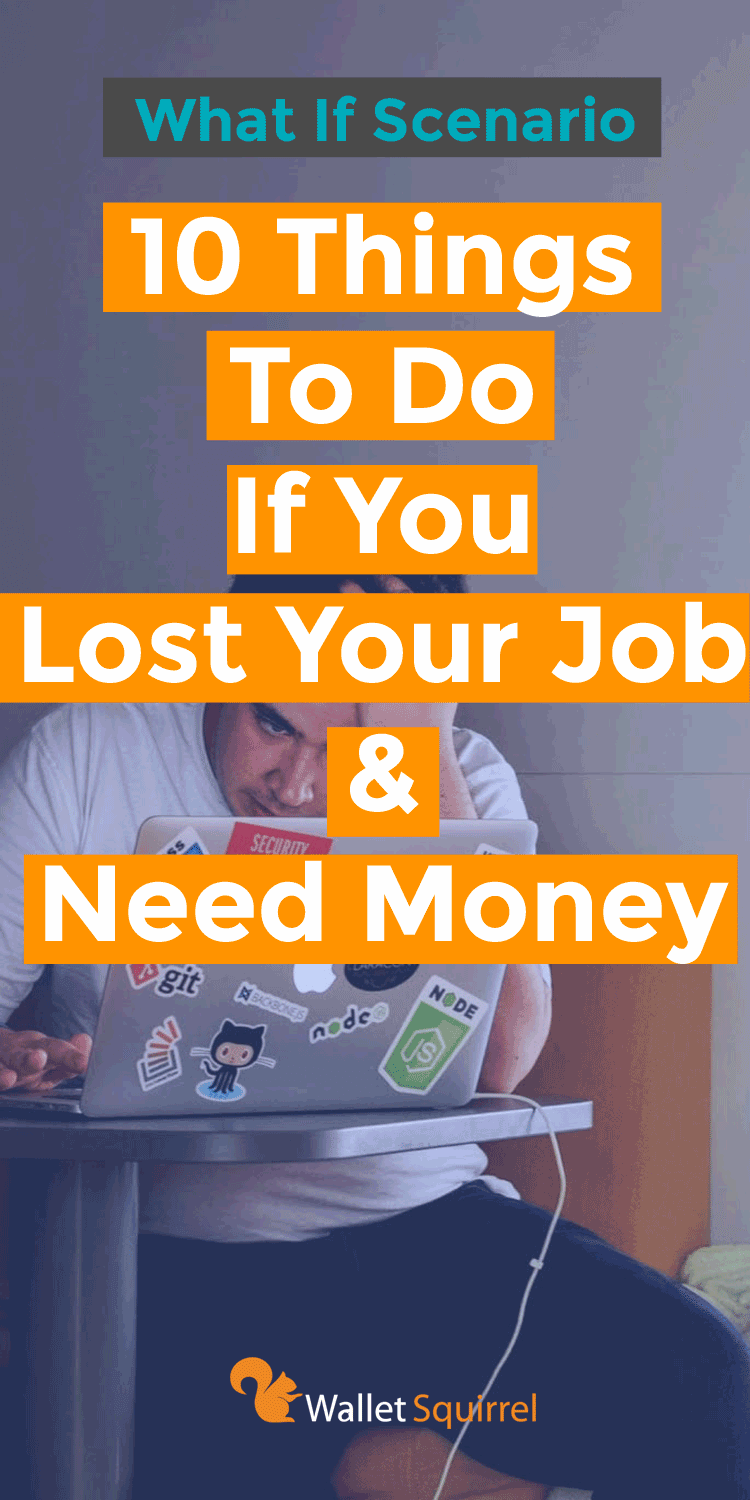

There is no bad time to become a blogger. Simply the sooner you start, the larger a blog can grow. In this article, we’re going to show you how to start a money-making blog in under 5 minutes.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

We all have the stress nightmare where your boss comes out of the blue and says “You’re fired”. That’s it and we spend the rest of the night in a panic. The problem is if it did actually ever happen, most of us don’t have a plan in case we do get fired.

Whether you’re thinking about losing your job due to stress, COVID-19, or any slew of reasons, it helps to have a plan. To lay out a blueprint, if this ever happened to me, here are 10 things to do if you lost your job and need money now.

Immediately Start

First, Take A Breath

It seems silly and not productive, but taking a breath is essential. People are let go or fired for a number of reasons and it’s not always a reflection of you or your work. Some things are just out of your control. Take an hour or take a day to let is sink it so it doesn’t consume you later.

1. Review Your Finances

Take a look at all the money you currently have. I personally use Mint to see all my bank accounts, credit card debt, and student loans all at once. You don’t need this, but make a list of every dollar in your possession. Look over your finances and get a feeling of how long you’ll last without a paycheck. It may not be pretty, but it’s something you absolutely need to know.

Know how much you need to spend each month, here is an example monthly breakdown:

Apartment & Utilities ($XX)

Food ($XX)

Car Insurance ($XX)

Cell Phone ($XX)

Internet ($XX)

Misc. ($XX)

PS. Also, consider health insurance as a cost. In most cases, your old employer would have provided this for you, but you need to talk to your HR to see how long this lasts. You may need to pick up supplemental health insurance until you get a new job.

Hopefully, you have some sort of Emergency Fund you can access if you lose your job. Your emergency fund will help cover rent/mortgage, food, and those expenses your paycheck normally covers. Most emergency funds should cover 4-6 months of expenses. If you don’t have an emergency fund, start saving up now but the following tips can still help.

I personally have an emergency fund I keep in a savings account, that will last me around 6-7 months. I know many people don’t have that. It took me 5 years to build. However it’s one of the best things I’ve ever done because it provides a mental safety net.

Let’s continue though as if you have $0 emergency funds.

If you just lost your job, you shouldn’t be watching Netflix, Hulu, or listening to Spotify. If you have any kind of subscription services that cost money regularly, you should cancel these until you get a job again. It may feel like a nice break watching Netflix between job applications, but you need to save all the money you can until you’re working again. If you feel this is too hard to do, consider using your parent’s or friend’s account temporarily to save money.

Needless to say, don’t make any crazy purchases thinking you’ll get a job next week when “you really try”. Until you have a signed contract with a company, I’d suggest avoiding the mall and any kind of gift ideas. If you can, cancel any flights, trips, running races, etc. Plus always ask if you can get your money back. It may not always be possible, but every little bit helps!

For me personally, I would cancel my gym membership ($73/mo.), cancel my Spotify account ($10/mo.) since there is a free version, and I’d probably quit investing in my brokerage account ($200/mo.) until I have a steady paycheck.

3. Ask to Defer Payments

During hard economic times, many companies are willing to work with you because they prefer late payments to nothing at all. Student loan services are often willing to reconsolidate loans or defer payments. Banks are sometimes willing to defer a mortgage payment or at least help with options. It often just takes a call and asks.

For me personally, I would call my student loan companies and ask to defer my payments until I get another job. That would save me $537/mo.

4. Budget and Eat At Home A Lot

One of the biggest ways people spend money is food and eating out. If you just lost your job, avoid going out to eat with friends (unless it’s a networking thing) or ordering in. It may not be sexy, but cold cut sandwiches, peanut butter and jelly sandwiches, and ramen got you through the dark years, it will again.

You know what you can cut to save money and you’ll see instant savings in your bank account. Remember one of the easiest ways of having more money, is not spending it!

One of the most popular tricks people use to limit spending is paying for food only with cash. The act of seeing the money physically leaving your wallet and the empty vacuum it creates, helps people be more selective with their purchases. I personally use credit cards because I enjoy the cash back, but I can’t argue with the success physical money has in limiting spending.

