaning “One out of many”. (source)

12. The most counterfeited bill is the $20 bill

While the $100 bill is a close second, people are more likely to break a $20 at a store or bar than a $100. Some famous counterfeit money launders took fake $20’s or $100’s to bars during rush hour to buy a drink and pocket the change. While the bartender is rushed, they often didn’t take the time to examine the money too closely. I wouldn’t suggest this though, there are better ways to make money. In the end, most people get caught. (source)

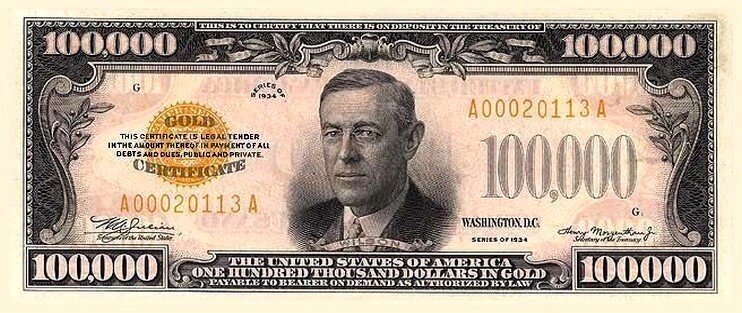

13. There is a $100,000 bill

It’s a gold certificate that features the 28th US President, Woodrow Wilson. However, it was never for public circulation. The Federal Reserve Banks used to use these paper notes to circulate money between the banks. This is one of the most expensive facts about money. (source)

14. The idea of paper money caught on in the 1700s when goldsmiths gave people paper receipts for their gold

At this point in history, most money was coin-based. This started the standard of governments using paper currency as a representative of that government’s storage of precious metals. For the US Government, paper money was representative of the gold supply in Fort Knox. This continued until 1971 when digital currency made the value of money in the world based on “faith” rather than gold. A $20 bill is only valuable because everyone agrees it has value. (source)

15. Digital facts about money, Economists estimate only 8 percent of the world’s currency exists as physical cash

Meaning digital transactions of automated electronic deposits and credit cards transferring funds back and forth are more prevalent than people actually using physical money to pay for things. Think about how much money you spend a month and realize how little of that you’re actually paying with cash. That’s a crazy number to think about. (source)

16. The US Bureau of Engraving and Printing currently only produces $1, $2, $5, $10, $20, $50, and $100 bills

At one point there was a series of $100,000 bills printed but they were only for transactions between Federal Reserve banks. Regular people were not carrying these around in their wallets. The $2 bill is fairly rare, they are only printed by demand and the last one was printed in 2003. (source)

17. The US Bureau of Engraving and Printing produces 37 million notes (paper money) every year!

That is a combined value of $696 million printed every year. Surprisingly, 95% of that money is created just to replace old money. (source)

18. The US. Bureau of Engraving and Printing uses 9.7 tons of ink PER DAY to print money

There are two active facilities used by the US Bureau of Engraving and Printing (Washington DC + Fort Worth, TX) that print money every day and those facilities go through so much ink. Mind you this is high-tech ink with trackable, magnetic, and color-changing properties. (source)

19. Green Ink was originally used to prevent counterfeiting with black & white cameras

It was hard to get the green ink right when people tried to produce photographic copies of the US currency. In 1929 when paper money designs became more standardized and intricate to reduce counterfeiting, the US kept the green ink because they had so much in stock. (source)

20. A single company (Crane and Co.) has always produced the paper to make US currency

Ever since 1775 when Paul Revere used paper from Stephen Crane’s paper mill for some of the United States’ first banknotes. Crane & Co. has been the sole company that has always produced unique paper for US Currency. (source)

21. The original purpose of the Secret Service was to fight money counterfeiting (Protecting Facts About Money)

In July 1865 the US Secret service was formed to fight early counterfeiting at the end of the Civil War. (source)

