Holy Crap! Interest Checking Accounts are a Thing

Until two years ago I didn’t know there were such a thing as an Interest Checking Account. I had a standard Wells Fargo checking account for 12 years making me zero money. Literally zip, so imagine my surprise when I discovered there are checking accounts out there that pay you interest like a savings account.

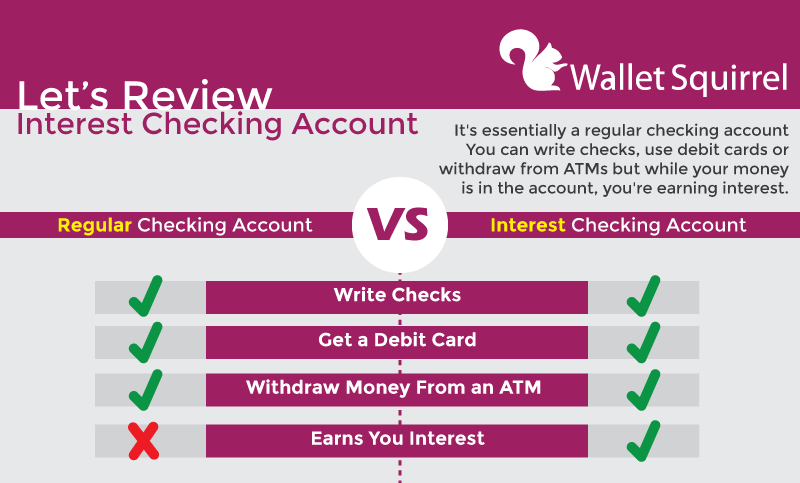

What is an Interest Checking Account?

It’s essentially a regular checking account You can write checks, use debit cards or withdraw from ATMs but while your money is in the account, you’re earning interest like a savings account.

Regular Checking Account vs. Interest Checking Account

How much can you earn in an Interest Checking Account?

It isn’t much, but better than zero. I have an account with Ally Bank and my Interest Checking Account makes 0.10% interest. To give you an idea. I keep around $4,000 in my checking account at all times. $2,000 is

To give you an idea. I keep around $4,000 in my checking account at all times. $2,000 is for my emergency fund and $2,000 for my monthly expenses. So that’s $4,000 sitting in my account making about 0.38 cents per month. See my Income Reports to see how it changes per month.

It’s not much, but over the last year, my Interest Checking Account made $3.66. That’s what I entered on my taxes last week.

My Personal History

Now $3.66 is more than I made on my Wells Fargo Checking Account, EVER! Keep in mind, I don’t mean to hate on Wells Fargo, but they simply never told me an Interest Checking Account was a thing.

They were like the cool kids in every high school (likely named Chazz). You wanted to hang out with them, even though you knew you they were dicks and there were better friends out there.

At Wells Fargo, if my checking account ever made interest, they kept it. Even my Wells Fargo Saving Account at 0.01% was earning less than my current Interest Checking Account. If I kept my $4,000 in Wells Fargo Savings Account for a year, I’d be left with $0.40 at the end of the year. THAT’S THEIR SAVINGS ACCOUNT!

Do a lot of Checking Accounts earn you interest?

Actually, most checking accounts I’ve encountered do not earn you interest. This is why I was so surprised when I discovered there are a few that do.

Many of my friends have a balance similar to mine with $4,000 in their account and some of my friends have up to $60,000 sitting in their checking account because they don’t know what to do with it. If you have that much, you should move it over to a savings account at least and hire a financial manager. I get the fear of the stock market, but there is no reason to keep that much in a checking account, especially not making you interest.

Conclusion

I’ve been wanting to do this post for a while now. It’s cool to share with people, who like me, didn’t know about Interest Checking Accounts. They exist! It’s not a lot of money, but it all adds up!

PS. I’m in no way sponsored by Ally Bank here. This is just my personal experience so far and if they start to F*!k up, you’ll hear about it

I hope I taught at least one person something new!

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Why not move the emergency fund money into the Ally bank savings account? They pay out a 1% interest compounded annually.that way you’d generate $20 per year.

It blows my mind to think someone has 60k in a checking account.

My logic was this. I have $2,000 in my checking account, I keep another $2,000 of my “Emergency Fund” in my checking account so I never overdraft. That’s a total of $4,000 in checking.

Then I keep another $4,000 in case anything really bad happens. So that $4,000 does earn the 1% interest.

Then if anything seriously bad happened, I can always take out of my stock portfolio and that’s only a 3 day wait to liquidate.

$3.66 is better than nothing, right? Most checking accounts don’t pay a dime, so that’s awesome you are able to get something for this! Similar to Diligent’s comment, does the bank also offer a higher yielding savings account for the emergency fund. I know you referenced liquidity in your response, but I’ve found that accounts within the same bank allow you to transfer funds on the date of transaction. So you could access the funds quickly if needed. But if you don’t want to do that, I understand as well.

Bert

You’re not wrong. I’m still about that extra $2,000 emergency fund as a buffer in case anything eats up my checking account and I get overdraft fees. Maybe I’m just oddly paranoid of that.

A savings account isn’t a bad idea, still way better than my buddy with $60k in a checking account. lol’

Thanks for stopping by Bert!

A lot of credit unions have interest checking accounts. 3% is pretty common. I’ve even seen 7%. Which is awesome…until you consider the caveats. Like having to make 10 debit card purchases a month, or check your balance through their website 4 times a month. Or it’s only on balances up to $5k.

I don’t make 10 debit card purchases a YEAR. Truth be told, though, I’m considering changing banks away from Chase; looking for a bank that offers ATM fee reimbursement, fee-free currency exchange, etc. Oh yes, and my savings account only gets $0.01 of interest per month. Maybe a credit union could work. I’d certainly like my cash to earn 3%+

That’s crazy having 3% Interest Checking Account, much less a 7%. Please send me the name of that bank if you find them again.

I agree about the 10 debit card purchases. We have a Credit Union in town (Bellco) offering a higher interest rate if you use their debit card 10x a month or something like that, similar what you’re talking about. I NEVER use my debit card for anything. I maximize the use of my 2% Cash Back Credit Card for every purchase.

Yea, 0.01% is insanely small for a savings account, you should really look into something else. It really does pay off switching banks if you crunch the numbers. Most people don’t switch banks often because it’s “hard”. Hence why alot of people stick with Wells Fargo even after all the scandals.

Good luck finding a Credit Union that works for you! It’s really exciting finding the right one. =)

What about all these high yield online banks?