To many, college feels like a free-for-all — a time when young adults can experiment with freedom but continue to enjoy the safety and security of an academic setting. Though some college students work to pay their expenses, many more rely on student loans, savings, and their parents’ money to fund their four years of university lifestyle.

Unfortunately, those first four years of adulthood are more impactful on future success than many college students realize. Especially when it comes to personal finance, college years can lay the foundation of bad habits that make wealth and happiness much more difficult to obtain. Whether you are a college student or you know a college student, here are some bad money mistakes to be aware of during the next four years:

Skipping Scholarships and Financial Aid

Yes, you can get all your college-related expenses covered by student loans — but that doesn’t mean you should. Loans might feel like free money right now, but in a few years, your student loans are going to be a massive financial burden that dictates where you live, what kind of job(s) you work, and how much fun you can afford to have. If you want the rest of your young adulthood after college to be fun and rewarding, you want to limit your student loans as much as possible.

One of the best ways to reduce student loans is by pursuing scholarships and financial aid programs. There is an almost unknowable number of scholarships available through colleges and universities, local, state, and federal government agencies, and even private companies; many of these scholarships require a one-page application and can award thousands of dollars in student funding. Meanwhile, financial aid programs take many forms, from reduced tuition costs to work-study programs. Before you commit to anyone method for paying for college, you should research other potential options of income.

Abusing Credit Cards

When you are already accruing thousands of dollars of student loans, a bit more debt won’t hurt — right? Unfortunately, credit card debt is some of the worst debt you can accrue. Credit cards come with punishingly high-interest rates and low minimum payments, meaning that if you aren’t careful, you could be paying your credit card debt for far longer than your student loans. You should get in the habit of paying your credit balance in full every month — or not using your credit cards much at all.

Being Wanton With Personal Information

In college, it feels like you have to enter your full name, birth date, and social security number on a different document every day, but the truth is you should be careful to read and understand every request for any type of personal information. College kids are often targeted by scammers because they tend to lack the awareness of potential threats or the responsibility to keep their personal information safe. You should protect information that can be used to identify you — and your financial information, too — by keeping that data secret and by being aware of common scams.

Failing to Budget

Everyone needs a budget, and that is especially true of college students who tend to have high expenses and limited budgets. It is a bit easier to manage your money when you have access to personal finance software that can track your spending, automate savings and bill paying and work with you on maintaining your budget. You might ask loved ones for a money management tool for graduation if you can’t currently afford a robust service.

Ignoring Retirement

Retirement might feel like eons away, but after college, the years come faster than you think. Because retirement savings grow over time, the sooner you start adding to your retirement fund, the more money you will have available when you finally call your career quits. Even if you can use a college savings fund to pay all your expenses through university, you should consider getting a part-time job if only to help you build emergency savings and start contributing to your retirement. You can add as much as $6,000 to a Roth IRA every year, and you might as well max out those accounts while you can.

While you should take the opportunity to learn and grow during your college years, you shouldn’t allow your experience to sink your finances for life. By being aware of the pitfalls of money management in college, you can make smarter choices for your future.

We often hear that Millennials are terrible investors because most Millennials entered the workforce during the 2008 financial crisis. Afterward, many hesitated to invest after seeing their families lose money, and those who often invested very conservatively. Many have avoided stocks, even the more conservative high dividend stocks.

Which begs the question – have Millennials changed their investment strategies? Let’s take a look.

With 20/20 hindsight, most people would agree that not investing during the turbulent 2008 financial crisis was a regret. Shortly after, we saw one of the greatest economic booms to the economy and those who invested made some of the greatest returns.

At this time, Millennials are facing their second economic recession with the 2020 pandemic (or third recession if we count the 2001 September 11th financial swing). Being recession veterans, they’re betting on a strong economic recovery.

Popular Millennial Stocks

This has been seen by Financial Brokerage Platforms like Robinhood, popular among Millennials. The platform gained 10 million users from 2016 to 2020 and added 3 million users during the pandemic.

By living through a strong economic recovery, Millennials show they are more comfortable with the stock market and purchasing stocks with their creative ways to make money.

The primary stocks that Millennials are purchasing are tech stocks (Tesla, Microsoft, Apple). As well as companies with strong brand awareness (Virgin Galactic, Amazon, Peloton) according to Robinhood’s list of 100 popular stocks.

Interestingly, some of these popular Millennial stocks offer dividends and create a rise in dividend investing. Dividend stocks traditionally offer stable returns and lower volatility, providing comfort to those Millennials with the 2008 financial crisis still fresh in their minds.

Millennials are gaining regular dividends, and additional portfolio growth as dividend stocks have outperformed their peers from 1990 to 2015 (source).

What Are Dividends

If you’re not familiar with dividends, here is a short recap.

Dividends are a portion of the company’s earnings that are distributed to shareholders. In addition to the value of a company’s stock going up, dividends are an additional payment sent to shareholders simply for owning the company.

Dividend payments are sent typically monthly, quarterly, or on an annual timeline, and determined by the company’s board of directors.

The types of companies that usually offer dividends are traditionally more established companies.

Dividend Investing Is a Growing Trend

Dividend Investing is a growing trend investment strategy involving owning primarily stocks that offer dividends. The idea is that by owning enough stocks that offer dividends, those dividend payments can eventually entirely replace your income for retirement.

Retirees may save up a large retirement nest egg, but they will eventually need to sell those stocks for money in retirement. Often using the rule of 4% to get the longest life out of their nest egg. All while hoping their nest egg doesn’t run out before they die.

The benefit of dividend investing is that there is no need to sell their stocks by retiring on the dividend income. The dividend payments from your stocks can cover all your expenses till the end of life. This helps ensure you have a consistent income stream in retirement and the ability to leave a sizeable inheritance for your heirs.

Take into consideration Warren Buffett, arguably one of the greatest investors who ever lived. He has a $200 billion portfolio through Berkshire Hathaway, consisting of 47 stocks. Two-thirds of those stocks have one thing in common – they provide dividends.

What Is The Average Dividend Yield

We established dividends are a portion of the company’s earnings distributed to shareholders, but how much do shareholders get?

Each company sets its own divided as a fixed dollar amount per share owned. However, the industry typically gauges dividend amounts as a dividend yield. This is the dividend compared to the current value of the stock. So while the dividend amount is typically pretty consistent dollar value, the dividend yield changes daily as the stock price changes.

In the S&P 500, which gauges 500 popular American companies. The average dividend yield of the S&P 500 is 2.00%. So, for every $100 you invest in the S&P 500, you will earn $2 annually in dividend payments.

What Are High Dividend Stocks?

High Dividend Stocks are typically stocks that offer a dividend yield greater than the average 2.00%.

Typically high dividend stocks come from companies with strong cash flow such as:

REITs (Real Estate Investment Trust)

Oil & Gas Companies

Telecommunication Companies

Utilities

Banks

High Dividend Stocks do have risks. Companies have been known to offer high dividends to attract investors. However, they may have trouble maintaining their high dividend yield in the long term, and their stock price may suffer. You should always be careful about these and do your research.

Popular High Dividend Stocks

Here are some popular high dividend stocks that have strong brand recognition and high dividend yields.

Bank High Dividend Stocks

Citigroup (C) – Dividend Yield 4.74%

Citigroup is one of the big four banks in the United States and JPMorgan Chase, Bank of America, and Wells Fargo. They offer financial services such as consumer banking and credit, corporate and investment banking, and wealth management. Citigroup is referred to as too big to fail with a market cap of 90.7 billion. When a company is too big to fail, that’s a nice assurance that it’ll continue to keep up its dividend.

JPMorgan Chase (JPM) – Dividend Yield 3.55%

JPMorgan Chase is considered the largest bank in the United States and seventh-largest in the world by total assets. These amount to around $3.2 trillion. The JPMorgan brand is used for banking services, while the Chase brand is used for credit card services.