22. If you want to tear any US Bill by folding it over and over, it’ll take 4,000 double folds

That’s a lot but these things are durable! Composed of 25% linen and 75% cotton, these things take some effort to rip. However, not many people are going to reach the 4,000 fold capacity. Keep in mind it only takes 400 folds before a regular piece of paper breaks. (source)

23. Damaged US currency can only be replaced at a bank if more than 51% or more is attached

If you get a ripped $1 and as long as more than 51% is present, it can be used as legal tender. You can take it to a bank and they will replace the torn currency with a brand new note. You need to have more than 51% so people don’t tear currency apart and turn in two separate notes. This is one of the most “ripped” facts about money. (source)

24. There is more than $1.99 TRILLION worth of federal reserve notes currently in the world

As of April 8, 2020, there are $1.84 Trillion of dollars and coins in circulation. So if you took every US dollar and coin in the world (banks, couch cushions, buried treasure, etc.) and added them all up, it would be $1.84 Trillion dollars. (source)

25. Our money is produced by two different organizations, the US Mint creates coins & US Bureau of Engraving creates paper money

There are two separate organizations that produce the money we use every day. (source)

26. The US Mint produces 30 billion coins every year

The United States Mint creates 1 cent, 5 cent, 10 cent, and 25 cent coins. Plus $1 coins commonly referred to as the Sacagawea Golden Dollar Coin, replaced the previous US $1 coin which was the Susan B. Anthony Dollar Coin in 2003. This is one of the most “coined” facts about money. (source)

27. It cost the US Mint more money to create a nickel than a dime

It comes down to size. The US Mint pays $0.1118 cents to produce a nickel, yet only $0.0565 cents to produce a dime. (source)

28. A penny costs more to make than it’s actually worth

It costs the US. Mint $0.0241 cents to create a single penny. That means it costs double to produce a penny than it’s actually worth! This is why there are many petitions to get rid of the penny because it’s literally a waste of money. This is one of the most well-known facts about money. (source)

29. There are ridges on the edges of quarters and dimes because people use to shave the edges for extra metal

Back in the day, people used to shave the edges of coins to gather precious metals (silver, gold, etc.) and combine those clippings to counterfeit new coins or sell outright. It was called “Coin Clipping”. Eventually, the US Mint started to add ridges to the coins to make it easier to spot and deter counterfeiting. Pennies and nickels were never created with precious metals so it wasn’t worth the effort. (source)

30. People use pennies to stop garden pests (One zapping Facts About Money)

It’s an odd thing but some people swear by it. If you bury pennies in the garden, the copper and zinc in the pennies will generate electric shocks for garden pests. Most people use them to deter snails. Nowadays there is more zinc than copper in pennies. This is one of the most “shocking” facts about money. (source)

31. The most expensive US coin is the 1913 Liberty Head Nickel, it sold for $3.7M in 2010

It was a five-cent piece produced in extremely limited quantities unauthorized by the US Mint. So it’s like the rebel of the coin world. There are only 5 in the world ever known to exists and two are in museums while the other three are in private collections. (source)

Even Snopes confirmed this is true. It’s not necessarily because everyone is out there snorting cocaine, but when bills with cocaine residue are counted in a counting machine, those machines move the trace amounts over other bills. So thus lots of money gets coated with cocaine. (source)

33. The average lifespan of a US Coin is 30 years

That is drastically longer than the typical lifecycle of a $1 bill, which is 18 months. Coins are simply more durable. This is one of the most “resilient” facts about money. (source)

34. All US coins have a stamp (Mint Mark) from where they were made

Each coin has a single letter to indicate where they were made. If a coin doesn’t have a mark, it was likely made in Philadelphia since they were the first US Mint and still largest Mint. Today most coins except Philadelphia’s have mint marks on the back. (source)

P – Philadelphia

D – Denver

S – San Francisco

W – West Point

35. The Lincoln Penny is the only coin where the figure faces right

On every other coin, the faces look left. It’s not the most significant finding, but it is kind of interesting for trivia! (source)

36. The US Mint produces more coins than any other Mint in the world

In fact, in addition to all the US coins produced by the US Mint. At times, they have produced coins for other countries as well, making it the largest coin maker in the world. (source)

37. Whenever the US Mint produces coins, they make a profit

There is a difference between what it takes to “make” and coin and how much it is “worth”. That profit is what funds the US Mint and creates additional revenue for the United States to spend on education, healthcare, and other US agencies. (source)

Think these were interesting? It took us lots of time, it would be super cool if you gave these a share to your friends who also like interesting facts about money!