Start the Job Search

5. File For Unemployment

If you lost your job and actively seeking new work, you can file for unemployment. It varies state by state, but essentially you would file a claim with the Department for Labor and Employment and prove you’re actively looking for work every 2 weeks (depending on your state). Unemployment benefits will pay you a portion (likely small) of your previous salary. This is meant to help lessen the negative impact that unemployment has on the economy. It won’t be a glamorous option and you’ll meet some interesting people, but it will help.

6. Update Resume & Social Media Profiles

This is the time to update your resume with the latest accomplishments, promotions, volunteer efforts, jobs, references, etc. As you start the job search you want to make yourself look as good as possible. However, this isn’t limited to your resume. You should be updating your LinkedIn, Facebook, etc with the latest info so you’re casting a wider net for employers.

Don’t worry too much about how your resume looks, just that the information sounds grammatically correct and makes you look good! Many companies will force to you to copy all the exact same information into their often terrible online web forms. On the bright side, if your LinkedIn is up-to-date, you can always use their “one-click apply” to jobs posted on their site.

YouTube is also a great resource if you use it to better yourself now that you have free time. There are great exercise tutorials on YouTube, classes on coding (if you’re into high-paying jobs), and even brush up on software like Microsoft Excel. Use this opportunity to start a new job with a new skill set!

7. Tell Everyone You Know You’re Looking For A Great Job

It may feel embarrassing for you to tell anyone that you’re jobless. It’s a very vulnerable situation where you feel like something is wrong with you. There isn’t! It’s a normal thing, and job searching is a $200 billion dollar industry. People are constantly moving and switching jobs, you are now just one of them.

In most cases, when you tell people that you’re looking for a job, they want to help! They’ll often share new job openings they’ve heard of, or perhaps make recommendations to people they know in your industry. The fact is your chances of finding a new job dramatically increase when more people are on your team, helping you get a job.

I personally will change my LinkedIn page to “Looking for an Awesome Opportunity” and email my friends and family that I’m actively looking. More often than not, they will understand (because we’ve all been there before) and they’ll want to help!

Some of the best job search tips I’ve ever heard:

I recommend LinkedIn, Google Jobs, and Indeed for job postings. This is what most people use. I often avoid Craigslist.

Always use Glassdoor and read company reviews on how they treat their employees.

If you like a company, stalk their employees on LinkedIn to see if they went to the same schools you attended, clubs you’re in or charities you participate in. Ask them what it’s like there and ask for advice.

Have a salary in mind, knowing how much you need to cover all your expenses.

Make Money Fast When Your Jobless

8. Sell Your Old Stuff for Extra Money

If you just lost your job and looking for extra money, consider selling your extra stuff on Craigslist or eBay. All that extra stuff in your apartment/house like old bikes or snowboards could make a couple of hundred dollars with a new family. That’s a lot of extra ramen noodles! Plus it’s a rewarding feeling getting rid of some of the junk in your life.

9. Write Articles For Money

I write all the time for a blog, but I discovered there are other places on the internet that pay you for writing! I’ve written a couple of articles on Seeking Alpha that pay $35 per article and $0.01 for every page view. It usually comes around $70/article in the long run.

With your new free time, this is probably one of the easiest ways to earn extra money while unemployed. You’ll have lots of extra time and most of the sites I listed pay between $50 – $100 per article.

For me personally, this is my plan. Spend my mornings looking for new jobs and my evenings writing articles. If I can write 1 article a night, at $50 per article. That’s an extra $1,500/month!

10. Side Gigs

We regularly talk about creative ways to make money, but some of the quickest ways to make extra cash are side-gigs. These are tasks that you can do anytime on different established platforms:

Random tasks in your city ranging from moving furniture to assembling IKEA (sites like TaskRabbit)

Many of these could be done in your afternoons while you spending your mornings (often the most productive time of the day) job searching for new opportunities.

Conclusion

Losing your job is incredibly scary, but there are TONS of resources here and online to help you find a new job and supplement your income. Hopefully, this helps make losing your job a bit less scary and aids in setting up your own backup plan!

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

At the end of last year, I was in a career funk. So I considered going back to school to get my MBA (Master’s of Business Administration). I figured with an MBA, you can practically do anything from advancing in your current field or make a complete switch to a new one. Every company values an MBA.

I was so excited! I previously considered the possibility of getting an MBA and my life was in a good position to do night classes. So I began picturing myself adding the letters “MBA” behind my name on business cards and looking up schools.

However, I quickly hit the brakes!

Ask These 2 Questions Before You Pursue an MBA

With many of my friends going back to school or are currently in school. I ALWAYS ask them these 2 simple questions that BLOW THEIR MINDS.

So I decided to ask myself these 2 simple questions to see if I can pass my own “Should You Get An MBA” test.

1. What is the EXACT dream Company and Job Title you want after graduation?

You should know this.

Most people get an MBA because they want to do something in business. They think they need an MBA for potential promotions or career growth.

However, what you should do is FIRST figure out what your dream job is.

You can’t just say “something in business”. If you are going to spend $140,000 or more on an MBA (average MBA costs according to Investatopia). Plus years of your life. You should identify the exact company and job title you want before you even start school. Come on, it’s your DREAM job.

This is a role you’ll potentially be doing for the rest of your life. You should have a clear idea of what it should be. Knowing this will guide every future decision you make within your MBA program, including the electives you take and the networking events you attend.

What’s the point of getting an MBA if you don’t know what you’ll do with it? Seriously? So take a moment and write down your dream job title and company.

2. Have you reached out to your dream company yet?

Once you can identify the exact job title and company you want, you should reach out to that organization and ask what they look for. This should ideally be less intimidating than pondering a future $140,000 MBA student tuition bill.

Usually, a company’s Human Resources department would be willing to meet with you if you tell them you’re considering going back to school to gain the skills necessary to work at their company.

When you meet with your dream company’s Human Resources Department (or any department), you should ask them some of these questions.

My dream job at your company is a Marketing Manager (or whatever it is), what is the typical salary range they get paid?

You should ABSOLUTELY know how much your future job pays because this will inform you how long it’ll take you to pay off your newly acquired student debt. Plus it’ll give you an idea of the lifestyle you can expect once you graduate with an MBA.

While it’s not all about money, you should be aware if your post-MBA salary can cover your student loans for the next 20 years. Are you ok with only eating peanut butter and jelly sandwiches?

What degrees or education do your current Marketing Managers have (or whatever your dream job is)?

This will give you an idea of the education level of their current employees. Some employees may have MBAs and some may not. You should probe deeper into what the HR team looks for in your dream position. Perhaps you don’t need an MBA and you may have the necessary experience to apply that day.

If you need to get an MBA for that position, ask if they have a preferred school or partner with any specific schools. If your dream job regularly partners with a local university and hires exclusively from there. That university may need to be on your radar for potential schools.

Does your dream company offer internships?

Yes, you’re getting an MBA but knowing if your dream company has an internship program is huge. Many companies will hire interns who are working towards their degree and help them grow into the position. There is no reason to wait till after you receive your MBA to apply to your dream company. You should use every opportunity to start making connections.

What does career growth look like at that company?

If your dream job is to be the Chief Executive Officer (CEO), they won’t just hire you out of school. What entry-level roles will you need to start off with and how does one become a CEO? How did the current CEO get his role and what did they do before that? Some jobs aren’t attainable right out of school, even with an MBA. You need to understand what your career path would look like moving into your dream position. You should understand what this looks like.

When I considered an MBA, I failed this checklist

Last year when I considered getting my MBA, I went full-throttle and visited 3 different universities. This included dropping in classes and meeting with professors.

I received all the brochures, met with all their “advisors” and compared costs ($39,000 – $80,000). I did soft applications and confirmed I would be accepted to each of them.

I was so freaking close to full-out applying.

