Here on Wallet Squirrel, every day we are finding new ways to earn money and investing those profits to build an online stock portfolio. Our stock portfolio is exclusively made of dividend stocks, so in the future, we can live off the income produced by those dividends. As investors, we have some preferences on why monthly dividend stocks are better than quarterly.

All Hail Dividends

If you’re curious about what dividends are, our best summation is that they are a portion of a company’s profits that are distributed to shareholders regularly.

If you want to know more, check out our What Are Dividends article. There are a lot of companies that produce dividends (why I love them), but receiving dividends monthly is pretty awesome!

Why Monthly Dividends Stocks are Awesome!

Monthly Dividend Stocks are way easier to budget for – If you’re waiting quarterly for those dividend checks, you’re forced to budget that income for the next several months. A lump sum you have to let sit in your bank account tempting you to spend it. No matter your willpower, you’ll always be thinking “I’d be willing to eat Ramen Noodles for the next month if I bought a boat right now”. You’ll be the most sodium-rich sea captain. You’re better than that.

Better Compound Interest – If you’re receiving dividends every month, you can use that to reinvest in more stocks and have those dividends grow more by the time your other quarterly stocks arrive. Simply, the faster you reinvest those dividends, the faster they’ll compound interest. For Example, if you owned 1,000 shares of a $10 stock at a 5% annual dividend. At the end of the year, you’ll have earned 5% at $500. However, if you received monthly dividends, you could reinvest those dividends each month and have earned 5.12% at $511.62. This is assuming you have a DRIP campaign set up. However it’s obviously more, and that’s only one year.

It’s enjoyable seeing regular income – There is something incredibly satisfying as an investor seeing their investments create monthly income. It feels like you’re earning extra as your stock price fluctuates, you’re still seeing income being produced. You can reinvest or spend that monthly income but it gives you extra cash each month to play with.

What Type of Companies Produce Monthly Dividends?

You’ll mostly find monthly dividend companies limited to Real Estate Investment Trust, Business Development Companies and sometimes Master Limited Partnerships.

Real Estate Investment Trust – is essentially a company that owns multiple properties and generates income based on those properties. They can specialize in different real estate niches such as commercial property, apartments, office buildings, hospitals, etc. Each REIT usually has a specific focus and most produce dividends.

Business Development Companies – are organizations that invest in small to medium-sized companies to help them grow in pivotal stages of their development. Their income is made up of their investments in companies.

Master Limited Partnerships – are organizations that generate predictable income streams based on production/processing/storage and transportation of depletable natural resources.

Are you invested in any monthly dividend stocks? Tell me about them.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

My goal on Wallet Squirrel is to find new ways to earn extra money and then invest what I make into my stock portfolio of dividend stocks. These dividend stocks are key, because my goal is to invest in enough dividend producing stocks that they may replace my current income. To do this, I need to invest more and my latest stock is Iron Mountain Incorporated, stock ticker (IRM).

Let me introduce Iron Mountain (IRM)

If you’re not familiar with this company, let’s hit a brief overview. Iron Mountain is a storage company, storing physical records as well as data centers for companies.

Physical Storage Items

The types of physical storage vary greatly from anything you could imagine a company wanting to store. These could be HR files, to legal, to extra storage. In fact, 95% of the Fortune 1000 uses Iron Mountain. They also mention a range of geological samples to fine art as storage capabilities they offer. These are storied in over 1,400 facilities, covering 87.5 million square feet of storage around the world, including a legit underground vault.

Digital Storage Items

Iron Mountain also has extensive digital storage systems that allow companies to electronically back up their systems. These are both in the form of storing disk drives of important systems, as well as their “Iron Cloud” as their enterprise cloud-storage platform. As cybercrime continues to become a bigger and bigger problem, companies are paying big money to have several working copies of their systems backed up. They expect their cloud storage to produce 7% of their total revenue in 2020. The total revenue for 2017 was 3.8 billion.

Why I Personally Like Iron Mountain

Reoccurring Revenue

I’m a huge fan of companies with reoccurring revenue because it’s dependable. Iron Mountain as a storage company holds company records for quite a long time. In fact, they’re still holding onto 50% of the boxes that were stored in their facilities over 15 years. As more legislature mandates companies to store physical copies for longer and longer. Iron Mountain is an ideal, service for these needs. Plus as their cloud business continues to grow, people continue to pay large contracts for years at a time to continue and hold their back up needs.