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Most of us have to work a day job. We have bills to pay and mouths to feed. But that doesn’t mean we have to take whatever they offer us. Many companies offer incredible perks and benefits that help take the sting out of working. Other perks at work seem nice on the outside but aren’t as great as the company makes it seem.

If you have options as to where to work, there’s a lot to consider regarding the offered perks. Sometimes you can even negotiate to get some of these sweet deals when the company doesn’t traditionally provide them!

What Are Work Perks?

Perks at work are the benefits employees get from working at a particular company or organization. Employers use perks in addition to compensation packages to recruit and retain the best and brightest employees.

Companies offer prospective employees a range of benefits for signing those employment documents. These might include traditional work perks like a hefty salary and pension plan or modern benefits like a retirement savings account and paid vacation time. These perks at work are generally considered part of overall compensation and not always considered perks. However, I’d argue that if you’ve ever worked retail and are moving into a position that offers these benefits, they are definitely perks!

How are Perks at Work Different than Employee Benefits?

Work perks and employee benefits can be interchangeable. When they aren’t, benefits are often used to describe compensation packages, and perks describe bonuses. Compensation packages include salary, healthcare, retirement accounts, employer matches, stock options, etc. Perks might consist of other things, like a daycare on-site, or flexible schedules, or even the ability to sleep or work out while on the clock.

What Are the Best Perks at Work?

It’s hard to say which perks at work are the best. Everyone values different things. Some may be thrilled to work at a place with a foosball table, while others want a high salary so they can build their FU fund. There is nothing wrong with either approach, but that makes it difficult to call one thing out as “the best.”

With that said, there are a lot of great perks you can get at work. It’s essential to determine which types of perks you value the most so that you can ask your recruiter or hiring manager about them during the hiring process.

Here are some perks and benefits that companies might offer to attract top talent.

Flexible Schedules

One of my favorite perks is the ability to have a flexible schedule. However, each organization has its own definition of flexibility. Some companies let you choose between different set schedules, like the traditional eight hours per day, five days per week schedule, or a four day per week, 10-hour schedule. They call this flexibility because you aren’t stuck working whatever schedule they give you. Although it’s nice to be able to choose, it’s not ideal.

Other companies have much better options for flexibility. They let you come in whenever you want as long as you get the work done. Or they let you decide to work 8 hours one day, then 10 hours the next to take a few extra hours off on a Friday night. Some even allow you to work remotely whenever you need to. The ability to do your work at your own pace is a great perk.

Childcare

One of the best perks a company can offer parents is onsite child care. Unfortunately, this one is tough to find. However, a company that provides it shows that it values women’s work and values families.

Childcare is one of the most significant expenses a parent will encounter. Working for a company that understands that and helps reduce that expense in any way is a huge perk. A company that offers free childcare on-site gives working parents a lot more flexibility at work. Some companies may not offer childcare, but they might reimburse some childcare-related costs. Anything a company does to help families is a valuable perk.

Tuition Reimbursement

With the exorbitant cost of college education, finding a company that will offer tuition reimbursement or helps you pay off student loans is a fantastic perk.

The Federal Government offers a student loan forgiveness program that pays off all of your federal student loans after ten years of government service. It can be challenging to qualify for this program, so please be sure that you read all of the fine print before deciding upon government service as a means to pay off your loan. Also, the loans have to be federal. Private student loans do not qualify for reimbursement under this program.

Many other companies also help their employees further their education. Some companies offer completely paid tuition at partner schools. Starbucks will pay for any of its employees to attend Arizona State University’s online program, for example. However, they don’t offer any covered tuition for any other schools or programs.