JPMorgan continues to have a healthy balance sheet and shows they’ll be able to maintain their high dividend stock even during a turbulent 2020.

Energy Company High Dividend Stocks

ExxonMobil (XOM) – Dividend Yield 10.19%

ExxonMobil is the third-largest publicly traded oil and gas company behind Chevron and Saudi Aramco. While oil prices have lately decreased and 2020 has not been kind to any stocks. ExxonMobil continues to maintain a high dividend stock for investors. Plus, there’s a comfort knowing the world will always need electricity.

Chevron (CVX) – Dividend Yield 7.07%

Chevron is another oil & gas company and recently overtook ExxonMobil for the world’s 2nd largest energy company. CVX has been a bit more conservative in its acquisitions and spending. Those choices have created a strong balance sheet for the company to maintain a great high dividend stock.

Edison (EIX) – Dividend Yield 4.53%

Edison is a utility company that generates, transmits, and distributes electricity in the United States, primarily in California. Utility companies like Edison have a fairly stable income stream as there is usually little competition, which helps them maintain high dividend yields.

DCP Midstream (DCP) – Dividend Yield 12.05%

DCP Midstream is also in the oil & gas industry, focusing primarily on transportation. They have 51,000 miles of natural gas pipelines and 44 natural gas processing plants in the united states, making it one of the larger midstream companies.

As they make a good portion of money transporting oil & gas, their revenue depends heavily on the oil price. Right now, oil is priced low, but as that changes, this high dividend stock has a potential upswing for growth.

Real Estate High Dividend Stocks

Realty Income Corporation (O)- Dividend Yield 4.64%

Realty Income is known as the monthly dividend company. Popular among dividend investors as they pay dividends every month. They are a real estate investment trust (REIT) that owns 6,541 properties in the United States, Puerto Rico, and the United Kingdom. They earn money through long-term leases on their properties, which uniquely positions them to weather most short-term economic swings.

Plus, their major tenants are Walgreens, 7-Eleven, Dollar General, FedEx, Dollar Tree. These companies aren’t easily going to get replaced by online eCommerce. If their stable cash flow wasn’t enticing enough, their high monthly dividend of 4.64% is pretty great.

Universal Health Realty Trust (UHT) – Divined Yield 5.01%

Universal Health Realty Trust is another REIT but focuses on hospitals, rehabilitation hospitals, free-standing emergency departments, sub-acute facilities, medical office buildings, and child care facilities. UHT earns money through long-term leases to these healthcare facilities located primarily in Arizona, Nevada, and Texas.

This stock has taken a beating during 2020. Healthcare facilities have had to put off higher-paying services as they adapt their facilities for COVID. Even with the recent stock price fall, it still offers an attractive dividend with growth as the economy improves.

Simon Property Group (SPG) – Dividend Yield 8.02%

Simon Property Group is another interesting REIT on this list. They are the second-largest real estate investment trust in the United States with a significant portfolio in malls, outlets, and large complexes with big-box retailers.

However, the rise of eCommerce has been brutal to Simon Property Group. Plus, 2020 has not been kind to in-person retail. Simon has many assets but needs a significant plan to navigate a future post-COVID and continue to compete with Amazon.

Iron Mountain (IRM) – Dividend Yield 8.99%

Another high-dividend stock on our list. Iron Mountain stores information. They store physical records as well as digital records for companies around the world. This includes 220,000 customers throughout North America, Europe, Latin America, Africa, and Asia.

With over 1,500 storage locations, including underground caves for added security, Iron Mountain is a great solution for companies needing secure offsite storage. Also, they’ve seen significant growth in digital storage. Their recurring revenue through storage services helps maintain their high dividend stock.

Telecommunication High Dividend Stocks

Verizon (VZ) – Dividend Yield 4.3%

Verizon is a well-known brand as they offer wireless telephone services to around 93 million people across the United States. Making it one of the largest phone services in the country. They primarily focus on wireless connectively, making about 70% of their revenue.

Also their Verizon Media Group, they earn revenue from their acquisitions of AOL and Yahoo. Verizon has a strong recurring revenue subscriber base making it a great high dividend stock.

AT&T (T) – Dividend Yield 7.61%

AT&T has been a staple in telecommunications for ages. Their wireless telephone services make about 40% of their revenue, but they’re a bit more diverse. They also have DirectTV, Warner Media (HBO, Warner Brothers, Turner cable networks, etc.).

This diversity has helped AT&T stay relevant, but companies like Netflix, Amazon Prime, and Disney + continue to bite off their network tv revenue.

CenturyLink (LUMN) – Dividend Yield 10.14%

CenturyLink is now Lumen Technologies. A recent name change occurred in September 2020. Lumen is one of the United States’ largest telecommunication companies offering internet services to businesses (75% of revenue) and individual consumers.

With 450,000 miles of fiber connecting people to the internet, Lumen has the infrastructure smaller companies can’t compete with. This helps maintain its market share and high-dividend payouts.

Cisco (CSCO) – Dividend Yield 3.59%

Cisco is not well known by individual consumers. Yet CSCO is one of the world’s largest hardware and software suppliers for networking solutions for businesses. They help companies build their own networks with routers, switches, video conferencing software, data centers, security, and more.

What’s great is that they sell the physical hardware companies need and the software as a subscription for recurring revenue to support that great high dividend stock.

Technology High Dividend Stocks

IBM (IBM) – Dividend Yield 5.18%

IBM is a hardware and software technology company that focuses on cloud computing, artificial intelligence, commerce, data & analytics, IT Infrastructure, security, and a wide range of digital products. They have been paying a dividend since 1916 and considered a solid dividend payer.

They’ve recently made acquisitions of companies like Red Hat to reduce their dividend growth for a bit. These acquisitions will still pay off in billions for the long-term and help maintain IBM’s significant high dividend stock.

Aerospace & Defense High Dividend Stocks

General Dynamics (GD) – Dividend Yield 3.08%

General Dynamics is the 5th largest US defense contractor and business jet manufacturer of Gulfstreams. Being a defense contractor, they receive military contracts that are less susceptible to market swings. They currently have $82.7 billion in backlog, including two US Navy submarines, Abrams tanks, and more.

As United States Defense spending continuing to rise, General Dynamics will continue to benefit as a reputable company in the defense field. For investors, this could be a great high dividend stock to hold on to for the long term.

Insurance High Dividend Stocks

MetLife (MET) – Dividend Yield 4.68%

MetLife is the largest life insurer in the United States and one of the world’s largest as they operate in 40 countries. They make money from premiums, investing income before insurance payouts, and retirement solutions such as annuities.

COVID will certainly have an impact on the insurance business. MetLife is better positioned than other life insurance agencies to weather the storm and maintain its high-dividend stock.

Disclosure: I personally hold O, IRM, VZ, DCP, CSCO. This article was written by myself, and it expresses my own opinions. I am not receiving compensation for it. Nor do I have any business relationship with any company whose stock is mentioned in this article. For a full list of my entire stock portfolio, visit Wallet Squirrel.

This article originally appeared on Your Money Geek and has been republished with permission.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Making money while you sleep has a beautiful ring to it.

Earning passive income provides the opportunity to do just that. Today’s profitable passive income ideas will help you brainstorm your next money-making venture.

What is Passive Income?

Passive income is defined as income that requires minimal effort—or perhaps even zero effort—to earn. Passive income typically enables your money to work for you. It’s a “work smarter, not harder” situation. We can compare it against active income, where your effort is 100% correlated to your income.

The best passive income takes the least effort. But today, we will consider many popular passive income ideas that will earn you money, whether you want to pay off a student loan, dig out of credit card debt, or put together a retirement plan. As long as it requires little passive activity, it could be a decent passive income stream.

Those who achieve financial independence will tell you that passive income streams are the key to success. The problem is that most supposed passive income ideas that you’ll find are not passive at all. A second job, for example, isn’t passive.