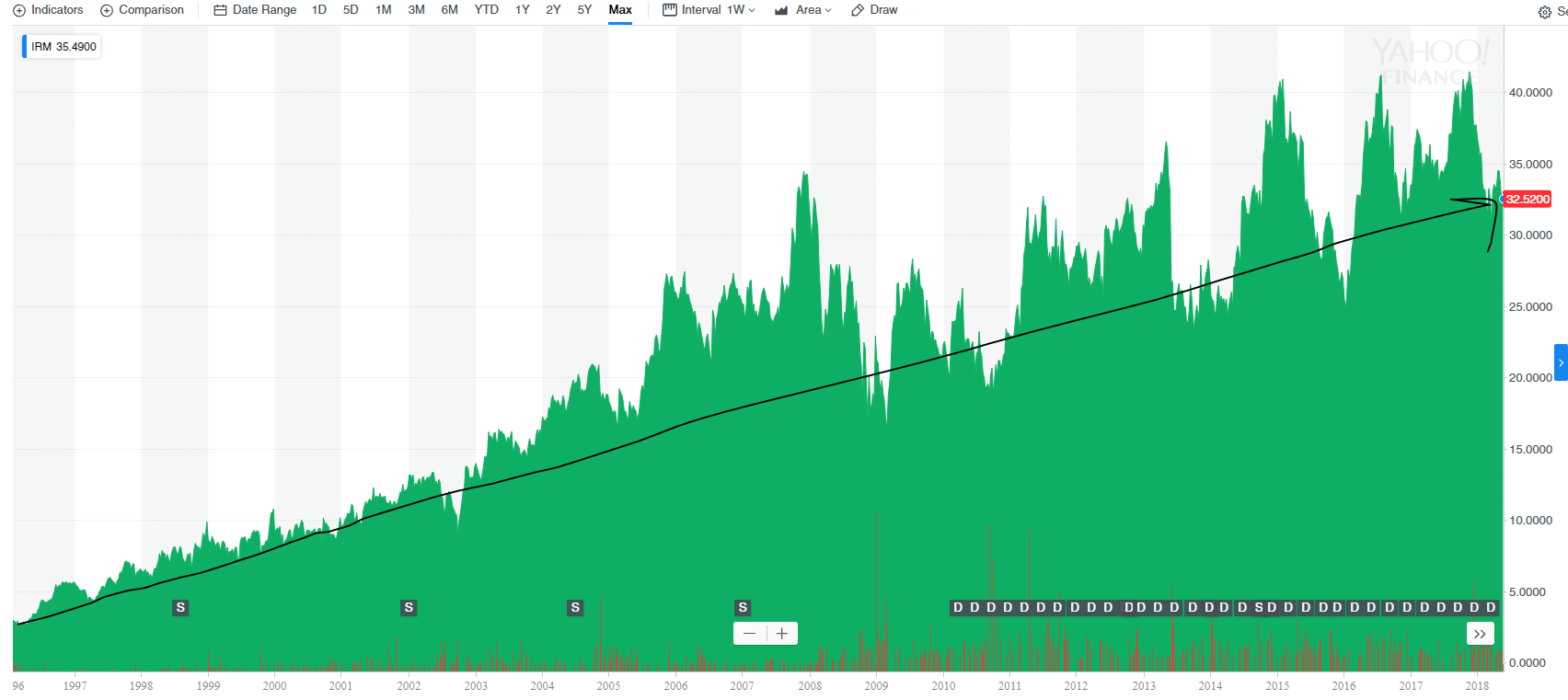

Technical Analysis

Technical Analysis is looking at their past performance to indicate how they will do in the future. Of course, past performance doesn’t guarantee future results, but I like to see that a company is consistently doing well. I usually do this by looking at their stock price over the max course of their life. Here is the trending graph for Iron Mountain (IRM). I typically like to see this chart shoot up and to the right. Despite some bumps, it continues to move in that direction.

Low Beta

I like safe stocks, so I always look at a stock’s beta. The beta will tell me how likely the stock price will swing with a market correction, or the overall stock market drops/raises. If the Beta is 1, the stock will rise and lower pretty equally with the overall market. If the Beta is over 1, it’ll swing more rapidly in either direction. The lower the Beta under 1, the less likely the stock will be as affected by the overall market. The beta for Iron Mountain is 0.54, meaning it’s relatively safe during large market swings. This is because most of Iron Mountain contracts are locked in for long periods of time, and short-term swings won’t affect them as much. I love that!

Dividend Rate – 7.01%

Yes, that’s right. It’s a high dividend, even for a REIT. I would be concerned if they didn’t have so many facilities around the world locked in long term contracts. A quarterly dividend of 7.01% is pretty great!

Diversified Revenue

For all of their storage capabilities for both physical and digital storage, no one customer makes up more than 1% of their revenue. That means even if one customer for some reason pulls out, it isn’t a big hit on their overall revenue.

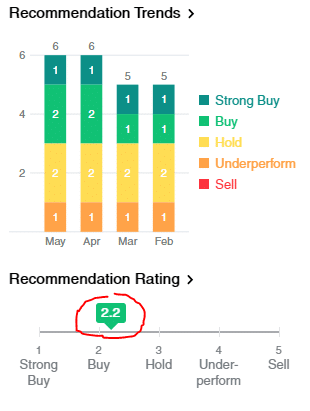

Experts Also Consider IRM a Buy

Before I make a purchase, even after all of my data and research, I always do a double check to see what the “professionals” are doing with this stock. If they suggest “buy” then I know they are aligned with my research. If they say “sell” then I dig a little deeper to see what they are looking at, that I may have missed. Just because they say “sell” doesn’t mean I won’t buy, I just want to make sure I know everything before investing. In the case of Iron Mountain, the “experts” say “buy” via Yahoo Finance.

Iron Mountain isn’t all Sunshine & Rainbows

The biggest thing against Iron Mountain is their debt. Similar to most REITs, they have a considerable amount of debt that has helped them grow. They pay for this debt with a portion of the revenue made through their storage leasing in these facilities both physical and digital storage. At the end of 2017, their debt was $7.1 billion, which is a lot. However it’s still under the $10.9 billion in total assets. Plus most REITs have a sizeable chunk of debt. So this is something I’ll continue to monitor.