Other companies will give each employee a set amount of money for tuition reimbursement each year as part of a compensation package. UPS offers $5250 per employee per year, and Wells Fargo offers $5000. You will have to work with your hiring manager and HR representative at each company to determine how to apply for that company’s specific program. Still, it’s incredible to know that there are so many companies out there offering help for tuition.

Paid Time Off

Paid time off is my favorite perk at work because, let’s be real; if they weren’t paying me to be there, I wouldn’t be. It’s even better when work pays me NOT to be there, am I right? No law in the United States guarantees any paid time off, so companies that offer comprehensive leave packages are the best places to work. Some offer both paid time off for vacations and paid time off for sick leave, while others lump all the time off together into one pool and call it “flexible time off.” I prefer them to be separate. It would be awful to plan a two-week vacation but then get sick a few weeks before and not have enough paid time off left for your vacation.

However, any paid time off is better than no time off. It’s a great perk when offered.

Healthcare

The healthcare system in the United States is a mess. It’s tied to employment, and that doesn’t seem like it’s going to go away anytime soon. The most significant benefit a workplace can offer is a comprehensive healthcare package that gives employees lots of options.

It’s wonderful to choose between HMO and PPO and pick the healthcare plan that works the best for you and your family. However, most people are limited by what their employers offer. By law, all large companies must offer some type of plan to their full-time employees, but that doesn’t mean the plan will be good. It’s important to discuss the healthcare plans and benefits with your hiring manager before accepting the role to ensure that it will meet your needs.

Discounts

One fun perk that some companies offer is discounts. Most companies will provide at least an employee discount at their organization, but some offer discounts for partner companies. The military is well known for getting deals in tons of places, from restaurants to retail to theme parks, but other companies can offer their employees similar perks.

Some companies sign up for overall discount programs for their employees. Great Work Perks is a website that any company can join to offer its employees discounts at various locations. There are quite a few different companies that offer bulk discount packages to corporations. That helps a company offer unique and exclusive benefits to its employees.

Wellness Programs

Many companies have realized that employee wellness is a huge factor in productivity and have instituted wellness programs to help their employees. These programs might include simple programs like gym reimbursements (or even on-site gyms) or more complex features like therapy sessions.

Many companies contract with employee assistance and wellness programs to provide confidential counseling in all areas of someone’s personal life. These might include financial, mental health, or relationship counseling, nutritional guidance, or even parenting help. A contractor administers these programs to ensure the confidentiality of any employees who use them.

I’ve used employee assistance programs to get free relationship counseling in the past, and it has been a godsend. Being able to seek out free, confidential help sponsored by an employer is a fantastic benefit.

Sabbaticals

One incredible perk that very few companies offer is the chance to take a sabbatical. Sabbitalcs are a once in a career break where you can research, explore, and do whatever you want for an extended time. Generally, it’s only available to tenured professors at prestigious institutions, but other companies may allow employees to take an extended leave of absence.

The difference between a sabbatical and an extended leave of absence is that most companies pay you while out on sabbatical, whereas with a leave of absence, your job is guaranteed when you return, but you won’t get paid while you are out.

It’s hard to find a company that offers a sabbatical, but if you do, be sure to take advantage of it!

What Are Some Perks at Work that Aren’t So Great?

When looking at perks with any new job offer, be sure to consider whether they really are perks or if they are insidious cultural expectations fancied up to look enticing. The office might have a free cafeteria, but do they expect you to work through your lunch or be available during dinner hours? There might be awesome-looking nap rooms available, but is the expectation that you will stay into the wee hours of the night to complete projects?

Some companies offer seemingly unique perks, like unlimited time off. However, be sure that the culture allows you to use perks like this. Sometimes, work perks are advertised, but the culture of the organization prevents you from using them. Unlimited time off seems like a great benefit, but you get chastised if you ask for even an afternoon off or told that “this isn’t a good time,” is it really a benefit? It’s important to know if you can use the perks at work before committing to employment.

Perks at Work Mobile App

As mentioned previously, many companies contract out their perks to a third party. Perks at Work is one such third party. It’s an employee perk program that you can access via a mobile app.