Since you’re already busy with your everyday life, you want to find passive income that truly works while you sleep, or play, or socialize, or whatever you want to be doing with your time. Most income sources require you to put in a LOT of work. But that completely negates the idea of “passive” income.

Do you want to make passive income? You will need to invest in an asset that produces passive income for you. Since you’re not committing time to earn this passive income, you’ll need to commit to another resource (e.g., money). Unless you are receiving money the old-fashioned way (inheriting it), there’s no such thing as a free lunch.

The good news is that you don’t need a pile of cash to start your passive income stream. If you already have an asset that you are not fully utilizing, that can serve as your investment. We’ll get to how that works shortly.

For now, let’s talk about a few passive income strategies. Stop letting your money stagnate in a bank account and lose its spending power. Some of these next passive income ideas will get you ready to invest in your future. Passive income means you want to start valuing your time and your money.

Truly Passive Income Ideas

These first ideas—which we call “truly” passive—require a one-time investment upfront and zero future effort. There’s no upkeep, no fuss, no muss. These are some of the easiest passive income ideas that you could implement.

1. Alternative Assets

Alternative assets, or alternative investments, are much talked about these days. The volatility of the markets and extremely low-interest rates for the foreseeable future have many people looking for alternate options.

There are many types of alternative investments. Some of the more popular offerings are hedge funds, private equity, crowdfunded real estate investments, and commodities like wine or geeky collectibles.

We recently discovered another unique alternative investment, usually only available to the wealthiest of the wealthy: luxury watches.

We’re not talking about a $500, $1000, or even a $10,000 watch. Instead, investment-grade watches merit a price range from a minimum of $50,000 up to $1 million.

Why inform you about an investment with that kind of price tag? Because the company we’ve discovered—LuxeStreet, Inc—has made this investment available with a minimum investment of $10,000. You can buy partial shares of an assortment of watches at that buy-in level. If you’re an accredited investor looking for a unique alternative, you should take a closer look at LuxeStreet.

This particular luxury watch investment pays 12% per year at the rate of 1% each month. The best part of it is your investment is backed by luxury watches owned outright by Luxe Street. There are very few investments we’re aware of that pay that kind of an income.

Here is our full review of LuxeStreet, where you’ll find the offering’s details and get our thoughts on the pros and cons of the investment.

Pro: Alternative investments give you exposure to unique asset classes, different from everyday stocks, bonds, real estate, etc.

Con: Alternative investing is a fledgling industry with developing regulations. There’s likely to be more risk than with typical investment choices.

2. Passive Real Estate Investing

Talk to any landlord, and they’ll tell you that “passive” is the last word they’d ever use to describe having to replace a washing machine after an already full day. That’s plain old work.

However, many companies give you the ability to invest in commercial and residential real estate projects without actually doing the heavy lifting yourself. It’s often better having your very own real estate agent or other real estate professional picking the properties.

One example is DiversyFund. It’s a private REIT (real estate investment trust) that allows you to invest in professional real estate passively for as little as $500. I love companies like DiversyFund because they don’t earn money unless the investors earn money since they invest and manage the projects themselves. Having aligned incentives is important in investing.

Another detail that differentiates DiversyFund is how they invest. Rather than spread their expertise too thin, DiversyFund focuses its investments on lower-risk multifamily housing. They use technology to scour the country for properties that fit their specific criteria.

What criteria? Specifically, DiversyFund looks for high occupancy and positive cash flow properties, but that needs some work. These aren’t complete renovations. Instead, a typical DiversyFund property could just need an updated bathroom or kitchen, or maybe just a fresh coat of paint.

The fact that DiversyFund does all of the work themselves means they have lower costs than their competitors. After the aforementioned minor renovations, the upgraded properties merit increased rents. And that increases your cash flows and the value of the properties.

Holding periods for DiversyFund properties tend to be in the five-year range. Preferred returns for their properties are in the 7% range.

Both DiversyFund and their passive investors—e.g., you—benefit from this business model. When incentives are aligned, you give yourself the best chance to win.

Pro: DiversyFund does all the hard work for you, giving you exposure to residential real estate without requiring you to be a landlord.

Con: There’s always a give-and-take to using a third party—namely, their fees.

3. Earn Passive Income with Lending Club

If you’re looking for another way to earn passive income, you may want to consider Lending Club’s peer-to-peer lending platform.

Lending Club allows passive investors to diversify their assets by investing in different types of loans. Wait…in loans? That’s right. Lending Club allows you to loan your money out to people and groups looking for funding. The type of loans you choose will determine your investment return and risk exposure (remember, risk and return are related).

All you need to do is invest as little as $25 in a single loan. Your investment is combined with other investors to make up the entire loan amount. While others may invest more, many investors choose to stick with $25 minimums across multiple different loans. This diversification tends to decrease risk.

So how do you generate income with Lending Club?

After you make your initial investment, you will start earning passive income from the borrowers’ repayments. As a borrower pays down their loan, you will receive monthly interest payments.

Like all loans, Lending Club charges interest to the borrowers. These interest rates may vary and will be determined by various factors, including the borrower’s creditworthiness and loan amount. Even if you don’t reinvest your passive income back into the platform, you will still earn a return on your investment from this interest.

Since this is a peer-to-peer lending platform, you’re essentially the lender. That means that you collect the principal and the interest. After you’re repaid, you can choose whether to cash out or reinvest your funds in other Lending Club loans.

Pro: Lending Club allows you to help many different loan seekers while earning passive income yourself.

Con: If a few of your loaners cannot repay your loan, it can be easy to miss out on profits or potentially even lose money.

4. Invest in Dividend Stocks

Dividends are profits paid out to owners of stocks. Some companies pay dividends regularly, which means that dividends can become a dependable source of income.

Investors who love dividend-paying stocks will talk about their investment is generating dividend income and appreciating. In other words, they’re getting a regular supply of money (from the dividends), and the underlying stock is increasing in value (as the company grows).

Keep in mind that stocks with high dividends still carry risk. Dividend stocks can drop in value like any other stock. Historically, dividend-earning stocks drop in price less than the overall stock market. They tend to be steadier in the priceless upside, less downside. But you should never invest in any stock, a high-paying dividend stock or otherwise, without understanding that you’re taking a risk.

They are similar to other equities in that they’re usually best to buy and hold for a long time. And with that long-term mindset, it’s reasonable to purchase stocks even at all-time highs.

Some people even rely on dividend checks for their regular expenses. They receive thousands of dollars each quarter from their dividend investments. And that might require you to own a significant number of shares!

But if you have some extra cash to invest and understand the risk involved, dividend stocks are something to consider. Perhaps an index fund full of them would be right for you. Just make sure you learn about the risk (or lack thereof) from the index fund bubble.

Pro: A proven income stream with over 100 years of heritage, backed up by some of the world’s most blue-chip companies.

Con: “Prior results do not guarantee future outcomes.” Your initial investment could lose 50% overnight if the stock market crashes.

5. Open a High-Interest Savings Account

If you are afraid of investing, there’s a chance you have a decent chunk of change saved in a checking or savings account. Saving money is always a good thing.

Sadly, brick-and-mortar banks barely pay any money in interest. Institutions like Wells Fargo, Chase, Bank of America, and others pay around 0.08% interest. You could have $100,000 in that bank, and you’d earn less than $100 per year in interest. That’s nothing!

That’s why keeping your savings in a high-yield savings account is clutch.

The best high-interest banks are online-only, so you won’t need to mess with going into the bank to get started. The best part is that as of this writing (October 2020), they pay as much as 0.80% interest per year. So with $100,000 in the bank, you’d earn $800 per year. That’s much better!

Even if you don’t have a ton of money saved up, you will still make way more money than you would with a regular checking or savings account. One of my favorites is VARO Money. They consistently pay higher rates than almost any local or national brick-and-mortar banks.