Conclusion

In the end, I ended up purchasing 2 shares of IRM at $32.73 per share. Why so little? Mainly because I’m broke, but try to buy stock whenever I can. I’ll continue to buy more of IRM as cash becomes available because so far, I’m a fan of the stock.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Disney’s New Streaming Service Will Soon Destroy the Competition

We talk about the rise of Netflix, Amazon’s streaming service, Hulu and even YouTube but I don’t think we’ve discussed enough of the impact Disney’s new streaming service is going to have.

Yes, Disney is Developing its Own Streaming Service

If you didn’t know, Disney is developing its own streaming service that’s looking to be priced substantially below Netflix at its launch. They have been leaking bits and pieces about their new streaming service here and there so we only know a little, but I don’t think people realize how big of news this is.

Cable TV is Dying, Streaming is the New Thing

In 2015, Netflix and Hulu grew 29% to a $5.1 billion market cap while cable and satellite tv only grew by 3%. It’s safe to say that streaming is taking over. Netflix alone has 109.3 million subscribers and anticipates another 6.3 million subscriptions this quarter. Those 109.3 million people are paying $10.99/month. That’s $1,202,300,000 per month. Not bad.

With Streaming, Content is King

Netflix realized a while ago, that anyone can get copy rights to movies and tv shows to be a streaming service, but what makes you unique is the original content you produce. That’s content you exclusively control. Think “House of Cards” you can’t get that anywhere except Netflix. Those original shows draw crowds of people to Netflix and they stay for the wide range of shows to watch. So much so that most people don’t need cable anymore other than sports, which have started streaming as well.

Nearly every childhood movie (Lion King, Aladdin, 101 Dalmatians, etc.) is owned by Disney. Now add onto those the Pixar movies (Toy Story, Finding Nemo, Cars), Marvel Studios (Iron Man, Captain America, Thor, Avengers, etc.) as well as Lucas Films (Star Wars). These are just a taste of the original content has, and can start streaming on their own network when ready. They own the exclusive rights to these films that can be leveraged in their new streaming service.

Then you also need to consider all the Disney channel content and shows that it’s created for tv, soon going to be available in one location. I wouldn’t be surprised to see the Disney Streaming service being the one streaming service owned by every mom in America.

Now start to consider what if Disney started to produce new content, including Star Wars, Marvel and/or movies exclusively for their new streaming service. That will be a huge draw to the service!

As much as Netflix, Hulu, Amazon Video and YouTube can crank out content. Disney has a winning formula it’s used for years to amass loads of quality content and proven itself over and over. It WILL win the original content game. If Disney can continue to dominate the original content game, they will win the streaming game.

When Does Disney’s Streaming Service Start?

The only thing we know is that Disney plans to debut their streaming service in 2019. Coincidently, this is when their current contract with Netflix is through. So when Netflix loses all their Disney content (think Marvel Series like Jessica Jones, Luke Cage, Daredevil, etc plus other Disney content), Disney will likely publish these shows on their own streaming service.

Keep in mind, they’ll start their ESPN streaming service in 2018 to start catching those cable-cutters who love sports. This will give them an opportunity to help hash out all the bugs for their larger digital content streaming service.

Will This Impact the Streaming Industry?

To give you an idea of the impact the news about a Disney streaming service. When Disney made the announcement, Netflix stock price dropped 4%.

Plus Disney has the resources not only from its box office hits, but it’s depths of resources to undercut all these other streaming services in price. So while Netfilx will continue to raise it’s monthly subscription price to pay for their original content, Disney win the war on prices and simply choke Netflix out. We’ll likely see Amazon Video and Disney as the lasting champions in the streaming game.

Conclusion

I am going to try to pick up a few more shares of Disney while the price is low before 2019. It’s not the greatest dividend for my dividend strategy at a 1.51% dividend, but it’s a great company with a great plan to be the #1 player in streaming services.

If you liked this article, I’d love if you shared it! =)

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

After seeing multiple investor friends pick up Cisco (CSCO) lately, I had to check it out. So these are the insights I looked into and ultimately factored into my first purchase of Cisco.

Why am I sharing my latest stock purchase?

Each month I try different ways to make extra money and share how much I make in my Income Reports. Every month I use this money to buy more stocks and other investments to build a $10,000,000 investment portfolio. It may take a while, but it’s done with one investment at a time.

This month I bought 9 shares of Cisco.

What is Cisco

Cisco (Stock Ticker CSCO) is a hardware and software company that designs, manufactures, and sells Internet Protocol (IP) based networking and other products related to the communications and information technology industry worldwide.

I basically just like to think of Cisco as the infrastructure of the internet. All of the highways that connect websites and databases and funny cat videos of the internet are primary run on Cisco products.

If you want to know what a company does look at their revenue. In 2016 this is where their money came from:

Switching (30% of revenue) – Switches connect computers, printers, and servers within a building or campus. These allow everything to talk to each other. Switches create a network of devices.

Routers (15% of revenue) – If a switch is a network, routers connect networks. A router links computers to the internet.

Collaboration (9% of revenue) – This is a general term to describe their immersive video conference software, IP telephones, software to connect the devices to talk to each other. This includes Jabber, Cisco WebEx and Spark. For example, my office uses Cisco WebEx to coordinate all of our in/out video conferences.

Data Centers (7% of revenue) – Data Centers allow large scale flexible computing. This can be from storage to computing power.