I knew I wanted to do something in finance because I LOVED writing about finance (hence why I started a blog). So I figured I’d get an MBA focused on finance.

This is how most people start the MBA journey. They love the idea of a degree, so they first get an education THEN figure out where they want to work.

I know this because that’s how I choose my bachelor’s degree. I went into Landscape Architecture without actually knowing if it was my dream job. I just thought it would be fun to draw and select plants. I didn’t learn till after internship opportunities and after graduation that it’s not what I wanted.

So I took this MBA checklist and failed.

When I looked at my dream job, there were some finance positions like Financial Planner, Mutual Fund Manager, Financial Analyst that sounded interesting. Yet when reviewing, I wasn’t drawn to them with such vigor that I could stomach another $140,000 in student loan debt.

Only one position that I was excited about, sounded fun, but it earned even less than I was making now. So I had to ask myself if I would be willing to take on $140,000 debt for a lower-paying job? It wasn’t a great option even with all the extra ways to make money out there like selling photos and earning money from walking.

Do the Math on your Future Tuition

According to Investatopia, the average MBA program costs $140,000, with higher-ranking schools costing more. They’re factoring in tuition, living arrangements, books, and peripheral expenditures. That’s more than the average night-only MBA program I was looking at.

Now factor $140,000 student debt at 6.8% interest which is the average Subsidized Federal Stafford Loan according to Federal Student Aid. Having that kind of student loan debt is similar to buying a house or literally thousands of lego technic sets for my kids.

However, the common response to seeing these numbers is that you’ll be paid more after your MBA. That is perhaps true. The average salary of MBA graduates in a full-time program was $126,919. This was taken from US News when they interviewed companies mainly on the east/west coasts which usually provide a higher salary than the Mountain States and Midwest.

Conclusion

Most people like me had to make an insane decision in high school to pick a college major before entering college. So at the same time, I was focused on rehearsing for the school musical and wondering if the homecoming queen liked me (she didn’t). I was asked to choose a degree that would affect the rest of my life. I was not ready.

Going back to school for your MBA doesn’t have to be like that. There isn’t any timetable, no matter what college recruiters try to tell you about upcoming semester deadlines. You have all the time in the world to choose if an MBA is right for you.

So if you’re considering going back to school for an MBA, you should have an idea of what your future will look like. You should identify your dream job at your dream company. This is your opportunity to do WHATEVER you want in the world, and create a plan that extends after graduation.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

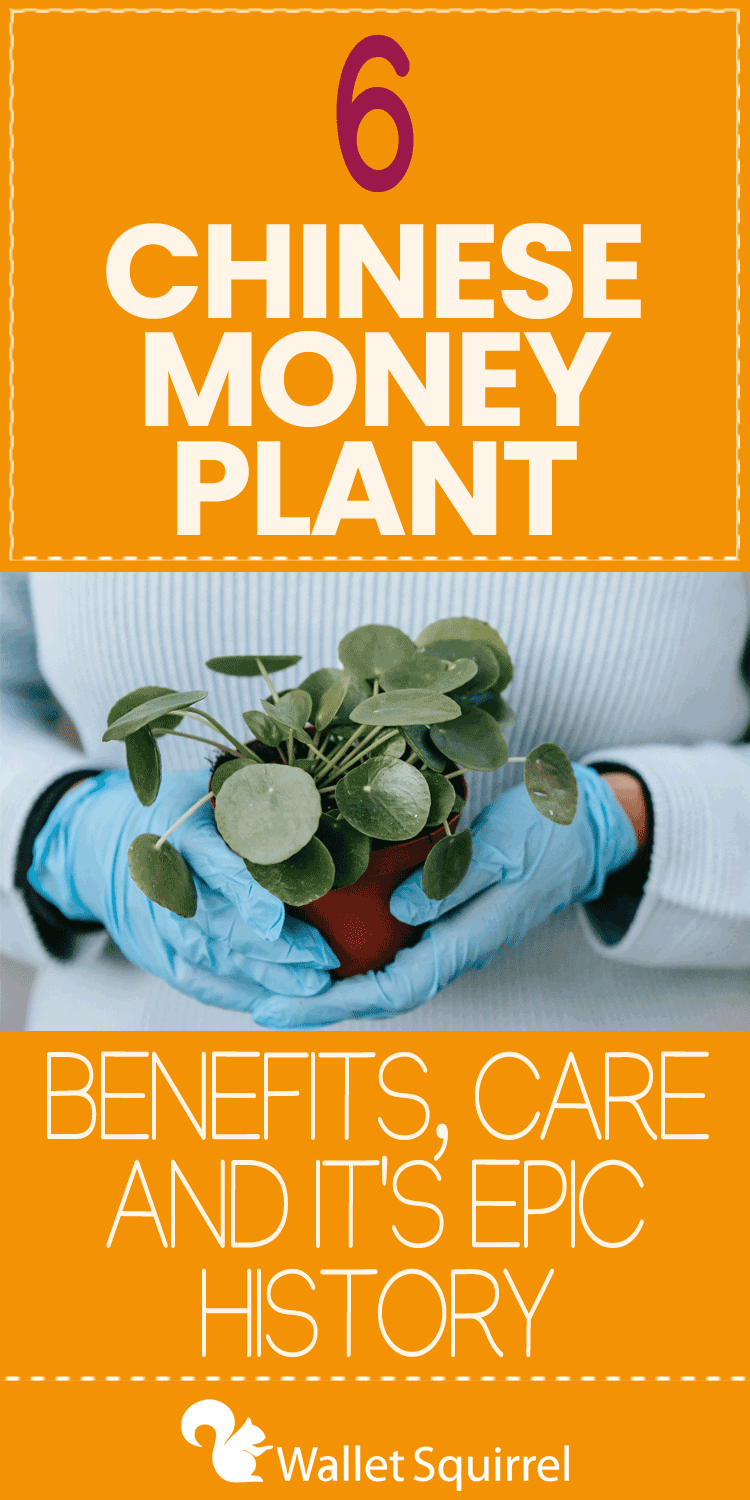

Money plants are famous for the exciting myths around their benefits, but their recent popularity on social media has brought a new wave of interest for home offices. As personal finance enthusiasts, we can’t help but cover the benefits of money plants, different types of plants considered “Money Plants,” and their exciting history around wealth.

6 Chinese Money Plant Benefits

These are the most widely known Chinese Money Plant benefits on the internet. The benefits apply to both money trees and money plants (more on the differences later). We’re not here to say if they’re right or wrong, but simply enjoy the lore around these fun plants!

1. Brings Prosperity and Wealth – Money plants are most widely known to bring good luck and wealth to the homeowners that take care of the plant. The healthier the plant, the greater prosperity it will generate!

When you give a clipping of your money plant to friends, it’s believed that you are giving your friends wealth and prosperity. The clipping will grow with little effort and bring great joy to whoever receives your generous gift.

On the other hand, some lore suggests a power to growing a money plant from clippings stolen from another homeowner. In this case, the thief will gain wealth while the previous homeowner will lose their wealth. It’s like stealing someone’s luck, so some homeowners are protective around their money plants.

2. Reduces Marital Problems – Whether it’s the calming nature of plants or the unique properties of this plant, money plants are known to minimize marital problems.

The five-leave patterns of money trees relate to the five fundamentals of Feng Shui, so many people associate the properties of money trees with the properties of Feng Shui. In this case, money trees kept in the southeast direction of the home help maintain peace and a healthy environment for marriage. This positive environment reduces bad luck, thus providing good fortune and wealth for your marriage.

3. Creates A Positive Environment – This is similar to #2, but we wanted to stress that you don’t need to be married to enjoy the positive environment that money plants create. Plants brighten the atmosphere of any room. Studies have shown that biophilia or viewing nature can positively impact people’s health, so having an actual plant in your home can only help create a more positive environment. You’ll feel calmer, happier and those feelings will lead to a more positive life!

