There is no bad time to become a blogger. Simply the sooner you start, the larger a blog can grow. In this article, we’re going to show you how to start a money-making blog in under 5 minutes.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

At the end of last year, I was in a career funk. So I considered going back to school to get my MBA (Master’s of Business Administration). I figured with an MBA, you can practically do anything from advancing in your current field or make a complete switch to a new one. Every company values an MBA.

I was so excited! I previously considered the possibility of getting an MBA and my life was in a good position to do night classes. So I began picturing myself adding the letters “MBA” behind my name on business cards and looking up schools.

However, I quickly hit the brakes!

Ask These 2 Questions Before You Pursue an MBA

With many of my friends going back to school or are currently in school. I ALWAYS ask them these 2 simple questions that BLOW THEIR MINDS.

So I decided to ask myself these 2 simple questions to see if I can pass my own “Should You Get An MBA” test.

1. What is the EXACT dream Company and Job Title you want after graduation?

You should know this.

Most people get an MBA because they want to do something in business. They think they need an MBA for potential promotions or career growth.

However, what you should do is FIRST figure out what your dream job is.

You can’t just say “something in business”. If you are going to spend $140,000 or more on an MBA (average MBA costs according to Investatopia). Plus years of your life. You should identify the exact company and job title you want before you even start school. Come on, it’s your DREAM job.

This is a role you’ll potentially be doing for the rest of your life. You should have a clear idea of what it should be. Knowing this will guide every future decision you make within your MBA program, including the electives you take and the networking events you attend.

What’s the point of getting an MBA if you don’t know what you’ll do with it? Seriously? So take a moment and write down your dream job title and company.

2. Have you reached out to your dream company yet?

Once you can identify the exact job title and company you want, you should reach out to that organization and ask what they look for. This should ideally be less intimidating than pondering a future $140,000 MBA student tuition bill.

Usually, a company’s Human Resources department would be willing to meet with you if you tell them you’re considering going back to school to gain the skills necessary to work at their company.

When you meet with your dream company’s Human Resources Department (or any department), you should ask them some of these questions.

My dream job at your company is a Marketing Manager (or whatever it is), what is the typical salary range they get paid?

You should ABSOLUTELY know how much your future job pays because this will inform you how long it’ll take you to pay off your newly acquired student debt. Plus it’ll give you an idea of the lifestyle you can expect once you graduate with an MBA.

While it’s not all about money, you should be aware if your post-MBA salary can cover your student loans for the next 20 years. Are you ok with only eating peanut butter and jelly sandwiches?

What degrees or education do your current Marketing Managers have (or whatever your dream job is)?

This will give you an idea of the education level of their current employees. Some employees may have MBAs and some may not. You should probe deeper into what the HR team looks for in your dream position. Perhaps you don’t need an MBA and you may have the necessary experience to apply that day.

If you need to get an MBA for that position, ask if they have a preferred school or partner with any specific schools. If your dream job regularly partners with a local university and hires exclusively from there. That university may need to be on your radar for potential schools.

Does your dream company offer internships?

Yes, you’re getting an MBA but knowing if your dream company has an internship program is huge. Many companies will hire interns who are working towards their degree and help them grow into the position. There is no reason to wait till after you receive your MBA to apply to your dream company. You should use every opportunity to start making connections.

What does career growth look like at that company?

If your dream job is to be the Chief Executive Officer (CEO), they won’t just hire you out of school. What entry-level roles will you need to start off with and how does one become a CEO? How did the current CEO get his role and what did they do before that? Some jobs aren’t attainable right out of school, even with an MBA. You need to understand what your career path would look like moving into your dream position. You should understand what this looks like.

When I considered an MBA, I failed this checklist

Last year when I considered getting my MBA, I went full-throttle and visited 3 different universities. This included dropping in classes and meeting with professors.

I received all the brochures, met with all their “advisors” and compared costs ($39,000 – $80,000). I did soft applications and confirmed I would be accepted to each of them.

I was so freaking close to full-out applying.

I knew I wanted to do something in finance because I LOVED writing about finance (hence why I started a blog). So I figured I’d get an MBA focused on finance.

This is how most people start the MBA journey. They love the idea of a degree, so they first get an education THEN figure out where they want to work.

I know this because that’s how I choose my bachelor’s degree. I went into Landscape Architecture without actually knowing if it was my dream job. I just thought it would be fun to draw and select plants. I didn’t learn till after internship opportunities and after graduation that it’s not what I wanted.

So I took this MBA checklist and failed.

When I looked at my dream job, there were some finance positions like Financial Planner, Mutual Fund Manager, Financial Analyst that sounded interesting. Yet when reviewing, I wasn’t drawn to them with such vigor that I could stomach another $140,000 in student loan debt.

Only one position that I was excited about, sounded fun, but it earned even less than I was making now. So I had to ask myself if I would be willing to take on $140,000 debt for a lower-paying job? It wasn’t a great option even with all the extra ways to make money out there like selling photos and earning money from walking.

Do the Math on your Future Tuition

According to Investatopia, the average MBA program costs $140,000, with higher-ranking schools costing more. They’re factoring in tuition, living arrangements, books, and peripheral expenditures. That’s more than the average night-only MBA program I was looking at.

Now factor $140,000 student debt at 6.8% interest which is the average Subsidized Federal Stafford Loan according to Federal Student Aid. Having that kind of student loan debt is similar to buying a house or literally thousands of lego technic sets for my kids.

However, the common response to seeing these numbers is that you’ll be paid more after your MBA. That is perhaps true. The average salary of MBA graduates in a full-time program was $126,919. This was taken from US News when they interviewed companies mainly on the east/west coasts which usually provide a higher salary than the Mountain States and Midwest.

Conclusion

Most people like me had to make an insane decision in high school to pick a college major before entering college. So at the same time, I was focused on rehearsing for the school musical and wondering if the homecoming queen liked me (she didn’t). I was asked to choose a degree that would affect the rest of my life. I was not ready.

Going back to school for your MBA doesn’t have to be like that. There isn’t any timetable, no matter what college recruiters try to tell you about upcoming semester deadlines. You have all the time in the world to choose if an MBA is right for you.

So if you’re considering going back to school for an MBA, you should have an idea of what your future will look like. You should identify your dream job at your dream company. This is your opportunity to do WHATEVER you want in the world, and create a plan that extends after graduation.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

If you follow this blog then you know I would normally invest any extra $100 into my savings portfolio but I have a unique opportunity to disprove a popular way of making money, Lottery Tickets.

Personally, I’m not a fan of Lottery Tickets or the lesser form, Scratch-It Tickets. I go by the understandable philosophy the HOUSE ALWAYS WIN. However I can’t just say Lottery Tickets are dumb, I have to prove it.

So I bought $100 of Lottery Tickets

It’s one of the funniest feelings in the world to walk into a Gas Station (Liquor Store/Gas Station for me) and lay down a crisp $100 bill to say “I want $100 worth of Lottery Tickets!”. I assume his opinion of me was that of a Lottery Addict getting his next fix, but I started grinning like a 5-year-old buying a box of Cracker Jacks hoping to get the secret decoder ring!

He asked me “what kind?”

Crap there are more than one? Well apparently yes. There were Mega Millions, Powerball, and Scratch-Its. Each of these are considered “Lottery Tickets” and there are tons of them!

To diversified my Lottery Ticket selection and then bought all of them.

I ended up getting a wide assortment of Lottery Options. I bought $99 worth of Scratch It Tickets and one Mega Millions Ticket. I figured if I was going to win the Mega Millions, one ticket would just be as good as 100 of them if I factored odds. My thought was that I’d win more with Scratch-Its than a Powerball/Mega Millions because the odds were better.

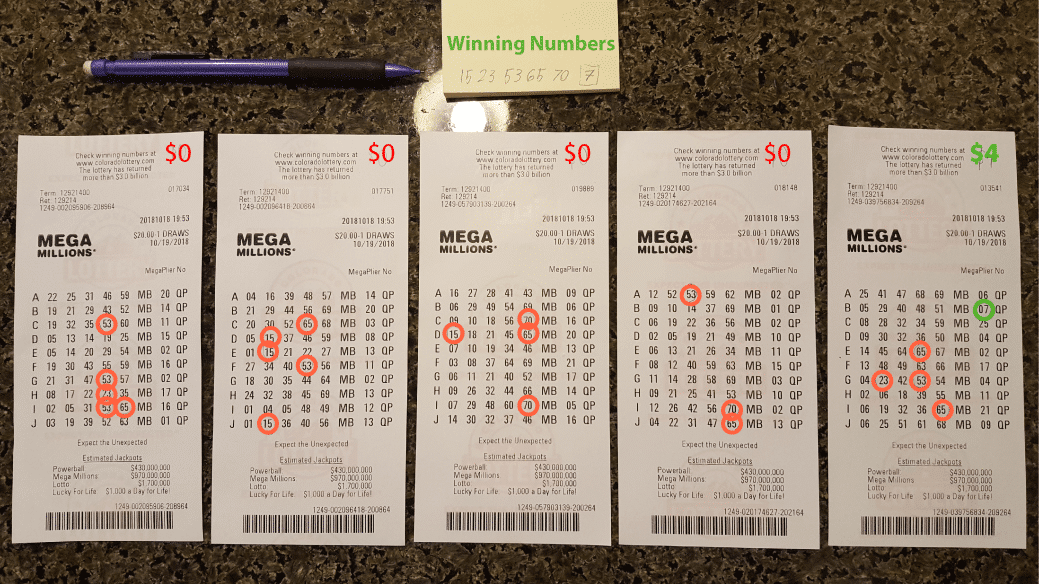

I bought (2) $20 Scratch Its, (2) $10 Scratch Its, (4) $5 Scratch Its, (5) $3 Scratch Its and (2) $2 Scratch its along with a (1) $1 Mega Millions Lottery Ticket.