You could also look into money market accounts, treasury bonds, or certificates of deposit for low-risk, stable return investments.

Pro: As safe as safe can be.

Con: Meager returns. In fact, inflation might cause you to lose buying power.

P.S. For passive investing or financial planning ideas, make sure you understand the tax ramifications with the Internal Revenue Service (IRS).

6. Long-Term Index Fund Investing

Do you believe that the global economy will continue to grow and progress? And do you have 10+ years to invest money and build eventual passive income streams? If so, index investing might be for you.

An index fund is a mutual fund that owns a wide assortment of assets. Some index funds are fairly focused (e.g., an automotive index fund might own all automotive stocks). Other index funds are broad (e.g., a total market index fund might own every single stock on the stock market.

Either way, the idea of index funds is that they lower risk by diversifying their assets, and they lower their costs by enacting simple asset ownership rules. Index funds don’t look for the needle in the haystack. They just buy the whole haystack.

Over the long run, index investing has proven to be a very successful method of portfolio growth. And if your portfolio is growing, you can skim off some of the profits as passive income.

Pro: Proven method of long-term monetary growth and successful retirement planning.

Con: Not a short-term passive income solution.

7. Become an “Angel”

Angel investing is a high-risk, high-reward proposition. It gets its name because it answers the question, “Who would invest in a startup company with no track record, no customer base, and no surefire path to revenue growth?” Answer: only an angel.

Of course, angel investing also provides a path to equity ownership in an eventual global company’s infantile stages. Could you imagine buying into companies like Shopify or Uber when they only had a handful of employees? Small angel investment can grow by 1000x! Of course, that same investment can just as easily disappear within 6 months to a year.

Angel investing is a feast-or-famine proposition.

Pro: Immense upside. A hands-off way to help entrepreneurs trying to change the world.

Con: As high risk as anything mentioned in this article.

Semi-Passive Income Ideas

We’ve got 100% passive income ideas out of the way. But there are still a lot of great “semi-passive” ideas that you can utilize. These take a bit more effort to execute, but they can still build long-term wealth.

1. Put Your Real Estate to Work

Utilizing your real estate is a great way to turn your property into rental income. You don’t have to buy a rental property to have rental property. Use what you already own!

1A. Use Airbnb or similar services

Rewind 20 years ago. Could you imagine that strangers would painlessly be staying in one another’s houses without ever meeting, talking, or interacting? Airbnb and similar services have revolutionized where we stay when we travel. And it has opened up serious passive income doors for you and me.

Unsure how much money you can make?

Simply log on to Airbnb and check out what your market looks like. There are sure to be other Airbnb hosts in your neighborhood. What are they charging for a room or their whole house? Would you be interested in offering up your room/house for that same price?

Granted, you’ve still got to ask yourself: is this money worth the effort? Being an Airbnb host isn’t truly passive. Sure, you already have the house (and that’s most important). But you still have to act as part landlord, part maid, and maybe even cook your guest some meals. That’s work.

But if you are excited by the idea of meeting new people and making some solid side cash, then Airbnb hosting might be perfect for you!

Pro: Meet new people every week while getting paid to do so.

Con: You have to become part landlord, part cook, part maid, etc.

1B. Rent Out an Extra Bedroom

If you own a home, there’s a decent chance you have an extra room that hardly gets used. Perhaps it’s the guest bedroom or kids’ old playroom. Consider renting it out for extra income.

Of course, hosting a long-term guest isn’t for everyone. There are some pros and cons to compare. The most obvious trade-off is a few hundred bucks in monthly rent compared to the inconvenience of having a guest in your home.

But if you don’t mind the company, it may be a no-brainer!

It’s easy to see how this could lead to a few thousand dollars a year. After several years, you’ll have accrued enough extra income to start planning an eventual early retirement.

Just make sure you both sign a formal rental agreement so that everyone is on the same page.

Pro: Turn an unused resource in your home into an income source. And hey, maybe you’ll make a new friend!

Con: Another person is living in your house…your kitchen…your bathroom. Even if they’re a saint, having a housemate can be tough.

1C. Rent Extra Land

Perhaps the idea of hosting someone inside your house isn’t for you. But how about hosting someone on your property by renting your extra land?

There is a tiny home bonanza sweeping the country right now. People are choosing to live in tiny homes and embrace a minimalist lifestyle. For a lot of those people, the only downside is where to place their tiny house. If they want to live in a tiny home to save money, it likely doesn’t make sense to spend hundreds of thousands of dollars to buy a land lot.

If you have some land, this creates an opportunity for you to rent out space on your lot. You’ll want to make sure you don’t violate any laws or codes in your city, town, etc.

But if you’re not using the land, why not get paid a few hundred bucks to let someone place their tiny home there? You’re making the most of a resource you aren’t using and giving someone else a place to live. Win-win.

Real estate income and rental properties are often considered passive, or at least partially passive. It might feel risky if we face another Big Short real estate bubble, but doesn’t it feel like rentals will always be needed? Either way, they are trendy methods to build long-term wealth.

Pro: Compared to other ways, you can share your real estate, this is pretty hands-off.

Con: Adding new buildings to your property can be a significant headache due to local laws and zoning codes. Do your homework!

2. Renting Your Car

Companies like Turo and GetAround are making it easier than ever to rent out your car when you aren’t using it. And let’s face it: if you live in an area with Lyft and Uber service, there’s a chance you might not even need your car daily.

You’ll want to keep in mind that renting out your car will mean additional wear-and-tear on your vehicle, so your repair bills might increase. But users have said it’s well worth it for the passive income checks coming in the mail.

If you have a second car sitting around or have begun to bike to work and no longer need the vehicle daily, this might be the perfect way to start generating some passive income.

Pro: A car is one of the worst investments you can make. But renting your car out makes that investment less bad.

Con: More miles = more repairs. And what if the car renter spills their burrito all over your nice clean seats?

3. Refer Friends to Great Products You Already Use

Companies like Rakuten.com (formerly eBates) have existing referral programs that pay out cash for every friend you can refer to. If you have many friends or social media followers, this can be an effortless way to earn money.

All you have to do is set up an account by clicking the join now tab at the homepage’s top. Once the account is up, go to your account settings and click where it says refer and earn to get a link to send your friends.

To find other programs like this, it’s super simple. Nearly any company that delivers food or other products have similar programs.

It takes a little effort up front and then some consistent effort to keep your friends or followers using the service.

Pro: Many people buy lots of things, and most people would like to save money if they can.

Con: You don’t want to be known as the “let me sign you up with my referral code” guy. There’s a fine line between passive income and alienating the people in your life.

4. Try Affiliate Marketing

I started a website from scratch. It was not an easy undertaking (unless you know what you are doing and have done it before). If you don’t want to build your site, why not find an existing website that is already earning money from affiliates and taking that site over?

Affiliate marketing is where you get paid a fee for referring new customers to brands.

For example, if you own a website that compares prices (e.g., something like Kayak.com), you can show price comparisons to your customer and then earn commissions for referring those customers to eventual purchases.

This type of investment can be genuinely passive if it’s already generating revenue with very little hands-on involvement. But keep in mind: if a site is making revenue, it will not be cheap to buy. Alternatively, a website might require some slight upkeep to make sure it runs smoothly and keeps your passive income coming.

Pro: Once the ball is rolling, you can make a lot of money very quickly.

Con: Creating a website can be tough. And buying one can be expensive.

5. Run a Site with Display Ads

Affiliate marketing isn’t the only way to make money online. Some websites sell digital products. But most common is to rely on advertising revenue as their primary source of building a passive income.

If you’ve spent any amount of time on significant sites like ESPN, The Weather Channel, Google, etc., then you’ve seen lots of advertisements on them. If you don’t remember seeing ads, then you either have a formidable adblocker, or you’ve learned to ignore them. Nice!