4. Health Benefits – There are many myths around the health benefits of money plants in reducing stress, providing an atmosphere, and bringing calm. Often referred to as biophilia, viewing nature has many health benefits. Many hospitals are filled with photos of nature because it helps feel good and improves recovery.

PLEASE KNOW we’re speaking to the calming effect these plants have. Some plants considered money plants are, in fact, poisonous if ingested. Often they won’t kill you but will cause vomiting and illness symptoms if ingested by dogs, cats, or tiny humans. Check each species of the plant before bringing it into your home.

5. Purifies The Air – In 1989, NASA was involved with a study that tested plants’ ability to filter the air onboard space stations. It was a small study and contained a controlled environment, but the study showed that plants clean the air! Further studies showed that plants could help remove harmful gases in the air, which helps improve health. These studies created a surge of house plants during the 1990s.

Later, reviewers argued you would need hundreds of plants in your house to achieve the same level of air quality that the small NASA study achieved. However, if we take the benefits of money plants to heart, any in your home could improve your health and wallet!

6. Helps Fight Radiation In Your Home – Many people often forget a small amount of electromagnetic radiation radiates from the gadgets in our homes. From wifi, phones, TVs, and more, we’re bombarded with signals regularly. In most cases, these signals are harmless and nothing like standing next to a nuclear reactor. However, some people claim to have electromagnetic hypersensitivity and express symptoms such as headaches and sleep disorders when surrounded by these EMF fields.

Luckily money plants and other anti-radiator house plants help absorb these electromagnetic fields with no harm to the actual plant. You’ll see some people place their money plants by their computer, wifi router, and TV. Their money plants help protect them from the EMF radiation they may be hypersensitive to. Cool right!

Money Plant History Around Wealth

History around the Money Plant has several iterations, as any myth does, but all these myths agree that it started initially from the Money Tree. A petite Asian tree that, when its stems were intertwined, the tree would continue to grow in this pattern on its own.

The unique braided stem of the money tree stirred massive popularity and speculated many myths around its mysterious nature. Some of these myths connected the tree’s five-leaf pattern and the five fundamental Feng Shui elements (wood, water, fire, earth and metal), which symbolized good luck and good fortune. While other wives’ tales speculated, its leaves resembling the shape of paper money could bring wealth to the home.

Types of Money Plants

Numerous plants represent wealth and prosperity as wive’s tales have spread over the years, and it’s easy to get confused. We find it simpler to focus on the Money Tree, whose leaves are said to represent paper money, and the Money Plant, whose circular leaves are believed to represent coins.

Pilea Peperomioides (Chinese Money Plant)

Pilea Peperomiodies is the botanical name of what many consider the Chinese Money Plant due to its circular leaves resembled the leaves of the Money Tree but in the shape of coins. Other names for this plant include the coin plant, the friendship plant, the pancake plant, and the UFO plant.

This plant is excellent for beginners as it’s easy to care for, usually only grows 12 inches tall, and maintains beautiful dark green leaves to decorate any home!

The Chinese money plant creates lots of little offshoots to collect and give to friends. However, getting your hands on one can be difficult as not many nurseries keep this plant in stock. We’ve found the Chinese Money Plant on Amazon as the best option to start with a single plant.

Chinese Money Plant Care

To help your Chinese money plant care, beginner houseplant owners need to keep their money plant in a bright room but away from any harsh rays piercing through windows. Usually, watering once a week will be perfect in well-drained soil. A rule of thumb is the 2” of topsoil should be dry between waterings. Also, consider periodically rotating your plant so it’ll grow symmetrically.

To help gauge the health of your plant, here are a couple of guidelines.

Money Plant Leaves Turning Yellow

If your money plant leaves turn yellow, it’s likely due to overwatering, or your pot isn’t draining well. Your money plant roots could be waterlogged and may rot in the damp soil. Simply let your soil dry out before you water again, or if the problem continues, you may need to replace the soil.

Money Plant Leaves Curling, Drooping and Wrinkling

When your money plant leaves are curling, droopy or wrinkling, it’s likely thirsty for water. Think of it like a sponge wringing itself out to get every last drop of water stored. This plant needs lots of light, but direct light may be harsh and drying it out. Give the poor fellow a deep watering.

Give Money Plant Cutting To Friends

These plants are perfect for giving to friends as they produce lots of little offshoots that can be easily separated to place in a new pot. Simply find an offshoot on the edge of the massing and get enough of the offshoot that includes some roots with a clean sharp knife. Place the offshoot in a pot at least 2” wide and care for it as usual. Give it as a perfect gift to friends and wish them a good fortune!

Pachira Aquatica (Money Tree)

The Pachira Aquatica is the botanical name for the Money Tree and one of the most popular indoor houseplant trees. As we stated in the history of the money plant, the Money Tree and its mysterious ability to braid its stems are what started the myths bringing owners good luck and good fortune.

Another reason leading to its popularity is its easy care. The money tree needs little water (once a week), will grow in most pots, growing up to eight feet tall.

An exceptional little tree for people to start their house plant collection, the money tree will bring a little wealth to your life. We’ve found several retailers selling them online and found the Money Tree on Amazon one of the best places to start your money tree journey.

Money Tree Care

The money tree is easy to care for as it requires little water (usually once a week) and loves bright light while avoiding direct sunlight. To help grow the money tree, add fertilizer no more than once a month.

To help gauge the health of your plant, here are a couple of guidelines.

Money Tree Leaves Turning Yellow

If your money tree leaves turn yellow and fall off, it’s usually a sign of overwatering or a problem with the light. Remember, the money tree only needs water once a week, so if the soil is always wet, the roots may be waterlogged and leading to root rot. Let the soil dry completely before watering again, and feel free to prune any overly yellow leaves on the tree.

Overwatering is usually the problem, but it may be over or under-lighting. Make sure the tree is placed in a bright area of the house while avoiding direct light.

Money Tree Shriveled Leaves or Trunk

If the money tree has leaves shriveling up or its trunk becoming wrinkly, soft, or shriveled, the problem may be underwatering. Think of it like a sponge where the tree is trying to wring itself out for any last water storage. Use this as an indicator to give it a deep watering.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Child psychologists and pediatricians have recognized that today’s lack of play contributes to children’s overall lack of well-being. An increased focus on academic activities, overly structured family, school, and extracurricular schedules have led to less playtime for kids.

If you’re looking to give your child a strong foundation for academic success, it may be shocking to hear that the best thing you can do is allow them to play more every day. Playing develops strong social skills, which in turn gives them the best footing for learning. It’s been proven that the best predictor of academic performance in eighth grade was a child’s basic social skills in third grade. Research shows that play is beneficial for kids’ development and learning, yet they aren’t getting enough.

So what’s an affordable change parents can make that doctors recommend and kids will put their device down for? It’s a 4,000-year-old invention that everyone can agree on – Board Games. They are such an effective tool for developing social skills that leading experts and therapists have played board games with kids for decades. It’s why Dr. Jon Freeman, Clinical Psychologist, Neuroscience Researcher, board-and-card game enthusiast, and Founder of The Brooklyn Strategist, offers an after-school social skills program at his Board Game cafe.

“After we observed a shortage of social skills in kids, we realized how much work there was to be done,” he said. “Our programs focus on neurodevelopment by having fun and developing and articulating strategic approaches through socialization and gameplay.” It’s such a game-changer that New York school administrators recommend kids play at Brooklyn Strategist after school.

Wait, So Playing is Actually Learning?