Here’s what $100 worth of Lottery Tickets looks like.

Leaving the Gas Station, I felt like a kid escaping a toy store with a stash of loot. I knew the odds were against me, but damn it I thought “I COULD ACTUALLY WIN SOMETHING HERE”.

I should say that the lottery is a game of luck. There is absolutely NO skill with these games. There are people that say you can tilt the odds in your favor with different strategies. I’m sorry, I don’t believe you. The lottery is like burning your money. It’s fun to do, but you’re left with nothing in the end.

Lottery Tickets are Hella Confusing

Here’s the thing, I remember the last time I did a Scratch-It Ticket when I was 10 years old, all I had to do was scratch a ticket and it told me whether I won or not. Nowadays, there are all kinds, like Bingo and Crossword Scratch-Its that take forever and are very confusing to see whether you won or not. Even then you’re not entirely sure. After two hours of scratching tickets, I discovered I won $128. That’s freaking incredible. Yet when I turned in the tickets, I ended up actually winning $158 because one ticket had a secret 2x bonus.

WTF! These should be simple. I’ll take the extra $30 but we should really be upfront and simple about these things.

I could have easily just bought the ticket and had the gas station clerk just scan the ticket to see if I won. I discovered there really is no reason to scratch them yourself. The games are entertaining to play, but in reality, they have no purpose. Once the ticket is bought, you can scan it and learn if you win or lose without ever “playing” the game.

So I ended up winning $158

I was frankly shocked and didn’t expect to win anything. I was planning on sharing this experience to say Lottery Tickets will always lose. I’m happy I won $158 dollars but I could have just easily lost everything.

Here are the break down of the Lottery Tickets:

Lottery Ticket Winning Amounts

Ticket Amount

$20 Scratch It Ticket

$20 Scratch It Ticket

$10 Scratch It Ticket

$10 Scratch It Ticket

$5 Scratch It Ticket

$5 Scratch It Ticket

$5 Scratch It Ticket

$5 Scratch It Ticket

$3 Scratch It Ticket

$3 Scratch It Ticket

$3 Scratch It Ticket

$3 Scratch It Ticket

$3 Scratch It Ticket

$2 Scratch It Ticket

$ Scratch It Ticket

How Much I Won

Won $50

Won $25

Lost

Lost

Won $5

Lost

Lost

Lost

Won $60

Won $3

Lost

Lost

Lost

Won $10

Lost

Winnings Compared to Price

250%

125%

0%

0%

100%

0%

0%

0%

2000%

100%

0%

0%

0%

500%

0%

It appears what you win is directly proportional to the amount you spend on the ticket. That is kind of scary, you want to win big, you have to gamble big. I won most of my money from two $20 tickets. The only exception was the $3 ticket that won 2000% of it’s ticket price at $60.

What Happens if You Invest that $158

Since Wallet Squirrel is all about earning extra money and investing it, let’s see what would happen over 20 years if you invested that $158 in dividend stocks. Let’s assume 7% Market Average with a 3% dividend.

1 Year

$174.03

5 Year

$251.62

10 Year

$386.38

20 Year

$849.02

*UPDATE*

There are really two types of lottery games. There are the scratch it tickets that I did before and the Powerball/Mega Millions that people have to guess 6 numbers. I wanted to update this blog post by spending $100 on Powerball/Mega Millions tickets.

I Also Bought $100 in Mega Millions Tickets

Since this is an update to this post, I just bought these tickets from the gas station on Thursday when the Mega Millions was at 1 BILLION dollars. Of course, that’s the annuity and not the lump sum. It would be more around $337 million if it was the lump sum. Still though, a lot of money.

So I laid down another crisp $100 bill (which the cashier immediately checked if it was legit, it was) and bought my Mega Millions tickets. Since it’s $2 per ticket, I bought 50 tickets in total. I was asked if I wanted “power play” which doubles your prize if you win (except the jackpot), and I choose “no”. My goal was the 1 BILLION jackpot and “power play” always feels more like an upsell.

I expected 50 individual tickets, but the machine lets you buy $20 worth of tickets at a time, so the cashier had to select 10 random tickets at a time. I felt bad for the dude to keep pressing the buttons, but this is what 50 Mega Millions tickets look like.

After the drawing, I went through each ticket and circled all the winning numbers “15 23 53 65 70 – 7”. They say you have a 1 in 25 chance of winning, but when you select random, I’m not sure those odds are accurate. Out of 50 sets of numbers, I only won once and it was because I had the correct “power ball” number “7”. So because I had the “power ball” number I won $4. Won isn’t the correct word though because I technically lost $96 in total.

Conclusion

I will admit that Scratch-Its and Lottery Tickets are a way to earn money, but it’s very rare. You’re more likely to be pranked by a friend with a fake lottery ticket, than the odds of actually winning. Most people just continue to buy lottery tickets because of the expression “You can’t win if you don’t play”. Technically true, but the odds are astronomically stacked against you.

Scratch-It tickets seemed to be much better in this little experiment. Your odds are so little that it may not be worth it except for the fun to think about winning because you’ll likely not win. You’re WAY better off investing that $100.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Let’s start by saying that asking for a raise is a perfectly normal part of business life. It’s business 101 for managers. Yet, for employees, the idea of asking and affecting the status quo of your employee/manager relationship fills many people with anxiety-inducing paralysis.

Let’s destroy the “You vs. Them” dynamic and learn how to get your manager on your side when learning how to ask for a raise.

How to Ask for a Raise

First Things First – Prepare

If you are asking for a raise, you control when you ask. You have time on your side, so start doing your research and build your confidence.

Know Your Worth – Go through your responsibilities at work and ask can anyone else do this? Are you more uniquely qualified for essential tasks that set you apart? If they fired you tomorrow, what would it take for your employer to replace you? Take an objective look at yourself as how your employer sees you.

Create A List Of Accomplishments – Since your last raise, what have you accomplished? Did these accomplishments set you apart or go above and beyond your everyday responsibilities? Having this list of achievements could be key talking points. If your actions are helping improve the company’s productivity or increasing revenue, like starting a company blog, there should be more than a “good job.”

Use The Internet To Find Similar Salaries – Sites like Glassdoor and popular job boards regularly post salaries of similar positions in other companies. This easily accessible information can be a huge talking point in meeting with your manager. If your salary is lower than the listings your finding, your manager’s discussion should be on how to increase your salary to industry standard. Suppose your salary is higher than the industry average. In that case, you should be arguing how your responsibilities justify a higher pay or discuss title changes to put you in the next higher bracket.

When preparing for asking for a raise, try explaining what you do, your worth, and your accomplishments with a friend. If you can adequately explain what you do to a friend, you’ll be more prepared to explain it to your boss during your salary meeting sufficiently.

The Best Time To Ask For A Raise

Often people talk themselves out of something by saying it’s not the right time. However, when asking for a raise, anytime is the right time, after 12 months from your last raise.

Annual performance reviews and raises are ordinary meetings. If that’s not normal for your company, you should set up a yearly review with your manager to get feedback and create a forum for these discussions.

Particular Circumstances When To Ask For A Raise

After Completing A Big Project – If you just completed a big project, and it went well. It would help if you leveraged that win. It’s often a time to discuss bonuses or raises while spirits are high. It’s ingrained in humans to reward good behavior. Use that!

When Your Manager Is Happy – You will always get farther with happy people. However, when approaching your manager about a raise, make sure they’re happy with you and not simply happy about winning a golf tournament.

Set Up The Meeting

When you decide to ask for a raise, remember this is something you’ve been thinking about, but for your manager, it’s out-of-the-blue. If you ambush your manager, they may have a gut reaction to “NO” because it’s their job to maintain the status quo.

One of the more successful ways we’ve seen people approach their managers about asking for a raise is to start with an email to schedule a time to discuss, along with a few key arguments. An email is a controlled way to establish a future time to discuss salary, state a couple of big wins since your last raise, and most importantly, provides your manager time to mull over the idea.

Another benefit to sending an email to set up a time for a salary discussion is that you have the time to perfect the email. Take your time and make it concise. No need to send your manager a short novel on every reason you deserve a raise.

The primary goal of your email is to arrange a time to discuss your salary in person. A secondary goal is to mention your accomplishments, which you should only list 1-3 of these to keep the email concise.