As you can imagine, these sites have ads on display because they get handsomely rewarded for doing so. The key to generating income in this way is to have a website with a lot of users. There is a strong correlation between the number of eyeballs on your website and the amount of income you’ll make. Easy enough to understand.

If you have a friend with an old site that they never use, it might be worth acquiring it if they have traffic. Adding ads to a website is super simple, and you could start earning some passive income quickly.

Pro: It’s the oldest and most consistent business model on the Internet.

Con: You’ve got to find the balance between earning money and driving away readers due to too many spammy ads.

6. Create a Print-on-Demand Online Store

Do you have a graphic design touch? If so, you could create iconic designs and sell them in an online store. Your customers can simply download the designs they enjoy and print them on their own.

Alternatively, you could outsource the printing to a third party—e.g., a customer orders one of your t-shirts, and a third-party print shop makes the t-shirt and sends it to the customer.

You’ve got to do some work upfront. What does popular culture enjoy, and how can you make graphic designs to meet that desire? This takes time, skill, and some open-minded knowledge about what the world wants.

But if you’re up for it, you can create a steady passive income stream from print-on-demand graphic designs.

Pro: A creative outlet that can lead to long-lasting passive income. Possible to outsource nearly all of the sustaining work.

Con: It’s possible to create a whole portfolio of graphic design that nobody actually wants. You’ve got to create something desirable.

7. Create an App

Are you a programmer? Heck, do you have a decent understanding of math and logic? If so, you can quickly teach yourself various app coding languages and start creating your very own smartphone apps.

As Marc Andreessen says, “Software is eating the world.” Everyone has a smartphone, and everyone is looking for ways to make their lives easier via software on those phones. The need is out there. Can you fill that need?

Where there’s demand, there’s an opportunity for passive income. Do you remember Flappy Bird?

In 2013, this simple single-player smartphone game seemingly took the world by storm, garnering millions of downloads. The app developer claimed to be making $50,000 a day from in-app advertising. And that game itself is incredibly simple.

Now, Flappy Bird struck gold. You and I might never be able to replicate that. But if you took a month to create an app and then made $20 per day for the next five years, that’d be close to $30,000 in passive income. That’s not too unrealistic.

Pro: App development is an industry that will only grow as smartphones become more ubiquitous worldwide.

Con: Requires specific domain knowledge, which can be a high barrier to entry.

Passive Side Hustles

These passive side hustles require a steady low-effort to execute. They aren’t fully passive but still can provide a lot of income compared to the effort involved.

1. Learn to Flip Products on eBay

There’s a chance that you know a certain product better than anyone else. Maybe it’s game consoles or cell phones. For others, it’s makeup, shoes, or handbags. The point is: you might be an expert and not even realize it.

You could earn a significant side income by learning the buy and sell that product for a profit on eBay. This is frequently called “flipping.” The learning curve may be a little steep at first. Once you get the hang of it, you can be churning out additional income regularly.

The beautiful thing about eBay is that there are so many buyers and sellers. All you have to do is find opportunities where you can buy products for less than they are worth (using your expertise!) and flip them.

Pro: There’s a lot of pure profit to be made, as long as you know what you’re doing.

Con: Dealing with anonymous parties can be tough, and eBay typically sides with the buyer over the seller. So if you’re selling for profit, it can be easy to get burned.

2. Use Your Washing Machine

If you don’t have money to invest, you may need to make money quickly. And if you have a washing machine and dryer, there’s a good chance you can start right away. Sound crazy? Maybe it is. But let me explain.

Several companies bill themselves as the Uber for Laundry, and they are pretty simple. You sign up, pick up clothes from people who live near you, and wash them. Once you deliver their laundry, you’ll get paid.

It’s that simple.

If you are enterprising, you could always pick up several different loads and head to a laundromat to wash several loads simultaneously. But be careful so that you know what to do with all of that cash you’ll make.

I recommend you invest in it!

Pro: Turn an unused resource in your home into an income source. You don’t need incredible skills to wash people’s clothes.

Con: Everyone has a different definition of “dirty laundry.” Are you sure you want to test yours?

3. Become a Tutor

Getting into top schools and programs is as challenging as ever. Getting a high-demand job is just as tricky. That means that there’s a lot of people looking for expert information. It might be how to pass a test or how to write a resume. So if you can tutor them, you could earn top dollar.

And the crazy thing is that with all of the new technology available, you can easily tutor kids in China and make money while sitting on the couch in Texas. Check out companies like VIPKid for online tutoring jobs.

You can make a lot more than minimum wage by working around your regular work schedule. This type of gig is perfect for those seeking to make extra money on the side.

Pro: You have a lifetime of knowledge. Someone out there is probably looking to learn what you already know.

Con: Teaching can be tough, and your students will expect results. How are you going to react when you’ve explained something ten times, and they say, “I still don’t get it.”

4. Become a Collectibles Expert

What do stamps, Beanie Babies, and Pokémon cards have in common? They are all niche collectibles with small but thriving markets. You can do a few hours of homework on a particular collectible and immediately become more knowledgeable than 99% of the population. And that knowledge is power.

People are selling their old “junk” every day for pennies on the dollar. If you develop the skills to recognize treasure from trash, you can turn their pennies into your dollars.

The world of collectibles is incredibly diverse, ranging from old arrowheads to Christmas ornaments to classic books. But where there’s a paying customer, there’s an opportunity to earn passive income. If you do the homework up front, you could earn a serious side hustle passive income.

Pro: Niche markets where large differences in knowledge can lead to significant profit margins.

Con: An incredibly diverse range of products and a real risk of getting fooled by counterfeits (a.k.a. losing money).

5. Give Lessons

Are you a highly-trained athlete or artist? Do you have demonstrable skills, competitive experience, or professional licensure? Then you could make significant side hustle income by giving lessons.

The biggest customers? Parents and their kids. There’s a huge demand from parents who want their children to have good golf swings, nice singing voices, and the ability to speak in public.

And you don’t need to be a professional opera singer or a world-traveling tennis player. All you need is enough skill so that the parents and their children respect your expertise. There are plenty of former DIII athletes and local art teachers who make $50-$100 per hour by giving lessons in their expertise fields.

Pro: Lots of potential clients, a high demand for your skills.

Con: While the effort to acquire your skills is a passive sunk cost, the effort to give the lessons is quite active.

Residual Income

Passive income, semi-passive income, side hustles, and now residual income?!

You may think we’re wordsmithing or splitting hairs, but there is a difference between passive income and residual income. Though many who write about it don’t differentiate. Here is a perfect definition from Webster:

a payment (as to an actor or writer) for each rerun after an initial showing (as of a TV show)

The fee paid to an actor for reruns is the best representation of how I think about residual income.

Examples of Residual Income

1. Royalties

Let’s say you wrote a book. It could be an eBook (e.g., via Amazon’s Kindle direct publishing) or a traditional book published in print. The publisher pays you an upfront fee for the work. Once they recover that fee from sales, any additional income you receive (net the publisher’s cut) is residual income.

You’ve done the work by writing the book upfront. You only did the work once. Yet all sales proceeds going forward provide you residual income.

Pro: A steady income stream from now until you die.

Con: You’ve got to write a really good book (or make a good movie, show, etc.). It takes skill and hard work.

2. Product Sales

Not the writing type? That’s fine. Let’s say you’re a widget salesperson.

You sell the widget for a set price. Part of the sale is for ongoing service. The purchaser pays a monthly (or other) ongoing fee for your company to service the widget. The company receives the money, the service department handles the continuing service, and you get a piece of the ongoing fee from the service contract—that’s residual income.

In the insurance world, salespeople get an upfront commission for the initial product sale. The sale might be life insurance, property, and casualty or health coverage. After the original commission gets paid, the salesperson receives an ongoing residual income from the initial sale as long as the customer continues to pay the premiums. Service usually comes from the client services team, not the selling agent.