According to the American Academy of Pediatrics (AAP), playing is serious business for a child’s health and development. Their report, The Power of Play: A Pediatric Role in Enhancing Development in Young Children, explains how playing with both parents and peers is essential to developing thriving brains, bodies and improving social bonds. It’s so critical the AAP is encouraging pediatricians across the country to write Prescriptions for Play at well-visits to combat the decades-long decline of playtime for kids.

Play is not just an important teaching tool. It’s the best teaching tool. “The seemingly simple activities that kids enjoy most help them explore and understand the world around them,” says Anna Yudina, Senior Director of Marketing, The Toy Association. Their Genius of Play program celebrates the 6 Benefits of Play: Physical, Emotional, Social, Cognitive, Creative, and Communication by giving parents and educators ideas on incorporating more play into the day.

How Do Board Games Actually Teach Kids Important Social Skills? 4 Experts Explain

What if I told you that playing board games can help kids in both school and life? As well as teaching kids about money. Well, after decades working with kids and families, that’s the recommendation from Leading Emotional Dynamics expert, Erik Fisher, Ph.D., aka Dr. E, Keri Wilmot, Occupational Therapist, and Toy Expert aka Toy Queen, Dr. Amanda Gummer, Founder and CEO of Good Play Guide, and Dr. Jon Freeman, Founder of Brooklyn Strategist.

Board Games, Basic Social Skills and Young Kids

Playing preschool-level board games may seem so simple on the surface. When you look closer at what’s going on, it’s providing teachable moments, improving social interaction, and developing good social skills amidst all the fun!

“As an occupational therapist of 20 years, I’ve played a lot of board games with kids of all ages and abilities,” says Keri Wilmont. “Board games are a great way for kids to alternate going first, taking turns, listening, and learning how to cope when others might not want to follow the rules and try to cheat or bend the rules in their favor.”

“Therapists aren’t playing games with kids by accident,” adds Dr. E. “Games can be an avenue for them to build many of the cognitive skills required for successful academic performance, as well as life. Games practice and build attention, concentration, memory, critical thinking, reasoning, and problem-solving skills. And as a bonus, it helps them “learn how to manage losing and gives them a chance to see that failure tells us when it is time to learn.”

Board Games, Great Social Skills and Older Kids

Playing board games presents an opportunity to understand group dynamics, practice interpersonal skills, improve social skills, practice specific social situations and develop the all-important skill of working well with others. With high school, college, and the working world full of group projects, playing board games helps to improve emotional intelligence and develop essential life skills.

“Making new friends and being able to collaborate with another person is important in a school environment. Board games allow kids to rehearse basic social skills through play,” said Dr. Amanda Gummer, widely considered the go-to expert on play, toys, and child development. “Fast-paced, luck-based games with a focus on fun can be a great way of getting children more opportunities to play with others and begin to develop an understanding of friendly competition.”

“More recent games have introduced cooperative elements, and that’s a great game-changer (no pun intended) regarding social dynamics. Instead of the neurotransmitter reward (e.g., dopamine) coming from being declared the winner at the expense of everyone else, the reward is now associated with working as part of a larger group,” explains Dr. Jon Freeman.

An example of cooperative games that build strong social skills is Role-playing Games (RPGs), like Dungeons & Dragons and Pathfinder. Players meet in small groups and work together under the game’s rules to accomplish imaginary tasks, but they’re using tons of interpersonal skills too.

“By RPG games’ very nature, players are required to interact with others, problem-solve how to attain a shared goal, and then divvy up the treasure when the goal has been attained. Very often, survival requires help from another player,” says Dr. Jon Freeman. “So, throughout the experience, players are simultaneously considering their own characters plus how their character interacts with other players in the group and how others perceive their character. If we can teach kids to verbalize thoughts and practice conflict resolution in games, the hope is they will have better outcomes later in life in difficult social situations.”

Heather Bernt-Santy, M.A.ED., aka That Early Childhood Nerd, sums it up when she says, “If you limit the play, you limit the learning.” So, shall we play a game?

10 Best-Selling Board Games That Teach Specific Social Skills

If you’re sold on the idea but are unsure what to play next, here’s a list of 10 beloved board games that experts recommend, kids love, and are favorites in our house. If you want to test drive some of these before buying them, many libraries have board games you can borrow for free, just like books!

1.Sneaky Snacky Squirrel Game

2-4 players | Ages 3-6 | Social Skills: Waiting Your Turn, Perseverance, Sportsmanship

For five years, it’s been the best-selling preschool game for a reason. It’s easy to play. Little kids love to spin the spinner and feed their squirrel five different colored acorns. While you might be in the lead one minute, you may get a strong breeze next and have to return your acorns and start again. It’s a big winner with the four-year-old in our house!

2. Candyland

2-4 players | Ages 3+ | Social Skills: Waiting Your Turn, Perseverance, Sportsmanship, Following Instructions

For over 70 years, this adored, easy-to-understand game set within a kids’ dreamland of candy has been a go-to for families. While it seems simple, it introduces the concept of rules, turn-taking, following directions, and winning and losing to preschool-aged kids. All the candy-themed elements are a hit with any treat-obsessed kid, too!

3. Zingo

2-6 players | Ages 4+ | Social Skills: Sportsmanship, Following Instructions, Attention Skills

It’s Bingo with a Zing! Fifty million families have purchased this kid favorite, award-winning Toy of the Year. Slide the zinger, make a visual match, and fill your picture bingo card to win! We’ve been playing this game regularly for years in our house, and it’s so much fun no one realizes it’s teaching reading fundamentals as well.

4. Richard Scarry’s Busytown, Eye Found It

1-6 players | Ages 4+ | Social Skills: Collaboration, Teamwork, Following Instructions

If you want to introduce your young child to the fun of board games but they are still getting used to losing, this game is for you. While the game’s goal is to move your piece through the board, no one wins until everyone gets to the end. This approach focuses the fun on playing and not necessarily winning, keeping the tears away.

5. Ticket to Ride

2-5 players | Ages 6+ | Social Skills: Sportsmanship, Following Instructions

This award-winning board game is so popular that they released a Juniors version so younger kids can get in on the fun (and improve their social skills too). If your train-loving toddler is now older, give this beloved cross-country train adventure board game a try! Players collect and play cards to own railway routes connecting cities like Miami and Seattle all across America.

6. Uno

2-10 players | Ages 7+ | Social Skills: Sportsmanship, Following Instructions, Attention

This classic game that’s “easy to pick-up and hard to put down” has been played for 50 years. While it seems like a fun, competitive race to get rid of your cards first, kids are practicing laser-focused concentration, following directions, and being a good winner and loser. This game is perfectly sized to bring along on your next family trip! The size of a phone, you can even fit it in your carry-on for in-flight fun!

7. Lattice Hawaii

2-4 players | Ages 8+ | Social Skills: Attention, Following Instructions, Sportsmanship

With more than eight awards to its name, this game is beloved by people of all ages. Described by the creator as a mix of Rummy, Sudoku, and a Rubik’s Cube combined with inspiration from Hawaiian myths, give this fast-paced tile-based game a try.

8. King of Tokyo

2-4 players | Ages 8+ | Social Skills: Following Instructions, Sportsmanship, Confrontation

Created by the same game designer behind Magic the Gathering, it’s not a surprise it’s won many awards, including Best Family game. My eight-year-old loves the chance to fight mom, dad, and his sister in an acceptable manner! The fact that you’re playing mutant monsters, giant robots, and weird aliens destroying the city to become The King of Tokyo doesn’t hurt either.

9. Pandemic

2-4 players | Ages 8+ | Social Skills: Teamwork, Collaboration

There’s nothing like the challenge of saving humanity from a pandemic to get a family or group of friends working together! This multi-award-winning cooperative board game gives each player a role like a medic, scientist, quarantine specialist. The group recognizes and applies the strength of each player’s part to cure a deadly disease before it’s too late.