Tips For Your Salary Meeting

Salary meetings don’t need to be adversarial. But rather a collaboration with you and your manager to get you to a salary you want. Here are a few tips on successful raise requests:

Don’t make it into a presentation – Your manager should already be aware of your accomplishments by working with you or highlighted them in your earlier email. It could be a simple paragraph “Hi! I wanted some time to discuss my salary as we haven’t met in over 12 months. According to Glassdoor and our competitor websites, here is the average industry salary for people in my position and responsibilities. I want to discuss how to get my salary closer to the industry average.”

Be Confident and Specific About Your Raise – Based on your research; you should have a specific number in mind to match similar positions at different companies. This number shows your manager you’ve done your research and gives them a firm number to work. Perhaps your number could be a little higher so you can negotiate down if needed.

Practice What You’re Going To Say – They say TED speakers practice 200 times before they present. For a compensation meeting, it’s more complicated because you don’t know how your manager will respond. However, you can still rehearse the main points with polish, such as “Why A Raise Now?”, “Why You Feel You Deserve A Raise?”, “How Can I Justify A Raise To My Boss?”.

If They Say No, Here’s What To Do

In the worst-case scenario, they say “no,” and that’s ok. The simple request of asking for a raise is a huge step in the right direction to increasing your salary. Here are a few tips if they say “no.”

Don’t Create An Ultimatum – Don’t force yourself into a corner by saying, “I’ll quit if you don’t give me this raise.” A manager may not have the resources in their budget to give you a raise. Then either quit to keep your word or lose credibility by staying. It’s best to ask for their reasoning and if you don’t like it, secretly start applying for other jobs.

Create A Plan For Another Raise Discussion in 6 Months – If your manager feels they can’t give you a raise right now, you should together set a hard time in the future to continue the conversation. This meeting gives you something to look forward to, knowing the conversation isn’t dead. Maintaining hard dates to continue a salary discussion keeps it top of mind for your manager. Remember, it’s always the squeaky wheel that gets cleaned.

Discuss Other Benefits That Can Make You Feel Rewarded – Perhaps there isn’t money in the budget to accommodate a raise right now. Other benefits may help you feel rewarded for your work.

Additional Vacation Time – Time off is a freedom that can be as beneficial as money. This benefit is sometimes far easier to grant employees when a raise isn’t in the budget.

Title Change – If your company can’t afford a raise, a title change may be a compromise. It’ll give you more prestige in your field and open up further salary increases down the road with a more prestigious title.

Work From Home Options – If more money isn’t an option, maybe you can work some of your hours at home. Working from home gives you additional freedom of spending time with your family and that time is priceless.

Make Asking For A Raise A Normal Thing

A raise shouldn’t be a “You Vs. Manager” ordeal. It’s a collaboration between you and your boss to give you’re the resources to feel appreciated for the job you’re doing. No manager wants to be the bad guy saying “No” to your raise, so find opportunities to work together to increase your salary to the industry standards you find on Glassdoor and adequately reflect your responsibilities.

For many people, asking for a raise is a terrifying experience, but it’s essential to know that raises are a normal part of business life. The mystery lies behind the closed doors where these discussions occur. Both you and your manager play their cards close to their chest while everyone wants to maintain the status quo. If you follow these steps, and with a bit of practice, you will master asking for raise.

There are always ways to make money outside of work, but asking for a raise is one of the easiest ways to make more money.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

In the United States, there were over 550,000 people who tested positive for COVID-19. A number that reached 180,000,000 people worldwide, according to the CDC. While symptoms varied, a common (and weird) symptom became loss of smell. Afterward, some people noticed after their smell came back, it was distorted, making some food smell and taste rancid. This phenomenon spiked thousands of Google searches for the term “Parosmia”. I was one of those who dealt with Parosmia, and while it’s nearly gone. I wanted to talk about Parosmia after COVID and how Parosmia is changing people’s food budgets.

I’ll start with I’m one of those unlucky few with jacked-up smell and tastebuds. I can no longer eat my favorite foods as they now taste like rancid trash. My go-to budget food like peanut butter and jelly sandwiches are now a pipe dream as peanut butter tastes like Styrofoam. It’s a rough life, but smells and tastebuds do come back.

When our smell first started to go south for Parosmia, we tried everything to get it back. Including home remedies on Tik Tok which included eating a burnt orange. It did nothing except taste like a burnt orange.

Parosmia Is Just Screwed Up Smell and Taste

Parosmia is common after a viral infection like colds but became more popular due to COVID-19. WebMD says perhaps up to 7% of the people who had COVID-19 developed a distorted sense of smell called “Parosmia.” People discover it about 2.5 months after the initial COVID-19 infection, and it can continue for at least six months.

What’s frustrating is how closely your sense of smell is tied to taste. When your smell and taste are off, it’s surprising how much it affects your entire life.

Imagine 30% of Food Tasting Like Garbage, That’s Parosmia

Here’s the deal. Having a screwed-up sense of smell is terrible, but Parosmia takes it to a new level. For most people, it takes the scent of specific food profiles and replaces them with the smell of rancid garbage.

Weirdly, the smell is of the same rotten garbage. Like my brain forgot what 30% of food smells like and replaced it with a generic smell of rotten garbage. For example, I’ve noticed that everything from Pizza to a McDonald’s Big Mac to a moldy wet towel has the same horrible garbage smell.

When things smell like rotten garbage, they also taste like rotten garbage. This has significantly changed my weekly grocery list!

Everyday Foods That Smell & Taste Terrible With Parosmia

Here is a list of foods that smell and therefore taste terrible, taken from my personal experience and the numerous Parosmia Facebook/Instagram Groups that have popped up since 2019.

Each person seems to have slightly different degrees of how bad foods are and what causes their rancid smells, but here are the common culprits.

Foods That Smell & Taste Terrible

Chicken

Eggs

Bacon

Onions (bye-bye Pizza & Pasta)

Garlic

Fish

Beans

Peanut Butter

Coffee

From personal experience, these foods taste terrible. Even if you force yourself to eat through the terrible rancid taste, I’ve learned your body still finds a way to reject it. I won’t go into more detail there but think bathroom.

Bacon was terrible with Parosmia. I could immediately tell while cooking, but I had to try. I can confirm the normally delicious bacon tastes awful with Parosmia. Life Sucked.

Most of this is trial and error, as the Parosmia community cannot find a common denominator for what makes certain foods smell rancid.

Even if you remove all of these items from your house, it’s still a challenge ever going out with friends.

I find myself at restaurants going through the ingredients of each dish and trying to avoid those mentioned above. A tedious process where onions and garlic make most dishes impossible to avoid. Then the process of explaining the complex nature of Parosmia to your waiter in hopes of substitution is enough to make me want to crawl under the table.

Foods That Seem To Be OK With Parosmia

I’ll start that most food will always taste a little off with Parosmia. There is no way to get around it. Simply your nose is broken so that food will feel a little off.

The best you can hope for is food tasting tolerable because asking for food to taste good again is like asking to fly.

Here is my weekly grocery list with parosmia. It’s nothing special but has become a safe haven for my deteriorated taste buds. It’s heavy on fresh fruit, ramen noodles, and protein shakes.

When we first got parosmia, we did a lot of charcuterie boards. We incorporated lots of fresh fruit and experimented with different combinations to see what worked for our smell and taste buds.

Here is my Parosmia grocery list for my family:

Bread

Milk

Apples

Strawberries

Grapes

Cuties

Diced Tomatoes

Mozzarella Cheese

Potatoes

Eggs

Mac & Cheese

Ground Beef

Cereal

Protein Shakes

Ramen Noodles

These have seemed pretty safe for my family, but I’ll add that anything sugary like cereal is also OK. It appears that sugary foods mask any rancid taste.

I know most people will balk at the surgery cereal, but it pretty much saved me when my smell and taste first started to skew. It was the only thing I could eat without gagging. I used sugary cereal as a base and started to branch out and experiment with other foods from there. However, as you may expect, the sugary cereal was KILLER on my diet, and my workouts had to compensate heavily, which was great for walking with Stepbet. So learn from my mistakes for your grocery list.

I’ve added a protein shake to most of my meals to get my daily protein since I can’t eat chicken like I used to.

Bland Food Is Your Friend, But So Is Spice

At first, I only ate bland food with simple ingredients. I figured I could swap out ingredients to find which foods caused the worst reactions. Learning from trial and error became second nature during Parosmia.

HOWEVER, as you may expect, my family had a short tolerance for bland food. It was safe, but the monotony was draining our morale. So we discovered an unexpected craving, spice.

Let me preface, myself and my family is NOT a fan of spicy food. We were total wimps when it came to any heat levels. Yet, spice became a welcome addition to all our meals that breathed new life into our meals. We used bottles of spices like red chili pepper for the first time since we bought a spice rack. It was an incredible discovery!

Our Favorite Meal During Parosmia

In addition to buying Ramen noodles in bulk for their bland, safe flavor, we practiced with different recipes at night to find new flavors that friendly to our pallets. Here is one of my family’s favorite recipes.