I like the perks at work app better than the other companies mentioned because it has more variety. It’s a discount app rolled into a wellness app that also offers personal development features. Employees can access a variety of online classes on countless topics. There are even programs available for kids.

Interestingly, there is space for a program like perks at work in today’s society. Businesses are learning that their employees need more – not only monetarily but also for their personal and professional development. This app fills that void, and companies that use this or similar programs prioritize the welfare of their employees.

How to Get Perks at Work?

Mobile app aside, it’s not always as easy as it seems to get access to some of the great perks and benefits discussed here. The companies that offer the most perks are trying to recruit and retain the top talent, which means that in-demand fields are more likely to be offered perks during the recruitment and hiring process.

The fact that a perk isn’t publicized doesn’t mean it’s not available. It never hurts to ask a potential employee if they offer a particular perk. Sometimes, this discussion of perks and benefits is part of the negotiating process. The company may not provide you a higher salary, but they can give you more time off or access to wellness programs that would cost more on their own.

If you are already making enough money, you may even prefer these benefits over a higher salary. It’s important to have these conversations before being hired or during your performance review with your boss if you’re already at a job you love. You never know what a company might be considering implementing, and having an employee ask might be the push they need to do it.

Getting the Perks You Deserve

Not all companies offer unique perks and benefits. Sometimes we need a job and need to take what we can get. But sometimes, we have choices and options. When you do, believe in yourself and your abilities. Know that the company needs you and is willing to pay to get you. Use that to negotiate for the perks that are most important to you.

This article originally appeared on Your Money Geek and has been republished with permission.

Millions of Americans have unfair credit scores. They affect many spheres of life: borrowing, renting, insurance, and even employment! Mistakes always stem from flawed reports. Information collected by any of the agencies — TransUnion, Experian, or Equifax — may be the culprit. If your low score is a result of inaccurate calculations, follow our guide to raise it for free.

Premise of Repair

As all scoring systems are automatic, your total will rise as soon as the mistakes vanish. You must understand that only erroneous reports may be changed. If a derogatory is a fact, it will remain on your records for years — usually, seven. Bankruptcies may tarnish the status for a decade depending on the chapter filed.

Correction requires several steps. First, you need to obtain the data from all three agencies and pore over it. After finding the mistakes, you should collect sufficient evidence to prove them. Finally, you will communicate with the bureaus in writing to have the errors deleted.

The complexity of the process prompts many Americans to opt for professional credit repair. Check reviews of the best credit repair services in your state to see how this works. Professionals can save you a lot of time and prevent re-disputes.

Do not expect an overnight boost, though. Every dispute claim is investigated within 30 days. Afterward, the bureau accepts or rejects it. You may also be asked for additional proof, which delays removal. Find out more about the average total duration in different cases. Here are the key stages regardless of complexity.

1. Obtain Your Reports

Collecting the records is a breeze, and you can always check your credit score through mobile apps like Credit Karma. To download the documents from all three bureaus, visit www.annualcreditreport.com and submit a request. Only basic information is required, and the result is immediate.

Alternatively, you could contact the organization by phone or send a written request. In this case, the data will be provided within 15 days. With the full reports on hand, you can proceed to the next stage — meticulous analysis.

Note that looking through all the records is essential. Each lender may share information with a specific agency. Any of the histories may be wrong. It means you may need to open disputes with one, two, or all three bureaus.

2. Scrutinize Your Histories

Look through all versions of your borrowing history carefully. Go line by line, checking all the figures and details. Mistakes range from wrong spelling to false events. You may even see a bankruptcy that never happened! Print out the reports and mark any inconsistencies.

3. Gather Evidence

For a mistake to be removed, it must be proved — contact your lender to collect sufficient information. Bank statements and other documents should make your claim persuasive. Upon receiving your request, the bureau will still communicate with the lender, but you have to include the evidence in your claim.