Wireless Infrastructure (5% of revenue) – These are the base stations and infrastructure for Wi-Fi. Think of hotels, casinos, grocery stores, airports and any building that provides Wi-Fi. Most of these devices are Cisco related.

Security (4% of revenue) – These are the firewalls that block out Russian hackers and malware from accessing their infrastructure and their client’s servers/computers/Internet of Things.

Services (24% of revenue) – These are the people that run these services, train clients how to use them, manage networks, operate systems and support their wide variety of products.

We can say that the other 6% is “Other”, but you get the idea they do a lot with the internet. Combined all these products and services generated $49,247,000,000 in total revenue in 2016.

Why did I buy Cisco?

When looking over Cisco, they really hit some of the key factors that I look for when buying a stock.

1. Dividend (good)- They have a 3.69% dividend that they’ve had since 2012. That 3.69% is really nice considering this is a tech stock that traditionally has lower dividends.

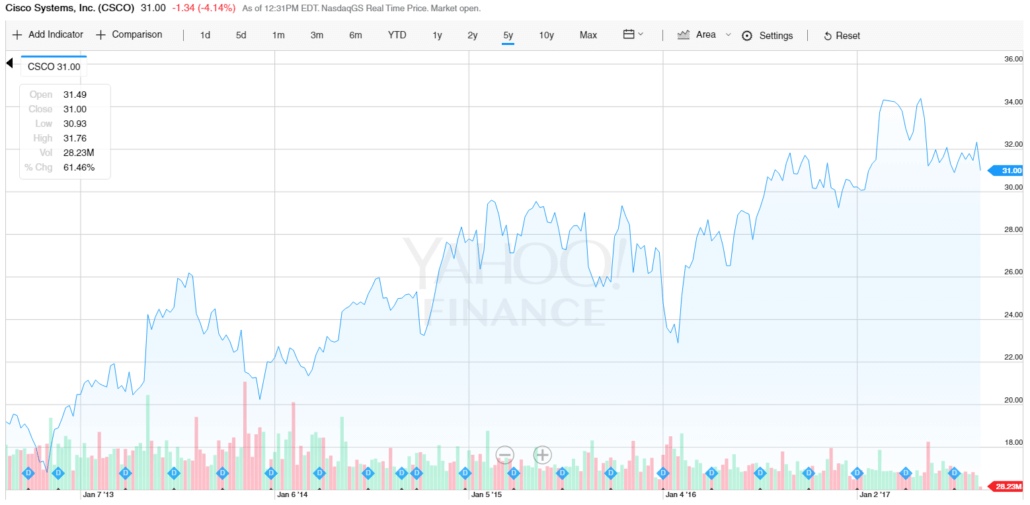

2. Historical Performance (good)- They say that past performance doesn’t indicate future performance, but I like the graph of the stock price over the last 5 years. It has its dips, but overall it has a progressive climb. That is a plus for me.

5 Year Graph of Cisco’s Stock Price

3. Strong History (good) – I’m not a big fan of crazy risk, so I like to invest in proven companies. Cisco has a market cap of 161.702 Billion, they’ve been around since 1984 building the internet. I want to make sure that the company has been tested long enough and a strong times interest earned ratio that they know how to manage market downturns.

4. Reoccurring Revenue (getting there) – Cisco has traditionally been a hardware company, but they are transitioning into more of a software company and one that wants to focus on a subscription model. Their CEO, Chuck Robbins even mentioned in their 2016 Annual Report that they are “working to move more of our revenue to a software-based and subscription-based model”. I am a huge fan of reoccuring revenue, so when I see a company of this size transitioning to that business model, I can get on board.

Since I liked what I saw, I bought 9 shares at $31.89 per share for a total of $279.09.

Why did I buy now?

In honesty, I probably rushed into buying Cisco because I wanted to buy their stock before their earnings call on August 16th (yesterday). I thought the stock would increase after the earning call, but it dropped a bit after coming short on revenue. F*&K.

The stock price has dipped about a dollar since then. I failed.

I will continue to hold Cisco because I think they are in the right direction, but it just sucks that I bought it right before the dip. This will probably teach me not to rush into anything when looking at future stocks.

Conclusion

I like Cisco and look forward to following them, but will be hesitant into rushing into any future buying just because a earnings report is coming up and everyone else is bullish on a stock.

If Cisco continues to invest more into their subscription-based business model, I’ll likely add more to this position.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

If you haven’t seen my income reports, I’ve been making some nice extra income and I always invest this for passive income in the form of dividends. Here are some of my latest stock buys with the extra cash.

How Do I Invest?

I’m still pretty new at investing so I usually try to invest $60 bi-weekly through dollar-cost-averaging. The idea that if I maintain a consistent schedule investing, I’ll be both investing in the worst of times and best of times of the stock market. This is much better than trying to time the market (that doesn’t work).

I invest using the Robinhood App so I don’t have to pay any fees, especially since I invest so little at a time.

How much have my investments made so far?

Before I go in my recent stock buys, I should share how much I’ve made so far to justify why I continue to invest. I started investing in September, 2015. That was my first stock market purchase ever! I invested $581.98 into a couple different stocks. Since then, I’ve continued to invest a little at a time as I earn extra money.

Since September, 2015 I have invested a total $7,437.81. That’s a hell of a lot to me! However the stock market continues to be my best income generator. My portfolio value is currently worth $8,615.56. So I have gained 16.65% in value. Not bad for someone who just started less than 1.5 years ago!