Homemade Pizzas – Take Nann Bread as your crust. We usually top with store-bought pasta sauce, but it’s packed with onions and garlic. So we create a homemade sauce with a can of diced tomatoes and blend them into a sauce with red pepper flakes. The heat helps with the bland flavor. Then add fresh mozzarella and oven-bake for 12 minutes. It’s great!

BONUS Tiramisu Crepes – I honestly don’t know the recipe because my girlfriend did them as a surprise and they were amazing. However, if you message us on Twitter I’ll see what I can do.

My girlfriend made these amazing tiramisu crepes. The sugary treat was perfect for parosmia but perhaps a little unhealthy. However, it tasted wonderful, and that’s a rare luxury for when everything else tastes terrible.

Expect Your Food Budget To Increase

One of the most significant ways my food budget has increased is that meal prep has become significantly more complicated.

It seems that anytime I reheat meals in a microwave or oven, the reheating causes food to have more pungent rancid tastes. So we no longer do many leftovers. Most of our meals are cooked the night off.

Also, purchasing all the ingredients from scratch makes food taste a little fresher but comes at a premium price. It’s not terrible, but something to be aware of. Luckily we have a couple of different income streams that make this easier.

Parosmia Makes Eating Healthy Difficult, but Not Impossible

Admittedly Parosmia initially caused me to gain significant weight because the foods I’m used to eating, Pizza, Pasta, Chicken, became intolerable.

I clung to the sugary foods that provide some sense of flavor. Eventually, as I learned more, I introduced more fresh fruit and learned to cook meals from scratch to control all the ingredients.

So I turned a horrible Parosmia experience into a learning experience teaching new skills and introducing more fresh ingredients into my diet.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Three weeks ago, a friend asked “What happens to debt when you die”. Now, this wasn’t a morbid question, I’ve simply just become the personal finance guy in my little group of friends, and they wanted to know what happens. The incorrect answer is “You’ll be dead, why do care?”.

What essentially happens when you die is “Probate”. It’s the process of paying off outstanding debts and distributing your wealth to your beneficiaries with your “estate”.

What’s in my Estate?

Your estate is essentially your net worth. This is made up of your home value, bank accounts, car, boat, RV and all your smaller assets as well such as paintings, flat screen tvs, etc. Essentially everything you have to your name, including your name. (source)

Your estate is everything you have, to pay off your debts first then distribute to your heirs as dictated in your Will. However some people don’t have enough money to pay off all their debt first, so I’m going to focus on what happens to your debt when you die that you can’t pay off.

Credit Card Debt – What If I Can’t Pay This When I Die?

Millions of Americans have credit card debt, so I was curious about this first. If you’re the only name on the card, the debt stops with you. So if you don’t have enough assets (money) to pay off your credit card debt. Then the Credit Card company simply has to take the loss and move on and your heirs aren’t responsible for paying it off. (source)

They can though, go after a “co-signer” on your credit card. So always be careful of co-signing anything. However, if you’re just authorized to use the credit card, you’re not liable to pay off the debt because you’re not the actual owner of the credit card and don’t carry the financial liability.

Student Loan Debt – What If I Can’t Pay This When I Die?

If your estate can’t cover your student loan debt, then that’s where the buck stops. Unless you had a co-signer on the account, no one else including your heirs, are responsible for that debt.

It was interesting to hear though that according to Nerd Wallet, collection agencies may still legally contact your family members to “discuss” student loan debt, but they can’t mislead your heirs into thinking that they’re responsible for your student loan debt (source). Not sure why they would do this unless they were trying to guilt your poor grandma into paying off your student loans for moral reasons. Those bastards. Be sure to send them a letter asking them to stop and request a read receipt.

Car Loan Debt – What If I Can’t Pay This When I Die?

This was interesting. If your estate can’t pay off your car loan debt then they can repossess your car. This makes sense, it’s a tangible asset that can be taken back if not fully paid off. How I paid off my car.) However whoever inherits the vehicle can just continue making payments on their inherited Ford Fiesta and the bank is unlikely to take any action as long as they continue to receive money. Remember it’s all just business. (source)

Home Loan Debt – What If I Can’t Pay This When I Die?

This is really the least of my concerns since I rent a studio loft downtown, but for some friends who recently bought a house, let’s chat. Due to the 1982 federal law, the surviving spouse may continue to make payments to the mortgage without having an issue (source). They can simply continue to make payments similar to how the recently deceased did or sell and keep the difference in monetary value.

Things get a little murky with mortgages with a “home equity line of credit”. These are usually paid off during the probate process but may involve selling the house if your assets don’t cover the debt. If you’re worried about this, I highly recommend you consult a local attorney.

Is anything safe from debt collectors?

In my research, I’ve found a few things that appear to be safe from debt collectors. These are IRAs, 401(k)s, brokerage accounts, life insurance and pension plans that don’t go to probate, so they won’t be considered a part of your estate to pay off debt collectors. So your heirs may be left with something. (source)

Sometimes people get life insurance to help their loved ones (often co-signers) with the debt they leave behind. Since life insurance is exempt from some estates, it can be used by your heirs and loved ones with the burden of any debt you accumulated together.

Conclusion

In short, your debt belongs only to you, it is not passed on to your family when you pass. (source). As long as you didn’t have any co-signers for your Student Loans/Credit Card Loans and your estate can’t pay them, those debts die with you. Home Loans and Car Loans are tangible assets that can be taken back if not paid off or have someone take over the payments in order to keep them.

If this research taught me anything, it’s to be very aware of what I co-sign. Debt dies with the deceased, unless there’s a co-signer.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Warren Buffett, CEO of Berkshire Hathaway, has a net worth of over $78.2 billion and is known as one of the greatest investors of all time. So when he speaks, people take note.

Here are some of the top 22 Warren Buffett Quotes the internet can’t get enough of.

Top 22 Warren Buffett Quotes The Internet Can’t Get Enough Of

Here are some of the top Warren Buffet quotes found on every list of Warren Buffet quotes around the internet. These quotes range in wisdom on investing to regular life. I try to live by these quotes on my own investment portfolio.

Warren Buffett Quotes

1. Rule #1: Never lose money. Rule #2: Never forget rule #1

One of my favorite Warren Buffet Quotes. The fastest way to grow your money is to never lose it in the first place. This applies from saving on your groceries to focusing on less risky stocks of well established companies.

2. It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you’ll do things differently

Think about the Wells Fargo or Equifax scandals. It takes years to build enough trust for someone to have brand loyalty. Warren Buffet quotes it takes 20 years, but it takes 5 minutes or less to destroy all that goodwill you’ve built. People are quick to revolt if you’ve done anything to betray their trust.

It is infinitely harder to build trust than destroy it.

3. Diversification is a protection against ignorance. It makes very little sense for those who know what they’re doing.

Multiple studies show that diversification in the stock market will help protect you against market falls. Or it could be summarized in the old proverb “Don’t put all your eggs in one basket”. Unless you have insider information that a stock is going do really well, maintain a diversified portfolio to protect you. No one knows what they’re doing all the time.

4. If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes. Put together a portfolio of companies whose aggregate earnings march upward over the years, and so also will the portfolio’s market value.

Unless you’re a day trader (I will never be), you should only be investing in the stock market with the intention to hold those stocks for a long time. You can do really well as a beginner if you’re buying stocks and not planning on selling till you retire. Those are where you get the best returns. Warren Buffett is infamously known for rarely selling stocks.

5. It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

When you buy a stock, you should think of it as owning a piece of that company. You should be looking at wonderful companies that have a competitive advantage in the industry. Those are the companies that will do well over the long run. You may find a wonderful price on a mediocre company, but really what are you getting? A mediocre company that will likely be edged out of the market by a better company.

Many of the famous Warren Buffett quotes are about investing in strong companies with a competitive advantage and strong brand loyalty rather than cheap companies where you think you can make a quick buck. Warren Buffett is never into buying a company for a quick buck.

6. Be fearful when others are greedy. Be greedy when others are fearful.

During the 2008 financial crisis when investors were all exiting the market, Warren Buffett invested in a few large companies even though their stock prices were falling. Those deals made Warren Buffett over $10 billion dollars when the market stabilized and it’s continuing to show dividends. When the market goes upside down during world events, politics, market forecasts, those are the times when everyone else is fearful, that Warren Buffet sees an advantage when the markets crash.

Think about it this way, the New York Stock Exchange has been around since 1817, it has always recovered. Chances are, minus a world apocalypse, that the market will always bounce back. Those who capitalize on those downturns are usually rewarded.

7. The difference between successful people and really successful people is that really successful people say no to almost everything.

One of my favorite Warren Buffett quotes because it has so many applications. You will see many opportunities in your life and you may want to jump on everyone, but it’s ok to be selective and say no. You’ll burn yourself out if you say “yes” to everything. This also applies to going out on a Saturday night with friends drinking. It’s ok to say “no” to save a few dollars or have a night to yourself to finish your article on Warren Buffett quotes. =)

This also applies to going out on a Saturday night with friends drinking. It’s ok to say “no” to save a few dollars or have a night to yourself to finish your article on Warren Buffett quotes. =)

8. Develop and build the habits you admire in others.

Remember all those times that your parents wanted you to hang out with those “good kids”. The habits of the people you surround yourself with rub off you on, consciously or unconsciously. When you find people like Warren Buffett, the Oracle of Omaha, who is one of the greatest investors of all time. You should find out what makes him so successful and learn those traits to improve yourself.