This stage is crucial. If the bureau finds your proof incomplete, it may request more information. Considering the length of every investigation (30 days), this will delay repair considerably. Consumers who use credit repair services have all the evidence collected for them. Professionals also send debt validation letters on their behalf. These oblige the lenders to prove their clients owe the amounts reported.

4. Open Disputes

The Consumer Financial Protection Bureau offers free guidance, and you can find free templates of dispute letters on its site. Formal correspondence must be sent by certified mail with a return receipt. This will provide hard evidence of communication.

Knowing when your letter was received, you can understand when to expect a reply. In some cases, the investigation is extended from 30 to 45 days. Eventually, if the corrections are accepted, the bureau will mail you a copy of the revised report. This does not count as your free annual copy.

Experts recommend covering 3-4 errors in every letter. As you can see, repair may take months. The more often you check your credit reports — the easier it is to fix them. Hiring a repair firm will also speed up the process. Industry experts know which derogatories to target first and what evidence to collect. They will do everything on their behalf while you simply monitor the progress using a portal or an app.

When the Score Is Correct

So, what can be done if the score is perfectly fair? When it falls due to your own irresponsible behavior, the only remedy is changing your habits. The bureau will never remove any missed or late payments that are legit. However, there are several methods to try. For the best results, use them all simultaneously.

1. Credit Utilization Ratio

Credit utilization reflects the use of available limits. It only applies to forms of revolving credit — i.e., credit cards. The lower the indicator — the better. Experts recommend keeping it under 11%.

To establish your utilization, divide all the current balances by the limits. For instance, if you have four credit cards with a total limit of $10,000, and you have used $4,000, the ratio equals 40%, which is too high. To bring it down, you could pay off the balances (at least, partly). Achieving the target utilization of 10% would require a total balance of $400.

Alternatively, request a limit increase. This will achieve a similar result. However, in our example, the size of your available credit would have to expand to $40,000, which is hardly realistic. So, extend the limits and pay off the balances at the same time.

Finally, getting a new credit card is also helpful. If you do not qualify for a standard product, get a secured one instead. As it requires a deposit, lenders will be more willing to issue it.

2. Adding More Data

One of the bureaus allows consumers to include more information in their reports. Through Experian Boost, you could add utility bills and other payments — even your Netflix subscription — to gain a few points. According to the bureau, 10 is the average result.

Final Words

To raise the credit score, you need to understand if it is fair. According to statistics, 20% of Americans have one or more mistakes on their records. Open disputes to remove verifiable mistakes, and rebuild your history if it is accurate.

Combine different methods for quicker results. If you want to avoid the hassle of complex repair, hire a team of professionals and delegate the job. It is the most convenient and efficient approach. Choose your provider based on BBB ratings, customer reviews, and expert opinions. All of this information is easily accessible online.

The 80-20 rule can be related to an old story. Legend has it that Italian engineer Vilfredo Pareto noticed something peculiar about the peas growing in his garden. Vilfredo recognized that approximately 20% of his pea plants were yielding 80% of the pea crop.

The engineer inside got the best of him, and he expanded this concept to macroeconomics, where he observed 80% of Italian wealth was and still is controlled by 20% of the population. In case you are wondering, Pareto did not create your favorite pasta sauce; instead, he is known for the infamous Pareto Rule, or what you might call – The 80-20 Rule.

You can 80-20 your life to create more money, time, and happiness. Today, we will show you exactly how to apply the 80/20 rule to your life, starting with the benefits and how the law works!

What is the 80-20 Rule

Simply put, the 80-20 rule states that 80% of your outcomes (outputs) come from 20% of causes (inputs). Using the pea example, 80% of the peas eaten from the garden came from 20% of the plants.

In business, the law states that you should focus your efforts on identifying the most productive 20% (clients, channels, sources of income) and spend 80% of your time there. You can use the popular 80/20 rule can be used to fit any facet of life, however, and many use it to help them strategize how they spend their time with regards to;

Health

Wealth

Business & Investing

Relationships

Habits

Mainstream examples of the 80/20 Rule

80% of your business will come from 20% of your marketing

80% of covid is spread by about 20% of people