Of course, there are highs and lows, but as long as you continue to invest in the highs and lows, traditionally the stock market continues to make 7% per year. Plus I always make dividends each month.

Latest Stock Buys since May

Apple (AAPL)

I picked up Apple (AAPL) back in May when the price was $91.18. This was the time people were freaking out that Apple hasn’t released any new products and feared that current customers would lose interest in their current iPhones. iPhones are one of their largest sources of revenue for Apple, so because phone revenue was leveling off, people saw this as the end of Apple.

That was a ridiculous notion, so I bought 1 share. Yea, that’s right, I only bought one because I didn’t have the money at the time to buy any more. It was at $91.18 and I bought it with a grin.

Why was I confident about Apple when so many people were fearful? They had over 1 Billion (Billion with a B) in cash reserves to use however they want. They could buy a company or invest in a new market, that much capital gave them so many possibilities, like invest in car ride sharing, driverless cars or new technology, and they did all of those! Plus have you ever met someone who owns an iPhone? They treat it like fat kids treat cake.

I told myself I would sell at $116, and when it moved up to that level in December 6 months later, I sold at $116.32. That’s a nice 27% profit, I’ll take that. Plus the $0.57 cents I earned in dividends. Currently Apple is around $141.42 but I can’t worry about that, you have to set goals, follow them and don’t look back.

Verizon Communication (VZ)

Verizon is one of my favorites because I’ve been to a Verizon store and any store that regularly has customers standing in line for 45 min, is worth noticing. People hate switching carriers, so they’ll deal with a number of issues before they go to AT&T, Sprint or Tmobile.

Since May, I bought 5 more shares of Verizon because it’s dipped below $50. So mainly this was bringing my average share cost down. The more shares I buy during this dip, the higher my profits will be when it goes back up. Remember when everyone else is cautious, that’s the time to buy. As long as the company is well established, in my opinion.

I’ll keep buying Verizon shares whenever I can, but they currently make up 15.9% of my portfolio, so I’ll look at some other companies before I buy anymore to diversify. I just really love their 4.60% dividend! Just last February, I earned $13.28 in dividends for holding this stock.

Procter & Gamble (PG)

This company makes recognizable consumer stables like Bounty Paper Towels, Charmin toilet paper, Crest Toothpaste, Dawn dish soap, Downy fabric sheets, Febreze and so many more! These are household items that people buy over and over again because people NEED them and they’re brands people trust.

Personally I’ve used all these products and I’ve never had a reason to use anything else. This is one of my biggest reasons for continuing to own this stock.

I’ve bought 4 shares since May, all when the price was around $82. Now the stock is up to $90 per share. Plus, Procter & Gamble has paid me over $20.10 in dividends for just holding the stock since May. Anytime this stock dips in price, I’ll be there to buy more.

Wells Fargo (WFC)

Oh Wells Fargo, you continue to disappoint people with scandals and I’m there to pick up your stock. I was sad to hear about the scandal because it took a massive dive to my stock price but I kept two things in mind. Fed Rates were going to rise and people hate switching banks, so I bought up shares like they were a new iPhone on Black Friday.

In total, I bought 9 shares. These shares ranged from $50.17 to $45.41. Currently the price has shot up to $55.33 and continue to produce dividends. Since May I have received $26.22 in dividends.

I’m really happy about this one because I knew fed rates would rise, increasing this stock’s value while everyone else concentrated on their scandals. People have short term memories and in this case, it paid off.

Iron Mountain Incorporated (IRM)

This REIT isn’t a well-known company, Iron Mountain is a REIT who provides physical and digital storage across North America, Europe, Latin America and Asia Pacific.

I like this company for two reasons. One, they provide physical document storage for companies across 1,400 facilities in the world. I’ve seen Storage Wars, I know people will pay to store things forever to calm any fear of losing something permanently. Second, I like this company for their growing digital storage capabilities. Cloud computing and cloud storage is HUGE, it’s quickly becoming Amazon’s largest revenue source. Iron Mountain leases a lot of these facilities. I like investing in companies like this that house the data centers.

Since May, I’ve picked up 9 shares at an average of $36.80 and the stock is currently at $35. I’m currently under on this stock but I believe it’ll raise back up. Plus in the meantime it produces a 6.31% dividend. So since May I’ve gained $19.90 in dividends.

HCP Inc. (HCP)

I’m always on the fence about HCP. What I like about it, is it’s a REIT that focuses on healthcare facilities like senior housing, medical office buildings and skilled nursing. I like this because baby boomers are starting to move into senior housing and medical office buildings are for outpatient services, which have grown tremendously in recent years.

My concern though, is HCP the best Healthcare REIT I can own? HCP has been doing a lot of house cleaning lately. HCR ManorCare, which did their post-acute/skilled nursing facilities has been facing challenges, so they spun them off into a new REIT called QCP (Quality Care Properties). It was a smart move because they were a high risk healthcare component to their portfolio.

In addition, they sold off over 64 properties that were leased to Brookdale Senior Living facilities because Brookdale made up over 35% of their healthcare portfolio, it’s now reduced to 27%. Plus Brookdale has had some major legal issues in the past that I’d prefer to distance myself from.

Because the last year was a little shaky for them and their stock has been cheap at around $29.85, I bought 11 shares. Now the stock stands at $30.49 with a 4.91% dividend that’s provided $27.91 since May. I’m still figuring out what I’m going to do with these guys.