9. Passive investing will make you more money than active trading

Oh my goodness, fees are the WORST! Active trading requires more work and more fees, so more of your money will be paid to your broker. Yet studies have shown over and over that passive investing where you set your money and forget it are far more successful for growing wealth. I don’t plan to ever touch my stocks currently making dividends.

10. There seems to be some perverse human characteristic that likes to make easy things difficult.

Great quote, people always imagine things are more difficult than they really are. When I first considered starting investing, I thought there were so many hurdles and financial experts I would have to pay. Yet, when I finally decided I wanted to start investing in the stock market, I just downloaded the Robinhood App and started investing. It took 10 minutes to sign up and buy my first stock when I worried about investing in the stock market for over 5 years. Things are often more simple than you think they are.

11. Tell me who your heroes are and I’ll tell you who you’ll turn out to be.

This is similar to the Warren Buffett quote “Develop and build the habits you admire in others”. If you want to be an entrepreneur, start joining local meetups of entrepreneurs. You learn SO MUCH MORE when you surround yourself with the people you want to be like. You can learn A LOT in a book, but you’ll learn even more by surrounding yourself with people you admire.

12. We have long felt that the only value of stock forecasters is to make fortune-tellers look good.

No one can predict the stock market, no one. Not even Warren Buffett. Anyone who says they know exactly how the market works is trying to sell you something. You can lump stock forecasters being as accurate as the carnival fortune-tellers. You know the ones with 3 teeth, crystal ball and you’re going to die in 2083.

13. When we own portions of outstanding businesses with outstanding managements, our favorite holding period is forever.

If you invest in an outstanding company, even if the stock price goes up, why would you ever sell it? No matter when you sell it, outstanding companies will continually do better and better. Don’t sell until you absolutely have to, otherwise, you’ll just be losing money in the long run. Many of Warren Buffett Quotes are like this, they are all very Anti-Day Trader.

14. You don’t need to be a rocket scientist. Investing is not a game where the guy with the 160 IQ beats the guy with 130 IQ.

If you follow the basic principals of Warren Buffett and buy outstanding companies with strong competitive advantages like Apple (AAPL). You don’t have to be a genius. Just buy and hold forever, you literally don’t have to do anything until you sell.

Many Warren Buffett quotes are similar to this because he stresses that anyone can invest in the stock market. The simplest way is just to invest in index funds that follow the market. Set it and forget it. The market sees an average increase of 7% per year and that’s WAY better than a savings account.

15. I try to buy stock in businesses that are so wonderful that an idiot can run them. Because sooner or later, one will.

Look for companies to invest in that are so strong that they can weather any storm because soon enough they will have to. Think about Apple (AAPL), as long as they keep pushing out iPhones it doesn’t matter who runs the company, they’ll continue to do well. People were worried when Steve Jobs passed because they didn’t know the future of the company, but Tim Cook stepped in and maintained the same Apple legacy. As long as Tim Cook sticks to the secret Apple recipe, they’ll be in good shape.

16. Buy into a company because you want to own it, not because you want the stock to go up.

If you see a company that you think is going to do well or heard will do well, don’t buy it unless you’re willing to hold it for awhile. If something goes wrong and the stock dives, you’re stuck with a company you don’t believe in and will likely sell at a lower price to get rid of it, ruining the reason you bought it in the first place.

17. Wall Street is the only place that people ride to work in a Rolls Royce to get advice from those who take the subway.

This is just a funny Warren Buffet quote.

18. Charlie and I have not learned how to solve difficult business problems. What we have learned is to avoid them.

I’m sure Warren Buffett and Charlie Munger have learned how to solve difficult business problems, but the best way to navigate murky waters is to avoid them all together. The more problems your business can avoid, the better shape you’ll be. You can avoid a lot of problems from being proactive instead of reactive.

19. Long ago, Ben Graham taught me that “Price is what you pay; value is what you get.”

Ben Graham, Warren Buffett’s mentor had this popular quote. I always think about it simply. Price is what you buy a stock for and Value is what you sell that same stock for.

20. It’s better to hang out with people better than you. Pick out associates whose behavior is better than yours and you’ll drift in that direction.

If you can’t tell, Warren Buffett believes in surrounding yourself with the right people. He credits much of his success from surrounding himself with smart, good people.

21. If past history was all there was to the game, the richest people would be librarians.

When you analyze a stock based on its historical performance, it’s called technical analysis. Yet past performance does not necessarily mean future performance. Just because you know what the stock has done in the past doesn’t mean it’s going to follow that same trend.

22. You only have to do a very few things right in your life so long as you don’t do too many things wrong.

It’s ok to mess up, focus on learning from those mistakes for the next time. It just sounds cooler when Warren Buffett quotes it. Or you can take this as no matter how many mistakes you’ve made in the past, you always have a chance to do more good. It’s one of those life quotes that can go many ways.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

That means the average person spends $54.63 eating out a week or $218.52 a month on just eating out. Unless you have a side-hustle that makes you lots of money. The obvious answer is to eat in!

What About Eating In?

Most people think they can easily quit dining out, and start cooking delicious meals. Here’s the thing with cooking for yourself, the movies get it wrong.

It’s not always a romantic and soothing experience.

Often times it’s a “Crap, I need to eat. What should I cook?” experience that you pray to the food gods you have the right ingredients in your fridge and clean dishes.

Let’s face it, we are busy in our lives and don’t have the time to visit the store every day buying fresh ingredients for a new recipe we found on the internet.

In fact, according to the Harvard Business Review, researcher Eddie Yoon over two decades collected data as consultants for consumer packaged goods companies. He found that:

15% of people say they LOVE to cook

50% of people say they HATE to cook

35% of people say they are ambivalent about cooking (mixed feelings)

If you’re one of the people that hate cooking, you should create a meal plan to make it as easy as possible.

Plan a week in advance what you’re going to eat for each meal and know how to cook it. This way you’ll have the ingredients and can plan accordingly for time.

However, not all plans work out.

Introduce The Peanut Butter and Jelly Theory

When meal plans fail, let me introduce Peanut Butter and Jelly sandwiches, otherwise known as a PBJ.

Let me first admit that I have an addiction to commenting on Finance forums, Facebook Groups, and Blogs. The mechanics of building wealth are simple and I’m always happy to remind people that things are often more simple than they appear. Like how I responded to this comment and created “The Peanut Butter and Jelly Theory”.

I get it, you want to start saving money on food and you’re looking for suggestions from the personal finance community to help.

Answers ranged from getting a crockpot to make meals simple, cooking large meals on Sunday and eating leftovers throughout the week, to buying frozen meals that may not be great for you, but easy to prepare.

All of the responses skirted around the idea that a solid weekly meal plan is the best option to help you save money on food. However, sometimes these meals don’t work out for a number of reasons, and once you fall off the wagon, you can end up at the local McDonalds.

So I introduced the Peanut Butter and Jelly Theory. The cost-effective, quickest meal ever to keep your budget on track.

This is easily the most actionable thing you can do to start immediately saving on your food budget. In many cases when people eat out, it’s due to convenience because they don’t have anything at home to sound appealing. That’s when the Peanut Butter and Jelly Theory comes in handy.

“Stash emergency PBJ&J supplies in your kitchen. When hungry, but have nothing else. You can have a PBJ. If you’re not hungry for a PB&J, wait 2 hours until you’re hungry enough to eat a PB&J.”

Sometimes a PBJ isn’t exactly what you’re craving and your favorite restaurant sounds better, or your family would not be happy about that. Well suck it up, you’ll soon be out of debt and you can buy your family a jet ski. Everyone loves a jet ski.

Try the Peanut Butter and Jelly Theory

If you want to save THOUSANDS on food budgets, you should try the Peanut Butter and Jelly Theory! Meals cost less than $1 to make, you’ll save time and money. Most importantly, you’ll have a secret stash of PBJs to make and everyone is a stack of cash saved from eating out!

You’re welcome.

Disclaimer: Wallet Squirrel did not invent the Peanut Butter and Jelly sandwich, just an advocate of saving money. Wallet Squirrel was not sponsored by big PBJ corporations to promote their superior and delicious product.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Let me preface that I used to be a waiter so I understand the value of tipping, but as a customer, tipping is the worst! It’s psychological warfare at the end of every meal that results in either anxiety that you haven’t paid enough or havoc on your wallet for paying too much.

Then exactly how much too much and too little for a tip? Common restaurant adequate says a tip should be 15%-20% pretax, but then why does every restaurant leave the anxiety for the customer to decide how much to tip?

Let’s face it, an extra 20% of a $60 check is still a lot on your budget. That’s $12 the menu doesn’t mention.

This History of Tipping is Murky

From what I found in the Business Insider and Washington Post (and it’s a murky origin story) tipping originated around 17th century England where the word T.I.P. meant “To Insure Promptitude”. The upper class provided extra “allowance” to servers (lower class) to be given faster service.