Pro: There’s a very high ceiling. Sales commissions and residual income frequently have no upper limits.

Con: Sales is a tough job. Your failures are very apparent and right in your face.

3. MLM Marketing

For those not familiar with it, MLM is multi-level-marketing programs. I’ll explain how it works below.

Before you go off on me for putting this in the post, give me a minute to explain. I’m not endorsing MLM sales or saying you can make money at it. However, the concept of MLM marketing is based on residual income.

In MLM programs, participants are encouraged to sell a company’s products. The participants get paid for that. But big money typically comes from recruiting others to sell those products under your account. You encourage those folks to recruit others, etc. The idea is to build a sales empire—sometimes shaped like a pyramid—and make a bazillion dollars. Sorry. The sarcasm got away from me.

People at the top of this food chain earn residual income via the people underneath them in their “line.” The folks at the top aren’t doing the selling themselves yet are making income from the sales of those underneath them.

Though similar in many ways, residual income isn’t the same as passive income in the traditional sense.

Pro: Turn your entrepreneurial spirit into passive income.

Con: MLMs are very controversial. Don’t get trapped by one, and don’t alienate your friends and family.

Buy a Small “Hands-Off” Business

Small business owners will tell you: it’s hard work, and there’s always something to do. Very few business owners would classify their income as passive. In fact, it’s probably the opposite of passive. It’s very, very active!

But some small businesses can, essentially, operate on their own. They might require a couple of hours of upkeep or a little bit of oversight, but that’s it! Let’s get to some examples.

1. Car Wash

Most modern car washes fall into two camps: they are either self-serve or fully automated. The car owner either gets out and washes the car themselves, or they drive up to a conveyor belt that sucks them through a tunnel of bubbles.

In either case, there are likely very few employees and almost no upkeep. All you have to do is make sure the soap is fully stocked, and the water is running. Sounds like the perfect job for a teenage part-time worker.

The upshot is: car washes provide steady income with almost no real effort from the owner. And that owner could be you.

2. Storage Rentals

People love stuff. And the more stuff they collect, the more likely they will pay a third party to store that stuff. And that third party could be you!

A storage rental facility requires some significant overhead upfront, but then…well, it requires almost nothing. All you need is one employee to oversee the lot and handle the customer sign-ups.

You collect regular monthly rental fees, just like a landlord. But unlike a landlord, you’ll never get midnight phone calls because the furnace stopped running. The storage facility—and all the stuff within it—just sits there. And you just collect your cash.

3. Laundromat

Last but not least, the laundromat is another great “hands-off” small business that could earn you passive income. Perhaps you’re underwhelmed since you’ll only be collecting profits $2.25 at a time. But think about it: what are your costs?

You’ve got to keep the lights on. You pay for water for washing and electricity for drying. But otherwise, the customers do all the work themselves! Dozens, if not hundreds, of customers, might use your laundromat on a typical day. That could easily add up to thousands of dollars per month, most of which is pure profit!

So after the initial start-up costs have been paid, what’s left? Passive income until the cows come home.

Pro: Very high potential for long-term passive income, with a small amount of active work as a business owner.

Con: Likely requires a high setup cost and is probably not fully passive.

4. Become a Franchisee

What if you could open a business that had worldwide recognition from Day 1? That’s what you can do by becoming a franchisee. The most common example of this occurs with popular fast-food chains like McDonald’s or Burger King.

Most individual fast-food restaurants are not owned and operated by the main corporation, but instead are owned and operated by a local small business owner a.k.a. the franchisee. This person might pay rent or licensing fees to the main corporation, but they keep most of the restaurant’s profits for themselves.

If you want to turn this idea passive, hire good employees to manage the franchise for you. They deal with the day-to-day operation; they deal with the headaches. You collect the profits.

Pro: An established business model with a very high ceiling (e.g., multiple locations at high-profit margins)

Con: Requires high initial cost and can easily become non-passive if you have a difficult time “letting go” of your involvement

5. Buy ATMs

Where do those fees go when you use an ATM? Answer: straight to the ATM owner’s pockets. And those pockets could be yours.

If you find a good location for an ATM, you can make significant amounts of passive income. The key is finding an under-utilized area with a high density of people needing cash.

Much like the laundromat or car wash, it might feel like earning 2 dollar ATM fees is a slow path to wealth. But it’s incredibly hands-off, and the customers do all of the “work” themselves.

Pro: Very hands-off. Good business model as long as people need money (and they always do).

Con: Requires a great location. And your business involves an unguarded box full of cash. That’s risky.

Other Simple Ideas

Here’s a quick list of some of my final ideas to generate passive income. If nothing else has struck you fancy so far, you can earn some cash flow from these different passive income recommendations. When it comes to creating passive income, nothing is too crazy.

Cashback Credit Cards or Cashback Rewards Cards. If you’re spending money anyway, you might as well get some cash back for it.

Vending Machine Business. Owning a vending machine(s) can be a low-effort tactic to earning a steady income. Just remember—location, location, location!

Start YouTube Channel(s). Do you have a message to share with the world? A bent for videography? A personality that people want to watch? If you gather a following on YouTube, you can earn a significant passive income from advertising revenue.

Create an online course. Do you have something you can teach the world? There are plenty of paying students who would buy your course.

Remember, generating passive income requires creativity and some initial work to set things up. If you’re already busy, that’s even more true for you. You’ve got to consider the value of time!

But if you can take the time to learn whatever you think you’d be good at, you can make some passive income. Maybe a lot of passive income. Did you think of any different income streams today? Create your own income streams! It’s good financial cents…er, sense…to start building wealth in your life.

I hope you can find at least one of these ideas intriguing enough to give it a try. Don’t listen to the negative nellies or the pounding pundits of pessimism (credit to Brian Wesbury for that one). Do your homework. Understand how much passive income you need. Learn what you need to know. And give it a try. You just might be the talk of the town because you’ll be making money while everyone else is breaking their back.

This article originally appeared on Your Money Geek and has been republished with permission.

It is jaw-dropping when the news announces So-And-So has been released on bail for $400,000. Many people have never been in that situation to know what is bail, how does bail work, and do you get bail money back. Here’s a short recap on everything you need to know about bail and the money behind it.

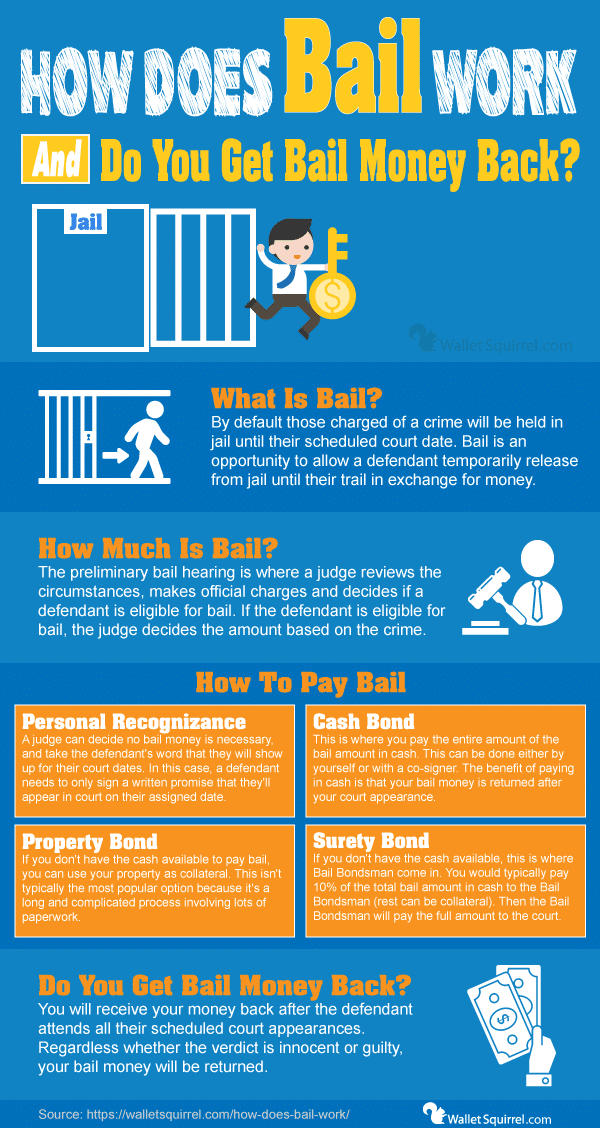

What Is Bail?