Since May, These Stock Dividends have earned $107.98 in Passive Income

The Wallet Squirrel way is to side hustle & invest that extra income to make passive income with dividend stocks!

I put every dollar I earn side hustling into my stock portfolio of dividend stocks to earn passive income in the form of dividends. I think this is one of the purest forms of passive income and it proves itself. These stocks alone earned me $244.32 in dividends since May. That is money I didn’t do anything to earn, no effort whatsoever.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Yes I’m new to the stock market, but come on, even I know this is a bit crazy. Ups, downs and all around insanity. Get your act together!

It’s awesome being a dividend investor right now because my current plan of action is to ignore the craziness. Can I get a “Amen”?

My portfolio worth went from 12% to 7%. That’s impressive. When I looked at my account recently, my absolute first reaction was “Cool, I’m still 7% higher than if I did nothing with my money”. I’m forever the optimist. Plus I’ve gained $78.49 in dividends alone since I started in October, 2015 so WOOT WOOT.

Way better than a savings account. All around my portfolio is up $484.70.

Latest Stock Buys

In this recent downturn, I picked up 1 share of Apple (APPL) at $91.18. I had an extra hundred in my Robinhood Account and while I thought I would NEVER buy Apple, I couldn’t pass it up. I have always avoided it since I’m more of a Google guy and frankly people who love Apple products are THE WORST. Look at these people. Come on, you’re tattooing a company brand to your body and it’s an apple.

Here are some my reasons: Apple has SO much extra cash on hand (55.84 Billion) according to Yahoo. Plus with such a loyal following, they can do so much. I’m still waiting for them to buy Adobe. It’s been rumored, but nothing has happened. They did however recently invest $1 Billion in Chinese Uber Rival, Didi Chuxing. Uber is huge and if these guys have the Chinese market, there are opportunities to grow.

Yes, the iPhone market is getting saturated, and Samsung is getting some of that smart phone market share, but so what. Reference the above Apple Tattoo. People are die hard about Apple products and they frankly work well. That loyal following was the sustainability I needed to buy my first Apple share and now the prices is up to $95.22. I’m just sad I couldn’t buy more at the time. It was so near it 52-week range low and it’s P/E at 10.60. I usually try to take P/E (Price Earnings Ratio) into account

FUN Coincidence: Right after I bought my 1 share. Warren Buffet announced he invested $1 Billion in Apple. So maybe I’m doing something right. Am I the next Warren Buffet? It’s very likely, based on this one isolated coincidence.

Watch List

I now have an extra $130 in my Robinhood Account now waiting to be invested. I was hoping to write this article and do some research on what I should do with it.

Here is my list of the next 3 stocks that I’m watching and may pounce on in the next month.

Verizon (VZ)

Main Street Capital Corporation (MAIN) – Maybe

Kinder Morgan (KMI)

I’ve often listed many reasons why I love Verizon (VZ). The simplest is that people HAVE to have a cell phone and Verizon is growing a solid hold over this industry. How much is your monthly cell phone bill? You can answer this because you have a cell phone and you will climb stairs and mountains to get a better signal. Anything you pay a monthly bill for, I’m all for. I’m a huge fan reoccurring payment models and Verizon has one of the best. The P/E is still an impressive at 11.26 and at the current price per share is $49.66. It seems worth it for me. Frankly anything under $50 I’ll buy for Verizon. Just like anything under $100 for Johnson and Johnson (JNJ), I’ll buy.

The second is Main Street Capital Corporation (MAIN) I’ve been recently learning more about since Jason Fieber, of the previous glorious Dividend Mantra, brought this to my attention through his Facebook Page. Since he had a significant holding of it, I thought I’d give it a look.

Main Street Capital Corporation is a business development company focused on lending capital and expertise to lower middle market companies with annual revenue between $10M-$150M. WTF. I had to spend all morning looking up what Business Development Companies were.

Business development companies function similar to REITs where they typically distribute 98% of their taxable income as dividends to avoid corporate taxation. In fact, you could say business development companies are REITs for Businesses. They buy, improve and sell companies to make a profit.

I am still on the fence about this one since it’s high risk/reward and it’s heavily influenced by any kind of Fed Rate Hike. If it gets back down to $26 I may try it out. It has an attractive monthly dividend, meaning it pays it’s dividends monthly like Realty Income (O).

Third, I may get in on Kinder Morgan (KMI). I love that it’s essentially a pipeline toll road that oil companies will pay in order to move their natural gas. Recently the price has dropped from $44 a year ago to the current $17. People are waiting to see where the oil and gas movement will go, but I think it’s already hit bottom and will slowly move up. If there is one oil & gas business model I can get behind, it’s Kinder Morgan.

I just need to understand their tax structure better……

Have you bought Apple recently or have any other recommendations for Stocks to watch out for?

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Spoiler Alert: I now have a portfolio worth roughly $7,000 and with an average yield of 3.43%. It generates $21.04 a month. To give you some perspective, my portfolio generates enough monthly income to buy 70% of the items in Walmart, a nice dinner out or a subscription to both Netflix and Spotify ($10 each). This is cool, because I have literally done nothing to earn this. I just invested in companies I believe in and they pay me in dividends. Thank you companies.

Now, what companies have I invested in? Check out my portfolio and income reports to figure out which stocks I’m into and how much I make from them.