This practice made its way to America after the Civil War when wealthy Americans started traveling back and forth to Europe. So we can blame them, and I do.

Tipping Today Just Allows Restaurants to Pay it’s Servers Poorly

Because servers receive tips, the federal tipped minimum wage for tipped workers is as little as $2.13 an hour because they receive tips to supplement the difference (source).

That’s kind of ridiculous, right! Restaurants are allowed to only pay their servers $2.13 an hour and expect servers to get the rest of their income from tips. So when you pay your bill, you’re essentially paying for the food/environment with your bill and your tip pays the waiter’s salary.

If you’re a waiter, the customer is actually your boss since they’re the ones that pay you. So every day, every hour, you have a different boss. Yikes.

How Much Do You Pay Your Server Then?

According to Google, yes I googled “How Much Should I Tip”. You should be paying your server 15%-20% of your pre-tax bill.

This Is Where The Anxiety Starts

Which one is it? Do I tip 15% or 20%?

What If The Server Was Bad?

If my bill is $100, does the server get an extra $20 just because they took my order and walked food back from the kitchen?

What if they were awful? We’ve all had bad servers who ignored us. They took a long time or brought us the wrong items with a rude attitude. Is that when you tip them 15% instead of 20%?

What about if the food was awesome but the service was terrible? ugh

Should I feel both angry at my server for bad service but feel guilty since they’re paid so poorly? How should I feel?

I recall a study conducted found that bad servers still received 15%-20% regardless of how good the service was because people felt it was the socially acceptable thing to do. No one wants to be a bad tipper, but should I tip poorly to save a bit of money and prove a point to the server? Would a bad tip even make a difference?

What if the server was awesome?

You plan to spend a certain amount of money eating out and even account for a 20% tip. Do you exceed your budget further if your server was fantastic? Should your server’s awesomeness impact your planned budget? Should they be worthy of more than a 20% tip of that you’re still paying off student loans?

Damn it Janet, you were so great that now my tip for you exceeds my monthly food budget.

Are you a bad person if you don’t acknowledge their above and beyond service or will they quit trying harder if people don’t tip more for the great service?

What About Tipping During Group Meals?

Now imagine eating out with a group of friends, each pays their own bills and it always ends with everyone deciding the tip for themselves. All while each of you judges each other’s tips. If you only tipped 15%, does that make you a jerk if everyone else tipped 20% – 25%?

On the other hand, are you a jerk for tipping more than everyone? Are you considered flaunting your money because you can spend more money than everyone else or does it make you more generous or charitable?

This Is Why I Hate Tipping!

Why does a nice meal out with friends have to end with awkward silences while everyone calculates percentages in their heads while they secretly judge the performance of the server? Ending in silent comparison of who tipped more, who was more generous, and who felt more charitable than the rest of the group.

I Now Tip 20% Regardless of Service

Tipping makes me so anxious that I’m just starting to tip 20% regardless of service (paying with my credit card). The server can refill my drink at the perfect time or pour hot soup on my head. Creating a baseline 20% tip in every situation saves me from unnecessary anxiety at the cost of a few extra dollars from my budget. Sorry budget.

Except Subway “Sandwich Artists”, I still don’t understand why they now have a tip jar. They literally walk along with me placing ingredients I select onto bread. Is tipping at fast food restaurants now becoming a thing?

If you also tip 20% regularly, here is a chart to help you decide what 20% would be when you’re looking over a menu because they don’t list the extra tipping cost on the menu.

20% Tip Per Cost of your meal

Check

20% Tip

$20

$4

$40

$8

$50

$10

$60

$12

$70

$14

$80

$16

$90

$18

$100

$20

If this seems like a lot of money to tip, you can always stay in and eat a Peanut Butter and Jelly sandwich. Save eating out when you know you can spend extra money on a 20% tip.

What do you tip your servers? There is obviously no right answer otherwise they wouldn’t leave the tip field on every check blank. I REALLY want to know. Do you judge your waiter every service or, like me, give them a flat fee regardless?

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

I’ve always had a hard time finding a good list of Amazon Affiliate Website Examples, so here is my personal list of inspiration that I’ve built up over the years. I’ve been itching to create a new website lately as an awesome way to make money, but before I start I thought I would review my list of successful Amazon Affiliate Websites currently making money for some lessons learned.

What is an Amazon Affiliate Website?

An Amazon Affiliate Website is any website that earns money by linking products from their website to the Amazon store. This can be a blog or website that references a product with a link back to Amazon, so customers can purchase that particular item.

The idea is that you are referring customers to Amazon where you gain a commission if a user buys from the Amazon store. This is usually 5%-10% per purchase. Amazon tracks this by a special code from the URL link on your website. Click here to create your own website with affiliate marketing.

Many of these websites use Amazon, along with other affiliate programs to boost revenue. Here is a list of 108 Best Affiliate Programs in addition to Amazon to make money for bloggers and influencers.

22 Successful Amazon Affiliate Website Examples

ThisIsWhyImBroke – Amazon Affiliate Website Example

ThisIsWhyImBroke.com

This is one of my favorite Amazon Affiliate Websites because it’s so freaking cool! These guys gather up the coolest gadgets, gifts, tech and oddities from Amazon and around the web to showcase on their website. These are gag gifts and fun gadgets people love to buy. They likely use an SEO tool like SEMrush to find great blog post ideas. This site uncovers the cool, often hidden, things of the internet and all you have to do is click on one of the Amazon Affiliate links to buy it from the Amazon store. ThisIsWhyIAmBroke works with more than just Amazon, but it’s one of their biggest revenue sources. It’s entirely possible to create a website just like this.

Monthly Visitors (SimilarWeb) : 2.40M Visitors Average Post Length: 10 – 160 Words One of Most Searched Products: Salt Firing Shotgun How much do they make: Around $20,000+ per month from Amazon (source)

How To Start A $5K Blog Free Email Course

A free step by step course with Andrew Kraemer looking at examples of blogs making over $5k, how to set up your own blog and what you need to do to get more traffic.

Join us to get wonderful blogging tips and access to this amazing course!

I will guard your email with my life. Check your inbox. =)

ConsumerSearch – Amazon Affiliate Website Example

ConsumerSearch.com

This website started in 2000 as a review website which helped consumers by reviewing different products and offering the consumer the chance to purchase the product. These have become a very popular way for bloggers to create Amazon affiliate websites. It’s a great way to feature products and a good review can be very motivating for someone to purchase.

Monthly Visitors (SimilarWeb) : 1.10M Visitors Average Post Length: 1,000 Words One of Most Searched Products: Bose Sound Bar How much do they make: This site was bought for $33 Million from About.com in 2007 (source)

GiftIdeaGeek.com

This Amazon Affiliate Website is similar to ThisIsWhyImBroke in that the main homepage is set up as an affiliate product page which is perfect selling. The idea is that GiftIdeaGeek focuses on geeky and pop culture referenced products that appeal to that niche. This website uses witty satire to hook the audience into “clicking through” on creative products and if they buy, GiftIdeaGeek gains the affiliate commission. In addition to the homepage, they use a blogroll section to gain SEO and additional affiliate opportunities.

Monthly Visitors (SimilarWeb): Unknown Average Post Length: 1,000 Words One of Most Searched Products: Clever Socks How much do they make: Unknown

TheWirecutter – Amazon Affiliate Website Example

TheWirecutter.com

This is a great example of a top-notch review site. They start at the homepage notifying that they make affiliate commissions but provide top-end reviews from independent reviewers. This is great, to be honest upfront. In addition to being transparent, they also take the content is king strategy. I randomly clicked on their “Top Home Projector” post where they reviewed (and linked) to several high-end home theater projectors. Keep in mind that these high priced items produce high commissions. That may explain why they spent the time to write a 5,000 word post on it. This site seems to do everything right in being a prime example of an Amazon Affiliate Website. This site now has over 60 staff members working for it.

Monthly Visitors (SimilarWeb) : 8.10M Visitors Average Post Length: 3,000-5,000 Words One of Most Searched Products: Air Purifier How much do they make: In 2015, this site combined with The Wirecutter made $150 Million in eCommerce sales. So you can get an idea of their commission revenue. (source)

TheSweetHome – Amazon Affiliate Website Example

TheSweetHome.com

This is the sister site to the affiliate marketing site TheWirecutter. Another amazon affiliate website that lists gadgets and gear that the website reviews. They come out and say it on their homepage, they earn money by affiliate commissions. Apparently, this site receives over 1.8M visitors, which is pretty impressive considering this site only started in 2013. I guess the moral of the story is, it’s not too late to start a review website. It also helps to have incredibly long reviews. In fact, their one soda stream review had over 13,000 words. This is a great example that content is king.

Monthly Visitors (SimilarWeb) : 2.50M Visitors Average Post Length: 4,000 – 5,000 Words One of Most Searched Products: Robot Vaccum How much do they make: In 2015, this site combined with The Wirecutter made $150 Million in e-commerce sales. So you can get an idea of their commission revenue. (source)

GearPatrol – Amazon Affiliate Website Example

GearPatrol.com

This is an interesting style review website that reads more like a magazine than a review site. This definitely helps give it some more credit than throwing a up a bunch of products and hoping people read them. It’s interesting that it takes a different approach, rather than writing long content, it focuses on a clean layout and video reviews to show people the product they’re testing, racking in 2.3 million monthly viewers. This is incredibly valuable for people willing to buy, but want to see the product in a video demo before purchasing. Now compare this site to what the site looked like in 2008 (here).