This 25-year-old board game, bought by 20 million people, has been called the most beloved board game of all time by table-top enthusiasts. And it’s definitely one of the favorites in our house. The countless ways you can develop the Island of Catan lends to endlessly fun replays of the game. Players as young as six can enjoy Catan with their Junior pirate-themed version with a simpler playing style.

This article originally appeared on Your Money Geek and has been republished with permission.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

“I want to quit my job. It’s time to become the CEO of my own life. I’m going to take control.”

I’ve heard this many times from friends. Quitting your job to pursue your passions could be the best thing you ever do. It could also totally screw up your life.

Do you want to quit your job in the near future? Before you quit your job I want you to look at a few potential issues (along with solutions) so that you don’t end up broke and begging for your old job back.

In movies or in motivational videos on YouTube, the story is usually the same.

The person quits their job with no safety net or any sort of backup plan. They tell their boss off and leave their job. They’re confused for a few days or possibly a few weeks before meeting a guru who changes their life. They usually end up starting some billion-dollar business or things just work out for them. Now they’re rich and married to a gorgeous partner.

This person then goes on to live a successful life where they share nonstop memes about how self-employment is the best thing ever.

In reality, it doesn’t work like this.

Quitting your job to work for yourself is very scary and intimidating. You’re going to experience many issues that won’t just go away. You’re going to be challenged like never before. You’re going to regret making the jump almost daily.

Let’s look at the issues (and solutions) associated with quitting your job to work for yourself…

What issues will you experience when you try to quit your job?

Before you quit your job, I want you to think about these issues. I’m not here to glorify working for yourself. You already know how much you hate your job and how badly you want to work for yourself.

I’m here to help you work self-employment on issues I had to figure out on my own.

What are the common problems that you’re going to experience when you start working for yourself?

Issue #1: You’re going to struggle to find a new schedule.

When you have a job, you have a set schedule. You’re told when you have to be there, when you can go for lunch, and when you can go home. You have to abide by the schedule or else you’re going to be fired. You never think about your start time or finish time.

When you work for yourself, you’re the boss. You get to decide when you start work, when you go for lunch, and when you’re done for the day. There’s a lot to think about.

You might be thinking that you’re going to be a productivity machine now that you have all of this free time.

I have some bad news for you. More time doesn’t equal more work done. I usually loiter around most of the day until it’s time to get some serious writing done at the worst times possible. I usually find myself working on the weekends when everyone wants to have fun since they don’t have to work.

Issue #2: Dealing with family and friends who want to interrupt you or give you unsolicited advice.

“Can you help me move since you’re free during the day?”

“I’m going to be in your area around noon, let’s do coffee!”

“Why would you quit your day job? That’s crazy!”

Those closest to you want what’s best for you. They also will think that you have all of the free time in the world now that you don’t have a traditional 9-5 gig.

You’ll have friends scold you, you’re going to have friends who think that they can just ask you for anything now since you don’t have a job, and you’re going to find that those around you may think that you’re not making the best move.

Dealing with close ones becomes even trickier when you have a family that you’re responsible for. It’s not exactly easy to give up a guaranteed income to chase the unknown.

Issue #3: Being in charge of everything is a lot to handle.

You’re in charge of everything from marketing to accounting. It may feel exciting to put “CEO” in your social media profile, but this means that everything falls on you now.

You have to deal with the following when you work for yourself:

Design work.

Accounting.

Sales.

Marketing.

Human Resources.

Technical support.

Customer service.

You can outsource most of this, but that won’t be free. You also have to decide what gets outsourced and what you’re going to do on your own based on costs and your skills.

Issue #4: Making money.

How are you going to make money on your own? How will you match your previous salary and everything that goes with that (retirement plan, health benefits, etc.)?

When you have a job, you know when you’re going to get paid and you know how much you’re going to get paid.

I have friends who are on salary who know exactly what they’re going to get paid and the exact moment that they’re going to be paid.

When you’re on your own, you have no idea when you’re going to get paid or how much you’ll be making. Sometimes, vendors will delay payment or people will try to get you to “work for exposure.”

You can also lose a major client due to no fault of your own. You can find yourself scrambling for money to just survive.

Issue #5: Your benefits and retirement planning.

I know many friends who stay at their jobs simply for the benefits and retirement planning. When you’re on your own, you have to figure out all of this.

How do you overcome these struggles of working for yourself?

Now that we looked at the most common issues with working for yourself, it’s time to overcome these struggles.

Solution #1: Trying to find a new schedule.

You have to tackle this first if you want any chance of surviving self-employment. You need a schedule because it’s far too easy to take a Monday off or to binge watch Netflix. You then end up catching up on the weekends and pissing off everyone around you.

How do you set a schedule now that you’re on your own?

Find an “office” space. This could be an extra room in your home or the local shop. You need to go somewhere to get in the zone.

Create work hours. You need clear working hours so that you’re not always on.

Focus on the work that brings in the money. It’s easy to get caught up in social media filters and things that don’t mean anything. You have to focus on what’s going to bring in the majority of your revenue.

Know when to stop working. You have to know when to stop for the day. You can’t always be working.

It won’t be easy at first, but hopefully, you can get into a decent routine.

Working for yourself doesn’t mean that you have free-time 24/7. You just have control over when you get to work and when you get to take some time off for yourself.

Solution #2: Dealing with friends and family.

It’s critical that you set expectations with your friends and family. There’s no other way around this. You have to sit those close to you down and explain what you’re doing.

On the flip side, you don’t have to explain yourself to every single friend or acquaintance from work. You don’t have to justify your decision to Steve from Accounting or some random dude from the gym.

Solution #3: Being in charge of everything.

The good news here is that your small business can stay small. There’s no rule that states you have to hire a whole team. Here’s how I deal with being in charge of everything.

Outsource everything that you can’t do easily and use tools to make your life easier.

Solution #4: Making money.

How do you handle this issue? This is where things get interesting. At your job you likely know that you’re going to get paid. You know when you’re going to get paid and how much you’re going to get paid. I have friends who know to the penny what their paycheck will be.

Here are a few financial rules that you should follow before quitting your job:

You have to be making money with your business before you quit your job.

To ensure that you can survive the lean times, it’s important that you save up six months’ worth of expenses in an account.

I’ll say it again: prepare your finances before you quit.

Solution #5: Your benefits and retirement planning.

There’s no easy solution here. You’re going to want to take care of this paperwork before you quit your job. You’re going to have to reach out to other self-employed folks and you’re going to have to do your research.

You should absolutely take care of this before you quit your job. I just don’t want you to quit your job and then realize that you suddenly have no retirement plan.

Bonus section: A few other things to keep in mind before quitting your job…

As I finished writing this article on quitting your job, I realized that I missed out on a few factors that you should consider.

Here are 4 more bonus considerations before quitting your job:

Job searching. Will you be looking for another job in the near future? Are you taking a career sabbatical to work on your own business?

Updating your social media. Don’t forget to update your social media information to reflect your new situation.

Interview skills. What will you do about your interview skills? The further removed that you are from the interview process, the more difficult that it will be to maintain your interview skills.

Your social life. What will you do for your social life? Many folks only hang out with co-workers. Will you make new friends now? What will you do to combat the loneliness that comes with working from home?

That’s what you absolutely need to think about before quitting your job so that you don’t end up feeling overwhelmed. This may be a lot to think about but that’s because quitting your job isn’t a decision that you should take lightly.

Martin of Studenomics makes personal finance fun since you have enough to stress about. You can click here to check out the wide range of content on everything from student loans to getting paid to drink coffee.

Three weeks ago, a friend asked “What happens to debt when you die”. Now, this wasn’t a morbid question, I’ve simply just become the personal finance guy in my little group of friends, and they wanted to know what happens. The incorrect answer is “You’ll be dead, why do care?”.