Lately, I have bought positions in only a few companies. I often like to invest in companies that have a sustainable cash flow like REITs that they have 20-year leases where they can depend on those clients to continually pay monthly rent.

I also like Verizon (VZ) because those stores are always packed and if people are willing to wait 45 min to get a new phone, they will likely continue to stick with this company for their phone plans. In fact, this month I have bought 10 more shares of VZ at $51.10. They are having some issues with employee strikes so the stock price has decreased a lot, but I don’t see this lasting. In fact, I’ve been trying to pick up more shares. Verizon has large network and they can rely on their clients to continually pay for their phones and let’s face it, people like their phones.

Otherwise, I have been trying to average down on a number of my current positions like Wells Fargo (WFC), Procter Gamble (PG), Digital Realty Trust (DLR) and Iron Mountain Realty (IRM). Mainly because I believe in these companies and I’ve done the research to know that it’s a fair price. The biggest thing is I’ve had some extra cash lately and rather than looking for new positions, I’d rather just increase my positions in my current companies. Remember it’s not always about buying more companies, but rather having a portfolio of companies that you believe in. That can be as big or small as you’re comfortable with. Currently I’m comfortable at owning 14 companies.

Another fun company I’m excited to be with is Comcast Corporation (CMCSA) which I’ve written about before, but I have been thinking about increasing my position with them. I now own the internet! Comcast and Time warner have a nice monopoly on access to the internet and let’s face it, people want/need the internet. We keep talking about cloud networks, apps, and cat videos on YouTube and Comcast is one of the kings to the gates of the internet. When you move into a new apartment (which I’m doing soon) internet is likely the first thing you’ll buy. More likely before food to be honest. I know I will. I have ramen and protein shakes, now give me my internet!

I will note that I’ve increased my positions in both VZ and CMCSA because while Comcast is one of the leading internet providers, I see VZ as an up and comer taking a piece of this market. There may be a time where people get their internet all from their phone via satellites using Verizon’s network. I am not positive this is the way that the market will grow, but I see it as a possibility, and I’m comfortable increasing my positions.

Do you have any recommendations for companies with subscription-based business plans?

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

I love REITs. OK, I love any business model that receives regular payments for just owning something and letting others use it. Imagine owning a car and someone paid you just to drive it. No matter what happens, you are getting paid. You can use that revenue to keep your business afloat and invest in new endeavors.

Roughly around 50% of my portfolio is currently in REITs. I love the high yields and business model, but they aren’t the companies that follow the subscription theory, here are some of my favorite companies that have a consistent reoccurring revenue business model.

Verizon – Nearly everyone has monthly cell phone payments, and even when you pay those off you’re paying monthly just to use the phone and data. Each month Verizon is making a profit off you and you’re not likely to quit using your cell phone. Plus with Verizon becoming a major player, it’s one of my favorite subscription business model stocks.

Aflac Incorporated – While I hate paying for insurance, everyone has it. You pay monthly in the event that you may need financial assistance in case something happens to you. I don’t know too many people who can say that they’ve received more from insurance than they’ve put in. For the fact that people will pay their monthly insurance bill regardless of economy, I like this subscription model.

Microsoft – While I believe their cloud service is subscription based, I am really anticipating Microsoft to make all their software this way. Currently they have made strides making Microsoft Office 365 subscription based for around $99 a year. I think this will be the trend for Office Home & Business in the future as well as their operating system, Windows. They are the main player in the market of office applications and if they do this, everyone will continue to pay. Even Apple is now bundling Microsoft Office when you buy a laptop or iPad, if Apple has given in, so will I.

My latest REIT though is Iron Mountain Incorporated (IRM) which I bought 8 shares at $31.46. I like this company for the same reason I like Digital Realty Trust (DLR). IRM sells data space (in addition to physical space for storage) for companies. So companies will pay monthly for IRM to hold on to their records be it digital or physical (some laws require you to hold onto paperwork for up to 7 years). This is where IRM comes in handy since physical paperwork takes up space and in the corporate world, every square foot counts they are willing to foot that monthly bill. They are utilizing their current assets for storage and investing in digital storage space for the future. I love a company that looks ahead.

Lastly I recently invested in 4 shares of Comcast Corporation (CMCSA) where I bought in at $59.93 a share. Yes, their customer service is awful and yes there are fewer people paying for TV subscriptions, but I like them for their internet provider service. People now-a-days can’t live without the internet and in many places, Comcast is the only option or cheapest option and they will continue to pay monthly through thick and thin. I believe Comcast’s internet service will continue to grow and I’m excited to hop on board. Especially if telecoms move toward a “The more you use, the more you pay” model towards internet usage. It’ll cut down on Netflix subscriptions, but be great for telecoms.

Do you guys have any subscription based business stocks you favor?

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

To be safe, I usually keep some cash in my checking and saving account. If I have too little cash, I may not have enough liquid to cover emergencies. If I have too much cash, then my money is just sitting there only earning 1% interest.

So what do I do when I have too much money in my bank? Well if you’ve read this blog before, you know I invest it, but how to invest $1,000?

I’ll tell you. I bought a boat load of stock in Realty Income (O) also known as the monthly dividend company.

Here’s why I invested in Realty Income (O)

There is something incredibly satisfying knowing that you have a monthly check coming in from places other than day job. I know every month usually around the 15th, Realty Income will deposit around $4.64 in my account just because I have a $1,289.52 stake or 24 shares in their company now. Plus this stock value will continue to rise since they have a great business plan that I can’t talk about enough.