Monthly Visitors (SimilarWeb) : 3.30M Visitors Average Post Length: 100-500 Words One of Most Searched Products: Alera Elusion Series Office Chair How much do they make: I don’t know how much they make

DogFoodAdvisor – Amazon Affiliate Website Example

DogFoodAdvisor.com

This is a testament that design isn’t everything. Look at their homepage. There is one, very cute puppy, but nothing else. I’m not sure how this site is successful, but from looking over their latest articles, they are receiving regular viewers and comments. Something is working. Then again, people do love their dogs.

Monthly Visitors (SimilarWeb) : 1.30M Visitors Average Post Length: 1,000-1,500 Words One of Most Searched Products: Dog Food How much do they make: I don’t know how much they make

BabyGearLab – Amazon Affiliate Website Example

BabyGearLab.com

So combine a review site and something people everyone loves, like babies. Imagine all the confusion new parents have when they bring a new baby into the world. What do they do, what do they need, what is the best? BabyGearLab solves that by reviewing baby stuff and helping parents understand it and buy it. This site has been around since 2011 helping parents through the impossible decisions of what is best for your baby.

Monthly Visitors (SimilarWeb) : 234.10K Visitors Average Post Length: 6,000-10,000 Words One of Most Searched Products: Convertable Baby Seat How much do they make: I don’t know how much they make

BestCovery – Amazon Affiliate Website Example

BestCovery.com

Review sites continue to be an impressive way to make an affiliate commission. This review site doesn’t even niche down, their tag line is “Discover the Best of Everything”. From my initial review, they continue the streak of long content to rank high in Google. In doing this, they list multiple items really pushing their 1st, 2nd, 3rd and so on picks. All conveniently with their own price tags linking to Amazon. With only 152 thousand monthly visitors, it’s not as much as other sites, but they continue to push out new content and gain new Facebook users. Anyone with a blog knows, it’s hard to get Facebook users, so they’re doing something right.

Monthly Visitors (SimilarWeb) : 152.10K Visitors Average Post Length: 4,000-6,000 Words One of Most Searched Products: Best Epoxy How much do they make: I don’t know how much they make.

BestReviews – Amazon Affiliate Website Example

BestReviews.com

This is one the cleanest designs I’ve seen of an Amazon Affiliate Website. It has a very professional look for a review website, but they don’t overcrowd you with product reviews right off. This site really sets itself apart with their actual videos and reviews inside of their test center. You know these testers are actually testing the product rather than copying a review from another site or making things up. It’s so legit that I will likely be back to this site for future reviews for my purchases. It really gains your trust with the photos and videos even though you know they are making money through the affiliate commissions. Plus they buy all the products themselves and never accept any products from the manufacturer to maintain objectivity, but when you bring in 3.1 million visitors per month, you can buy a few items to review.

It’s so legit that I will likely be back to this site for future reviews for my purchases. It really gains your trust with the photos and videos even though you know they are making money through the affiliate commissions. Plus they buy all the products themselves and never accept any products from the manufacturer to maintain objectivity, but when you bring in 3.1 million visitors per month, you can buy a few items to review.

Monthly Visitors (SimilarWeb) : 3.80M Visitors Average Post Length: Around 1,000 Words + Videos One of Most Searched Products:Best Hair Bleaching Products How much do they make: I don’t know how much they make.

KidsTabletswithWiFi – Amazon Affiliate Website Example

KidsTabletsWithWiFi.com

This is an Amazon Affiliate Website that has really niched down into specifically, as the name implies, kids tablets with Wifi. These are high priced items that produce high commissions in a huge market, children. What is the best tablet for kids? Do you give them an iPad? What if it breaks? Is there a cheaper option? These are all questions that this site helps with. It runs like a blog, but with a relatively simple design. It’s hard to tell if they have produced much new content because they don’t include dates with their blog posts. However, this site is just one blog, with three additional pages for “Best Tablets for Kids”, “Kids Tablet Reviews” and “Kids Tablet Comparisons” all of which are likely keyword researched names. It’s likely the niched down keyword research to bring in the traffic, because the content while good, is relatively short with 300-500 words per post.

Monthly Visitors (SimilarWeb): 1.80K Visitors Average Post Length: 400 – 600 Words One of Most Searched Products: Fire HD Kids Tablet How much do they make: I don’t know how much they make.

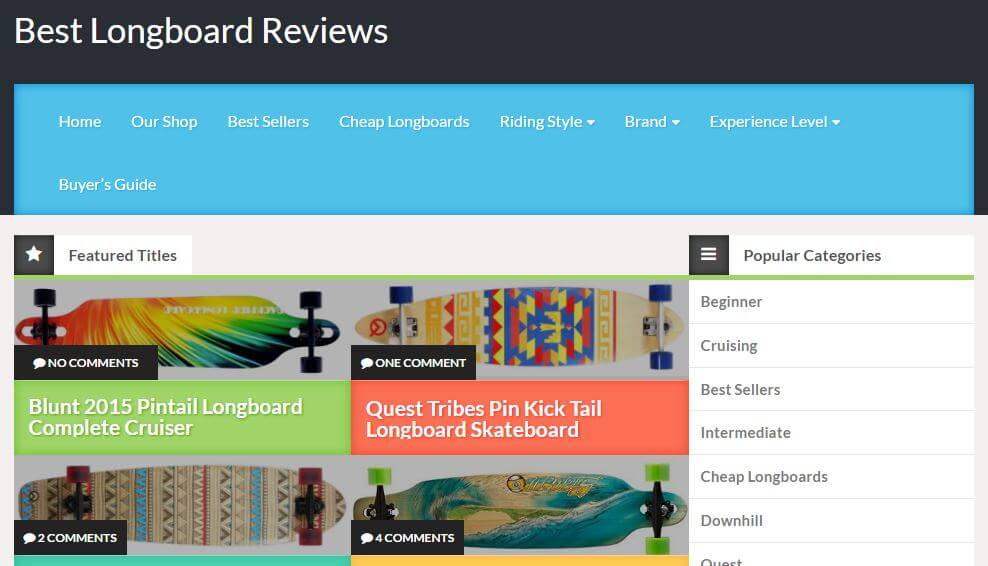

LongBoardReviews – Amazon Affiliate Website Example

LongboardReviews.net

Another example of an Amazon Affiliate Website that niched down to long boards. These are like skateboards but longer and meant to cruise, going longer distances than skateboards. It’s a relatively simple website that loads the user with tons of products from the homepage but highlights the lack of comments per review (usually 0 – 2 comments). The typical length of an article is 300-500 words so they are relying on their specific niche for traffic. Not bad for a “.net” domain as they are less common than their popular counterparts “.com”. It’s not the best example, but I’m going for a range.

Monthly Visitors (SimilarWeb) : 2.70K Visitors Average Post Length: 400 – 600 Words How much do they make: The website sold in 2016 on Flippa for $5,275. Usually a website sells for a year’s worth of revenue. So we can expect this site to make around $500 per month (source)

FootballSnackHelmets – Amazon Affiliate Website Example

FootballSnackHelmets.com

This is one of the most niche markets I’ve ever seen. It’s gems like these that make me confident the right keyword research in the smallest of niches can lead to a successful Amazon Affiliate Website. I’m not saying this specific site is successful though. They have only 2 blog post with minimal content for each “Football Snack Helmet”. It seems like someone had great intentions to set up an affiliate site with a clean design but forgot about it after 2 blog posts, ending in June 2016. This is one of the easiest examples that you could set up in a weekend.

Monthly Visitors (SimilarWeb) : 2.20K Visitors Average Post Length: 100 – 300 Words One of Most Searched Products: Cleavland Browns Kids Uniform How much do they make: I don’t know how much they make, but we anticipate it’s seasonal and reliant on the US customer base.