When someone is charged with a crime and booked by law enforcement. By default, those charged with a crime will be held in jail until their scheduled court date. Bail is an opportunity to allow a defendant to temporarily be released from jail until their trial.

Considering court dates often take weeks or months after the initial arrest, bail is often preferred to waiting in jail.

Cash Bail System

The United States is largely a Cash Bail system. Meaning you are required to stay in jail until all your scheduled court dates, that is unless you can pay the court money for bail.

In order to be granted bail, a defendant must pay the court in exchange for temporary release from jail until their scheduled court date. The amount of money paid is typically set at a base amount per alleged office, but judges have a large amount of discretion in raising it, lowering it, or completely waiving it at the preliminary bail hearing.

Many states are working to abolish cash bail. States including California, Alaska, Washington D.C., and New Jersey have completely abolished it or limited cash bail because it heavily favors the wealthy. Poorer individuals who don’t have money for bail are stuck in jail for weeks or months until trial. This leads to further financial hardships as they are forced to miss payments, miss work and potentially lose their job and go into debt before they can even attempt to prove their innocence.

How Does Bail Work?

So let’s say you’re arrested for a crime you may or may not have committed. Law enforcement is first going to take you to the local police station for booking. This entails providing general information (name, address, etc.), mug shots, fingerprints, and a criminal background check. After your booking process, and the well-known “one free call”, you are placed in a station jail cell with other recent suspects.

What happens next in the “how does bail work” process is the preliminary bail hearing. This occurs usually within 48 to 72 hours after the booking. The length depends on when you were arrested because courthouses are typically only open on weekdays.

The preliminary bail hearing is where a judge reviews the circumstances, makes official charges, and decides if a defendant is eligible for bail. If the defendant is eligible for bail, the judge decides the amount, if any.

When a judge sets a defendant’s bail amount, they are starting from a base amount according to the severity of the crime. Then they weigh additional considerations such as the defendant’s criminal record (if one exists), past experience showing up for court, flight risk, ties to the community, and whether they are a danger to themselves or others. These all factor into the judge’s consideration, who ultimately has the final say in the bail amount.

Not until a bail amount has been set in the preliminary bail hearing, can a defendant be released from jail on bail.

If you find yourself in this situation, consider having your lawyer present for the preliminary bail hearing to help plead with the judge and reduce any bail amount set.

How To Pay Bail

Once the preliminary bail hearing has set the bail amount, it can be paid in cash, money order, or cashier’s check to the Clerk of the Court.

There is a lot of confusion about the terms bail vs bond, but they have two distinct meanings. Bail is the process that allows a defendant to temporarily be released from jail until their trial date. While the bond is what the defendant provides to the court in exchange for bail.

Bond is usually cash, property, or another one of the different types of bail listed below. Think of the phrase “A person’s word is their bond”, except most courts prefer money to be the bond.

Types of Bail Bonds

Since a bail bond is how a defendant affords bail, there are different types of bonds. Think back to our initial “how does bail work” example of So-And-So was released on a $400,000 bail. That doesn’t mean So-And-So had $400,000 in their bank account ready to hand over, although they may have it or used crowdfunding. Here are the different types of bail bonds that help people afford bail

Personal Recognizance – A judge can decide no bail money is necessary, and take the defendant’s word that they will show up for their court dates. In this case, a defendant needs to only sign a written promise that they’ll appear in court on their assigned date.

Cash Bond – This is where you pay the entire amount of the bail amount in cash. This can be done either by yourself or with a co-signer. The benefit of paying in cash is that your bail money is returned after your court appearance.

Property Bond – If you don’t have the cash available to pay bail, you can use your property as collateral. This usually isn’t the most popular option because it’s a long and complicated process involving lots of paperwork. Additionally, the property you use as collateral typically needs to have a value of 150% or more of the bail amount. Although that varies by state.

Surety Bond – If you don’t have the cash available, this is where Bail Bondsman comes in. This is often a popular option as people don’t typically have thousands of dollars around to post bail. In this case, you can enter a Surety Bond agreement with a Bail Bondsman to pay for bail.

What is a Bail Bondsman

A Bail Bondsman is a licensed agent who helps with Surety Bonds. This usually involves paying 10% of the total bail amount in cash to a Bail Bondsman, and the remaining amount can be personal collateral such as property, cars, jewelry, etc. Then the Bail Bondsman will pay the entire amount to the court (if necessary) for your release on bail.

The Surety Bond makes the Bail Bondsman responsible for the defendant showing up for their trail. If a defendant doesn’t show, the Bail Bondsman is left on the hook. The Bail Bondsman will lose all the money they paid for the defendant’s bail and thus will make every effort to track the fleeing defendant to recoup their losses. This is where you find popular tv shows like Dog The Bounty Hunter make a living chasing down people who broke their Bail Bondsman agreements.

How Do Bail Bondsman Make Money

When you enter a Surety Bond with Bail Bondsman, you typically pay 10% of the total bail amount in cash. This upfront cash is usually kept by the Bail Bondsman as their fee for the risk their taking. The total amount varies by state and even the individual Bail Bondsman. This hefty fee is the downside of using a Bail Bondsman.

How Long Does It Take To Get Out of Jail After Posting Bail

Once the bail amount is paid and signed for, the paperwork usually takes 4-8 hours to be processed before you can leave. This is an average, but some cases can take up to 12 hours. There are a number of procedures the jail must ensure before releasing an inmate. It all depends on the jail and their current workload.

Bail Conditions

Once out on bail, there may be certain conditions you must follow. Each judge decides their own conditions at the preliminary bail hearing based on the particular case. You may have some, none, or all of these common bail conditions.

Travel Restrictions

Mandatory Check-in

Staying Alcohol & Drug-Free

No Weapon Possession

Employment Requirements

Mandatory Classes by the Court

No Contact / Stay Away Orders

How To Bail Someone Out Of Jail

If a friend was arrested and used their one-free-call to ask for help. Here are the steps on how to bail someone out of jail. First, identify where they’re located and when their preliminary bail hearing is scheduled. Second contact your friend’s lawyer or help get them a lawyer. The sooner you have a lawyer involved, the better.

Otherwise, there isn’t much you can do until the preliminary bail hearing within 48 to 72 hours after booking. Only then can you figure out how much it will cost to bail out your friend.

Do You Get Bail Money Back

You will receive your money back after the defendant attends all their scheduled court appearances. Regardless of whether the verdict is innocent or guilty, your bail money will be returned. However, some courts may take a fee for administrative court costs.

The entire bail process is simply the defendant promising to attend their scheduled court appearances. Money is provided to the court to ensure the defendant keeps their promise and once that promise is met, the money is returned. The only exception is if you did a Surety Bond with a Bail Bondsman, the upfront money you paid (usually 10%) is kept as their fee.

What Happens if You Don’t Show Up For Court

If you fail to keep your bail promise to attend your court date. Your initial bail money is forfeited to the court and a judge will issue a warrant for your arrest.

If you missed your trial, you may petition for a reinstatement of your bail instead of forfeiting it. However, it would have to be an incredibly good reason for missing your initial trial.

Wrap Up

Hopefully, this helps makes bail feel less scary and provide a better understanding of how does bail work.