Realty Income owns 4,400 properties that pay a monthly rent check. They use that money to pay down their debt and also purchase additional properties to grow their empire and stock value. Another portion of that rent check is distributed among all of their shareholders as dividends. So I receive the $4.64 dividend and their stock price will continue to climb as they build their empire. Cool right.

Now I will caution, there are risk like any company but I feel these are worth it and this company has been around since 1969 will likely be around for a while longer. People have to keep paying their rent and when I say people, I mean their long time lease clients such as Walgreens, CVS, Dollartree and other staple companies in the community. Even if some of them don’t, Realty Income’s real estate empire is so large, it’ll take a lot of companies to default at once to even make a dent. That’s why I am comfortable depositing the full $1,000 into this stock, and being a small time investor, that’s alot for me.

However I will probably focus on other stocks now since 36% of my portfolio is in this company (that’s a lot). They say diversity is the best strategy, and who am I to argue. I just saw a great opportunity to get in on this company and I’m very happy I did. My monthly dividend income of my entire portfolio is now $10.38! I broke the $10 benchmark which is awesome! You have no idea how excited I am about this. That’s $10 I will receive every month for the rest of my life.

It’s exciting whenever I have extra cash to buy stocks. These are the latest purchases to get me caught up on all the stocks I’ve bought over the last couple months. Each of these are stocks are dividend producing stocks, which in a couple years (like 20), these will be my monthly paycheck.

Realty Income (O) – 4 shares @ $46.51

Digital Realty Trust (DLR) – 2 share @$69.80

The Clorox Company (CLX) – 1 share @ 123.42

CenterPoint Energy (CNP) – 5 shares @ $18.70

LTC Properties (LTC) – 6 shares @ $42.64

Microsoft Corporation (MSFT) – 1 share @ $53.20

Verizon Commutations (VZ) – 7 shares @ $45.71

I won’t touch too much on my further investment into Realty Income (O) since I expanded on this company in one of my first posts, my first stocks. This is such a great company since it’s a REIT that relies on tenants who will be in 20 – 30 year leases such as CVS, Walgreens, Dollar Tree etc. The income from those tenants go to Realty Income who, by being REIT, has to distribute 90% of that income to its shareholders. Pretty cool!

Digital Realty Trust (DLR) is another REIT that I’m excited to expand into. Like Realty Income, the business model revolves around real estate but focuses exclusively on data centers. Now why I like this. There is a large push by companies all across the board to expand into cloud computing. If this proves to be true, the Amazon, Microsoft and Apple companies of the world which are hosting cloud computing (a growing it quickly) will need a place to store all their data centers. That’s where I see Digital Realty Trust stepping in. I have increased my stake in this company by one share.

Let’s face it, everyone knows the Clorox Company (CLX) brand. It disinfects and cleans. That’s something everyone needs from hospitals to the everyday person. One of the things I like most about this company is that it’s stock price has steadily risen over the last 20 years. This is what I love. Companies that constantly produce dividends AND raise their own share price. The stock price is a little high for me, but it just keeps going up so I’m not sure if there is a bad time to get into this stock.

Oh CenterPoint Energy (CNP) what am I going to do with you? Oh wait, I sold. I picked up this stock after following Jason Fieber’s (Dividend Mantra) portfolio. He picked up this utility stock and provided an excellent description why. I think utility stocks are important and I plan to acquire quite a bit in the future. Utilities are usually incredibly reliable because they have a solid customer base and regular income since it’s a subscription based service. Now I bought this following the example of someone else without exploring it to much. So since I wasn’t 100% on board with it, I ended up bailing out on it as soon the stock went down in value. Another lesson learned, if I don’t believe in the company to succeed, I shouldn’t invest in it.

LTC Properties (LTC) is another one I threw myself blindly into after following the advice of another market guru. I try not to do that anymore. The logic was sound. LTC stands for Long-Term Care Facilities. LTC is a REIT that focuses on skilled nursing facilities. With everyone talking about the babyboomers now hitting retirement age, they need somewhere to go and LTC is one building nursing homes. Since I wasn’t completely on board with this company, as soon as the stock went down a couple dollars so I bailed. Now you need to know LTC isn’t the ONLY one building nursing homes, and I do hope to tap into this pool. I just need to do more research to find the best option that I can partner with to take advantage of aging babyboomers.

Only if I could have invested in Microsoft Corporation (MSFT) when Bill Gates was still tinkering in his garage all those years ago. Since I lack time travel, I’m investing now. A couple of years ago I would have been hesitant since Apple seemed to take over the world but hey, every office still has Windows and I don’t see that going away too soon. Plus with the company’s focus in cloud computing, Microsoft has recently grown quite a bit. The thing with cloud computing is its subscription based and those are the best type companies. Where the customers keep paying every month. I’m all about revenue streams. I will be looking for ways to increase my position in Microsoft in the future.

Now one of my most recent buys is Verizon Communications (VZ). As I said before, I love subscription based businesses and people love cell phones. I really like telecommunications because everyone has one and people are more likely now a days to go back home if they forgot their cell phone than their wallet now a days. It was a tossup between VZ and AT&T, but I like Verizon for their growth. Both of them have great yields but if I follow the trends, I see Verizon keeping on taking away market share from AT&T.