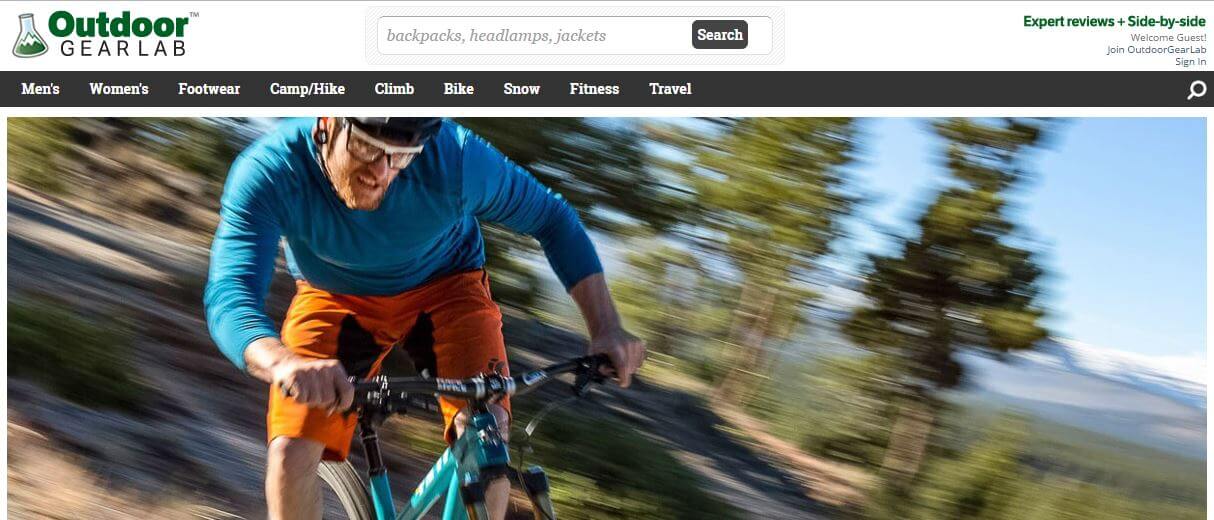

OutdoorGearLab – Amazon Affiliate Website Example

OutdoorGearLab.com

This site is owned by the same owners as BabyGearLab.com so you’ll notice some similarities. It’s a really clean site that looks more like REI’s website than a review site. They generate tons of organic traffic for each review category like ski gloves combines all of their test products (amazon links), test experiences, reviews and opinions so that the review pages reach around 6,000 words. This is a great way to do a review page in my opinion to combine the word length of each review into one huge, helpful page. Plus keep in mind that people love outdoor gear. It’s insanely fun to go outdoors but you never know if you have right equipment. To figure out what’s right, these outdoor review sites help immensely!

Monthly Visitors (SimilarWeb) : 1.60K Visitors Average Post Length: 5,000 – 7,000 Words One of Most Searched Products: Arc’teryx Jacket How much do they make: I don’t know how much they make.

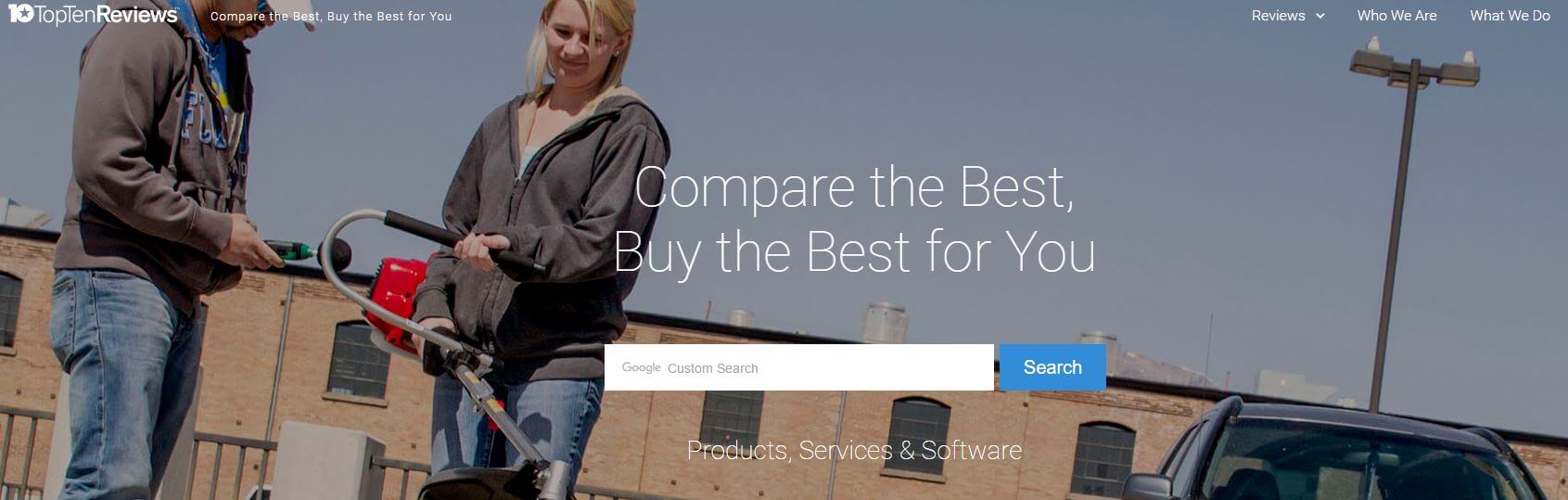

TopTenReviews – Amazon Affiliate Website Example

TopTenReviews.com

This is an older site (2003) with some heavy domain authority. That explains the crazy amount of content this site contains. It’s helpful though when you have 350+ employees. This isn’t a small enterprise, and they still utilize the Amazon Affiliate network to monetize their site. They use long and wordy articles to review products, maximizing the SEO of each page. The biggest difference from this site and others is the amount of digital content these guys review. Their digital content ranges from Antivirus Software to Credit Card processing. This isn’t a typical Amazon product, but digital content can earn affiliate commissions through other sources than Amazon. Amazon is a great resource to monetize your site, but it’s definitely not the only way.

Monthly Visitors (SimilarWeb) : 12.80M Visitors Average Post Length: 3,000 – 5,000 Words One of Most Searched Products: Best Printer How much do they make: I don’t know how much they make.

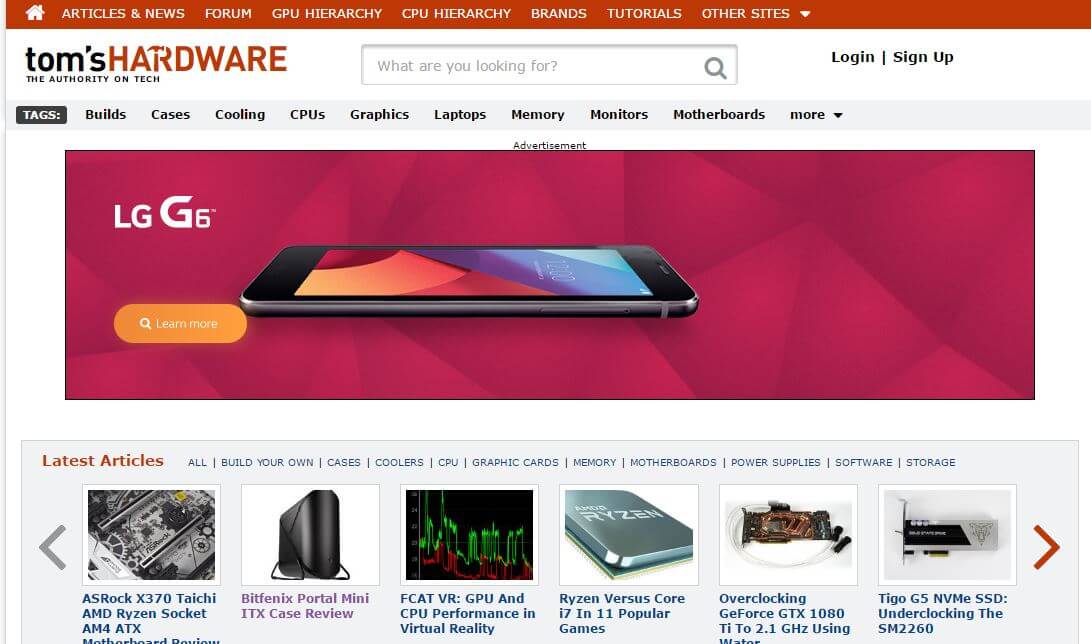

TomsHardware – Amazon Affiliate Website Example

TomsHardware.com

Do you remember 1997? That’s when this website was created. You could maybe tell from the website homepage that looks more like About.com than a review website, then again they have over 1.5 million pages indexed. Don’t make the same mistake I did, this isn’t a door and sink hardware company, this is computer hardware for hardcore nerds who build their own computers. I’m sure this site is at the forefront of every build-it-myself computer geek out there (I’m one ). The site is now owned by Purch, the same people who own TopTenReviews. These guys have really got a good handle on successful Amazon Affiliate Websites.

Monthly Visitors (SimilarWeb) : 47.50M Visitors Average Post Length: 500 – 1,000 Words One of Most Searched Products: Best Gaming Monitors How much do they make: I don’t know how much they make.

CarSeatAnswers – Amazon Affiliate Website Example

CarSeatAnswers.com

It’s really simple and plain websites like this that make me happy! If something this plain can bring in so many visitors, than someone creative and design oriented like me can do better, right? CarSeatAnswers focuses on keywords like “Car Seat Answers” and “Car Seat Guide” and “Which Seat is Safest for a Baby’s Car Seat” then writes 700-1,000 word articles with no photos except for the Amazon Products sold throughout the article. This is one of the simplest example, but it still brings in visitors even with a small amount of domain authority. It gives you hope though, that you can easily create a successful website, right?

Monthly Visitors (SimilarWeb) : 3.40K Visitors Average Post Length: 300 – 500 Words One of Most Searched Products: Best Car Seat How much do they make: I don’t know how much they make.

KichenFaucetDivas – Amazon Affiliate Website Example

KitchenFaucetDivas.com