What essentially happens when you die is “Probate”. It’s the process of paying off outstanding debts and distributing your wealth to your beneficiaries with your “estate”.

What’s in my Estate?

Your estate is essentially your net worth. This is made up of your home value, bank accounts, car, boat, RV and all your smaller assets as well such as paintings, flat screen tvs, etc. Essentially everything you have to your name, including your name. (source)

Your estate is everything you have, to pay off your debts first then distribute to your heirs as dictated in your Will. However some people don’t have enough money to pay off all their debt first, so I’m going to focus on what happens to your debt when you die that you can’t pay off.

Credit Card Debt – What If I Can’t Pay This When I Die?

Millions of Americans have credit card debt, so I was curious about this first. If you’re the only name on the card, the debt stops with you. So if you don’t have enough assets (money) to pay off your credit card debt. Then the Credit Card company simply has to take the loss and move on and your heirs aren’t responsible for paying it off. (source)

They can though, go after a “co-signer” on your credit card. So always be careful of co-signing anything. However, if you’re just authorized to use the credit card, you’re not liable to pay off the debt because you’re not the actual owner of the credit card and don’t carry the financial liability.

Student Loan Debt – What If I Can’t Pay This When I Die?

If your estate can’t cover your student loan debt, then that’s where the buck stops. Unless you had a co-signer on the account, no one else including your heirs, are responsible for that debt.

It was interesting to hear though that according to Nerd Wallet, collection agencies may still legally contact your family members to “discuss” student loan debt, but they can’t mislead your heirs into thinking that they’re responsible for your student loan debt (source). Not sure why they would do this unless they were trying to guilt your poor grandma into paying off your student loans for moral reasons. Those bastards. Be sure to send them a letter asking them to stop and request a read receipt.

Car Loan Debt – What If I Can’t Pay This When I Die?

This was interesting. If your estate can’t pay off your car loan debt then they can repossess your car. This makes sense, it’s a tangible asset that can be taken back if not fully paid off. How I paid off my car.) However whoever inherits the vehicle can just continue making payments on their inherited Ford Fiesta and the bank is unlikely to take any action as long as they continue to receive money. Remember it’s all just business. (source)

Home Loan Debt – What If I Can’t Pay This When I Die?

This is really the least of my concerns since I rent a studio loft downtown, but for some friends who recently bought a house, let’s chat. Due to the 1982 federal law, the surviving spouse may continue to make payments to the mortgage without having an issue (source). They can simply continue to make payments similar to how the recently deceased did or sell and keep the difference in monetary value.

Things get a little murky with mortgages with a “home equity line of credit”. These are usually paid off during the probate process but may involve selling the house if your assets don’t cover the debt. If you’re worried about this, I highly recommend you consult a local attorney.

Is anything safe from debt collectors?

In my research, I’ve found a few things that appear to be safe from debt collectors. These are IRAs, 401(k)s, brokerage accounts, life insurance and pension plans that don’t go to probate, so they won’t be considered a part of your estate to pay off debt collectors. So your heirs may be left with something. (source)

Sometimes people get life insurance to help their loved ones (often co-signers) with the debt they leave behind. Since life insurance is exempt from some estates, it can be used by your heirs and loved ones with the burden of any debt you accumulated together.

Conclusion

In short, your debt belongs only to you, it is not passed on to your family when you pass. (source). As long as you didn’t have any co-signers for your Student Loans/Credit Card Loans and your estate can’t pay them, those debts die with you. Home Loans and Car Loans are tangible assets that can be taken back if not paid off or have someone take over the payments in order to keep them.

If this research taught me anything, it’s to be very aware of what I co-sign. Debt dies with the deceased, unless there’s a co-signer.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

Warren Buffett, CEO of Berkshire Hathaway, has a net worth of over $78.2 billion and is known as one of the greatest investors of all time. So when he speaks, people take note.

Here are some of the top 22 Warren Buffett Quotes the internet can’t get enough of.

Top 22 Warren Buffett Quotes The Internet Can’t Get Enough Of

Here are some of the top Warren Buffet quotes found on every list of Warren Buffet quotes around the internet. These quotes range in wisdom on investing to regular life. I try to live by these quotes on my own investment portfolio.

Warren Buffett Quotes

1. Rule #1: Never lose money. Rule #2: Never forget rule #1

One of my favorite Warren Buffet Quotes. The fastest way to grow your money is to never lose it in the first place. This applies from saving on your groceries to focusing on less risky stocks of well established companies.

2. It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you’ll do things differently

Think about the Wells Fargo or Equifax scandals. It takes years to build enough trust for someone to have brand loyalty. Warren Buffet quotes it takes 20 years, but it takes 5 minutes or less to destroy all that goodwill you’ve built. People are quick to revolt if you’ve done anything to betray their trust.

It is infinitely harder to build trust than destroy it.

3. Diversification is a protection against ignorance. It makes very little sense for those who know what they’re doing.

Multiple studies show that diversification in the stock market will help protect you against market falls. Or it could be summarized in the old proverb “Don’t put all your eggs in one basket”. Unless you have insider information that a stock is going do really well, maintain a diversified portfolio to protect you. No one knows what they’re doing all the time.

4. If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes. Put together a portfolio of companies whose aggregate earnings march upward over the years, and so also will the portfolio’s market value.

Unless you’re a day trader (I will never be), you should only be investing in the stock market with the intention to hold those stocks for a long time. You can do really well as a beginner if you’re buying stocks and not planning on selling till you retire. Those are where you get the best returns. Warren Buffett is infamously known for rarely selling stocks.

5. It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

When you buy a stock, you should think of it as owning a piece of that company. You should be looking at wonderful companies that have a competitive advantage in the industry. Those are the companies that will do well over the long run. You may find a wonderful price on a mediocre company, but really what are you getting? A mediocre company that will likely be edged out of the market by a better company.

Many of the famous Warren Buffett quotes are about investing in strong companies with a competitive advantage and strong brand loyalty rather than cheap companies where you think you can make a quick buck. Warren Buffett is never into buying a company for a quick buck.

6. Be fearful when others are greedy. Be greedy when others are fearful.

During the 2008 financial crisis when investors were all exiting the market, Warren Buffett invested in a few large companies even though their stock prices were falling. Those deals made Warren Buffett over $10 billion dollars when the market stabilized and it’s continuing to show dividends. When the market goes upside down during world events, politics, market forecasts, those are the times when everyone else is fearful, that Warren Buffet sees an advantage when the markets crash.

Think about it this way, the New York Stock Exchange has been around since 1817, it has always recovered. Chances are, minus a world apocalypse, that the market will always bounce back. Those who capitalize on those downturns are usually rewarded.

7. The difference between successful people and really successful people is that really successful people say no to almost everything.

One of my favorite Warren Buffett quotes because it has so many applications. You will see many opportunities in your life and you may want to jump on everyone, but it’s ok to be selective and say no. You’ll burn yourself out if you say “yes” to everything. This also applies to going out on a Saturday night with friends drinking. It’s ok to say “no” to save a few dollars or have a night to yourself to finish your article on Warren Buffett quotes. =)

This also applies to going out on a Saturday night with friends drinking. It’s ok to say “no” to save a few dollars or have a night to yourself to finish your article on Warren Buffett quotes. =)

8. Develop and build the habits you admire in others.

Remember all those times that your parents wanted you to hang out with those “good kids”. The habits of the people you surround yourself with rub off you on, consciously or unconsciously. When you find people like Warren Buffett, the Oracle of Omaha, who is one of the greatest investors of all time. You should find out what makes him so successful and learn those traits to improve yourself.

9. Passive investing will make you more money than active trading

Oh my goodness, fees are the WORST! Active trading requires more work and more fees, so more of your money will be paid to your broker. Yet studies have shown over and over that passive investing where you set your money and forget it are far more successful for growing wealth. I don’t plan to ever touch my stocks currently making dividends.