Bail is simply the process of being temporarily released from prison until your court date. This happens through an exchange of money (the Bond) for the court to hold until your return. Once you return for all scheduled court dates, the court returns your money minus any court fees.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

While most of us have our own personal and specific financial goals, we also share many common goals and generally want similar outcomes when it comes to money.

We want to earn more money. We want to retire at a reasonable age. We want to improve the relationship we have with our money. And we want to find ways to manage our money better and save thousands of that hard-earned money.

Good money management practices are often a result of hard work, dedication, and an ongoing commitment to the long-term. But what it boils down to is simply taking initial action. In fact, you’d be surprised by how much money you can save by taking a few small steps.

The below tips are 10 easy, effective, and proven ways to help you save thousands of dollars this Fall and any other season. The best part is that each of these tips only takes anywhere from a few minutes to around half an hour to either start or complete.

1. Review and Compare Auto Insurance Quotes

Time it takes to complete: 30 minutes

Estimated cost savings: $100 to $1000

Comparing and shopping around for new automobile insurance every 6-12 months is a sure way to either save a few hundred dollars or at least to ensure that your policy doesn’t increase gradually.

Two fundamental principles make doing this worth your while.

First, insurance providers regularly adjust their prices, and policy rates fluctuate dramatically, even over a 12 month period. Second, the industry is highly competitive, which means that companies are always fighting to get new business.

Previously, one of the best ways of doing this was to do a quick Google search to find the best providers and to get a quote from multiple providers one at a time. However, thanks to insurance marketplaces like Gabi and Policygenius, it takes relatively no time whatsoever to get access to multiple quotes from top providers in just half an hour or less.

Depending on when the last you’ve done this was, you’ll be able to save yourself more than a few hundred dollars easily. If it’s been a few years since you’ve reviewed your auto insurance policies and gotten quotes from multiple providers, there’s a good chance that you’re leaving money on the table. When you mix in additional insured drivers on the policy, your cost savings will likely increase compared to individual policies.

2. Build a Free Financial Plan

Time it takes to complete: 5 minutes

Estimate cost savings: $500 to ~$2,000

A financial plan is one of the best tools you can have available to you. Your plan is like the north star of your current and future financial picture, guiding you through your decision making and showing you the exact next steps you need to be taking.

The real value of any true financial plan is that it’s holistic. It considers every major area of your financial life, rather than focusing on just one area. By being able to look at your income, savings, investments, insurance, and estate plans, you’ll uncover your financial strengths and weaknesses that will help pave the way for your road to success.

The good news is that financial planning applications like Savology can provide access to free financial planning. This can help you avoid paying anywhere from $500 upwards to $2000+ from fee-based planners.

To make the most of your financial plan and to continue improving your chances of success, it’s critical to make sure that you’re reviewing your plan and the progress you’re making at least every three to six months.

With the abundance of online subscriptions and memberships available, it’s easy to assume that there are a few online subscriptions and memberships of your own that you are not using nearly as much as you should be.

Ask yourself this: How many channels from your 200+ cable package are you actually watching? If you’re subscribed to services like Netflix, Prime, and/or Disney+, are you using them enough to justify their monthly rate? On their own, they’re relatively cheap, but when you add them up, these costs can start to stack up quite considerably.

Personally, we recently removed Disney+ and Netflix (well, we are now on a family tier), which saves us around $20 every month, adding up to more than $200 every year.

When you’re reviewing your online subscriptions, it’s important not to overlook memberships such as your gym membership and industry-related memberships. The bottom line here is that you really need to consider whether or not you’re getting your money’s worth. There’s a good chance you can find free alternatives that can easily save you another few hundred dollars of your well-earned money.

4. Eliminate Your High-Interest Debts and Loans

Time it takes to complete: 5-10 minutes (to review)

Estimated cost savings: $100 to $1000

High-interest, revolving debts like credit cards are a sure way of killing your financial plan and getting in the way of your ability to save. Instead of saving, your hard-earned money is directly being used to pay for interest payments.

By paying down your debt, you’ll be saving yourself hundreds or even thousands of dollars in interest payments over time. When you’re working on paying off your debts, focus on the accounts with the highest interest rates, and start paying those down first. Once you’ve finished paying one-off, work on the account with the second-highest interest. Continue in that order.

You’ll soon find over time that it’s not as hard as you once thought it was to pay down your debts, especially when you tackle them in order of highest-interest first.

For better results, create an action plan for paying down your debts and stick to it. This plan will help you stay focused and committed to tackling your debts most effectively and freeing up cash flow so that you have more available cash to save and use in other areas.

If you’re unsure where to start, consider using a debt payoff planner like Savvy, or similar alternatives, that can help you get out of debt entirely by taking baby steps.

5. Get an Accountability Partner

Time it takes to complete: 5 minutes (to get one)

Estimated cost savings: $1000+

An accountability partner also referred to as a success partner, is exactly what it sounds like. A person who’s there to hold you accountable for the decisions and actions in your financial life.

Early on, you and your accountability partner need to have a conversation about expectations and how you both foresee the relationship going. Like any relationship, you need to share information (and likely details) of what you are working on and be comfortable asking for their help to get you there.

When you find your accountability partner, I highly recommend having regular “check-ins” and conversations about money the same way you would have a regular phone call with a friend or a scheduled one-on-one meeting with an employer. If this person happens to be a friend or a spouse, it makes regular conversations about money that much easier.

6. Challenge a Friend to a No-Spend Challenge for 30 days

Time it takes to complete: less than 5 minutes (to challenge your friend)

Estimated cost savings: $100-$1,000

The best way to save your money is not to spend it in the first place. Believe me, as someone who can be impulsive with my money at times; I know just how hard not spending it can be.

This is exactly where a no-spend challenge can help out.

Pick one week, or even month if you can, in your calendar and challenge a friend (it can even be your accountability partner) not to spend a single dime within that time period. If you want to make this challenge even more ‘fun,’ encourage multiple friends to get involved so that you can challenge and support one another while even keeping a tallying leaderboard to track spending amongst the group.

Keep in mind that it’s next to impossible to avoid spending entirely as you’ll have bills to pay, but pick one or two spending categories and challenge yourself with avoiding spending in those areas.

To really make the most of this challenge, keep any cash or cards you have out of sight and out of reach. If you have cash lying around, deposit it ahead of time. If you have cards, tuck them away somewhere safe and out of sight for the week or month.

You’re probably wondering what the prize is, considering this is a challenge. That one is completely up to you and your friends. But from what I’ve seen, saving well over a few hundred dollars is more than a good enough prize.

7. Freeze Your Credit Card(s) for One Month

Time it takes to complete: less than 5 minute

Estimated cost savings: $200-$1,000

Freezing your credit cards might seem like an odd thing to do, but it works.

When you have credit cards at your disposal every time you make a purchase, there’s a good chance that you’ll be inclined to use this card more than you ever need to. It reinforces bad habits. Not to mention, you might even find yourself using this card when you have cash available, which can potentially lead to more unnecessary spending by way of interest payments.

A good friend of mine tried this for herself, planning only freezing her cards for one month. It turns out that she kept her cards frozen for more than four months because she actually forgot all about having them or needing them. Those four months saved her more than $1,000 in excessive, compulsive spending.

By freezing your credit cards and keeping them completely out of sight, you’ll be resisting any urge you have of spending compulsively.

8. Automate Your Savings

Time it takes to complete: 30 minutes

Estimated cost savings: $120-$5,000

This is one that you’ve definitely heard before, and you are maybe already doing, but the number of people still not taking advantage of this continues to surprise me.

By automating your monthly savings, you’ll feel instant relief knowing that your money is being put to good use immediately.

The real trick here is just getting started—even if you can only save $10 from every paycheck, that’s still $10 more than you were previously saved. After one year, you’ll end up with $120 more than you had the previous year, without the interest being compounded.