10. There seems to be some perverse human characteristic that likes to make easy things difficult.

Great quote, people always imagine things are more difficult than they really are. When I first considered starting investing, I thought there were so many hurdles and financial experts I would have to pay. Yet, when I finally decided I wanted to start investing in the stock market, I just downloaded the Robinhood App and started investing. It took 10 minutes to sign up and buy my first stock when I worried about investing in the stock market for over 5 years. Things are often more simple than you think they are.

11. Tell me who your heroes are and I’ll tell you who you’ll turn out to be.

This is similar to the Warren Buffett quote “Develop and build the habits you admire in others”. If you want to be an entrepreneur, start joining local meetups of entrepreneurs. You learn SO MUCH MORE when you surround yourself with the people you want to be like. You can learn A LOT in a book, but you’ll learn even more by surrounding yourself with people you admire.

12. We have long felt that the only value of stock forecasters is to make fortune-tellers look good.

No one can predict the stock market, no one. Not even Warren Buffett. Anyone who says they know exactly how the market works is trying to sell you something. You can lump stock forecasters being as accurate as the carnival fortune-tellers. You know the ones with 3 teeth, crystal ball and you’re going to die in 2083.

13. When we own portions of outstanding businesses with outstanding managements, our favorite holding period is forever.

If you invest in an outstanding company, even if the stock price goes up, why would you ever sell it? No matter when you sell it, outstanding companies will continually do better and better. Don’t sell until you absolutely have to, otherwise, you’ll just be losing money in the long run. Many of Warren Buffett Quotes are like this, they are all very Anti-Day Trader.

14. You don’t need to be a rocket scientist. Investing is not a game where the guy with the 160 IQ beats the guy with 130 IQ.

If you follow the basic principals of Warren Buffett and buy outstanding companies with strong competitive advantages like Apple (AAPL). You don’t have to be a genius. Just buy and hold forever, you literally don’t have to do anything until you sell.

Many Warren Buffett quotes are similar to this because he stresses that anyone can invest in the stock market. The simplest way is just to invest in index funds that follow the market. Set it and forget it. The market sees an average increase of 7% per year and that’s WAY better than a savings account.

15. I try to buy stock in businesses that are so wonderful that an idiot can run them. Because sooner or later, one will.

Look for companies to invest in that are so strong that they can weather any storm because soon enough they will have to. Think about Apple (AAPL), as long as they keep pushing out iPhones it doesn’t matter who runs the company, they’ll continue to do well. People were worried when Steve Jobs passed because they didn’t know the future of the company, but Tim Cook stepped in and maintained the same Apple legacy. As long as Tim Cook sticks to the secret Apple recipe, they’ll be in good shape.

16. Buy into a company because you want to own it, not because you want the stock to go up.

If you see a company that you think is going to do well or heard will do well, don’t buy it unless you’re willing to hold it for awhile. If something goes wrong and the stock dives, you’re stuck with a company you don’t believe in and will likely sell at a lower price to get rid of it, ruining the reason you bought it in the first place.

17. Wall Street is the only place that people ride to work in a Rolls Royce to get advice from those who take the subway.

This is just a funny Warren Buffet quote.

18. Charlie and I have not learned how to solve difficult business problems. What we have learned is to avoid them.

I’m sure Warren Buffett and Charlie Munger have learned how to solve difficult business problems, but the best way to navigate murky waters is to avoid them all together. The more problems your business can avoid, the better shape you’ll be. You can avoid a lot of problems from being proactive instead of reactive.

19. Long ago, Ben Graham taught me that “Price is what you pay; value is what you get.”

Ben Graham, Warren Buffett’s mentor had this popular quote. I always think about it simply. Price is what you buy a stock for and Value is what you sell that same stock for.

20. It’s better to hang out with people better than you. Pick out associates whose behavior is better than yours and you’ll drift in that direction.

If you can’t tell, Warren Buffett believes in surrounding yourself with the right people. He credits much of his success from surrounding himself with smart, good people.

21. If past history was all there was to the game, the richest people would be librarians.

When you analyze a stock based on its historical performance, it’s called technical analysis. Yet past performance does not necessarily mean future performance. Just because you know what the stock has done in the past doesn’t mean it’s going to follow that same trend.

22. You only have to do a very few things right in your life so long as you don’t do too many things wrong.

It’s ok to mess up, focus on learning from those mistakes for the next time. It just sounds cooler when Warren Buffett quotes it. Or you can take this as no matter how many mistakes you’ve made in the past, you always have a chance to do more good. It’s one of those life quotes that can go many ways.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!

That means the average person spends $54.63 eating out a week or $218.52 a month on just eating out. Unless you have a side-hustle that makes you lots of money. The obvious answer is to eat in!

What About Eating In?

Most people think they can easily quit dining out, and start cooking delicious meals. Here’s the thing with cooking for yourself, the movies get it wrong.

It’s not always a romantic and soothing experience.

Often times it’s a “Crap, I need to eat. What should I cook?” experience that you pray to the food gods you have the right ingredients in your fridge and clean dishes.

Let’s face it, we are busy in our lives and don’t have the time to visit the store every day buying fresh ingredients for a new recipe we found on the internet.

In fact, according to the Harvard Business Review, researcher Eddie Yoon over two decades collected data as consultants for consumer packaged goods companies. He found that:

15% of people say they LOVE to cook

50% of people say they HATE to cook

35% of people say they are ambivalent about cooking (mixed feelings)

If you’re one of the people that hate cooking, you should create a meal plan to make it as easy as possible.

Plan a week in advance what you’re going to eat for each meal and know how to cook it. This way you’ll have the ingredients and can plan accordingly for time.

However, not all plans work out.

Introduce The Peanut Butter and Jelly Theory

When meal plans fail, let me introduce Peanut Butter and Jelly sandwiches, otherwise known as a PBJ.

Let me first admit that I have an addiction to commenting on Finance forums, Facebook Groups, and Blogs. The mechanics of building wealth are simple and I’m always happy to remind people that things are often more simple than they appear. Like how I responded to this comment and created “The Peanut Butter and Jelly Theory”.

I get it, you want to start saving money on food and you’re looking for suggestions from the personal finance community to help.

Answers ranged from getting a crockpot to make meals simple, cooking large meals on Sunday and eating leftovers throughout the week, to buying frozen meals that may not be great for you, but easy to prepare.

All of the responses skirted around the idea that a solid weekly meal plan is the best option to help you save money on food. However, sometimes these meals don’t work out for a number of reasons, and once you fall off the wagon, you can end up at the local McDonalds.

So I introduced the Peanut Butter and Jelly Theory. The cost-effective, quickest meal ever to keep your budget on track.

This is easily the most actionable thing you can do to start immediately saving on your food budget. In many cases when people eat out, it’s due to convenience because they don’t have anything at home to sound appealing. That’s when the Peanut Butter and Jelly Theory comes in handy.

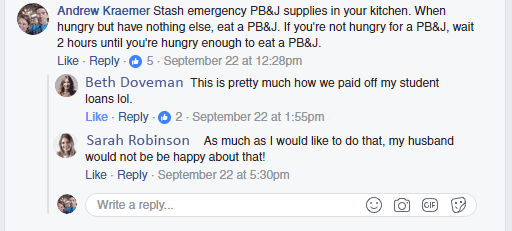

“Stash emergency PBJ&J supplies in your kitchen. When hungry, but have nothing else. You can have a PBJ. If you’re not hungry for a PB&J, wait 2 hours until you’re hungry enough to eat a PB&J.”

Sometimes a PBJ isn’t exactly what you’re craving and your favorite restaurant sounds better, or your family would not be happy about that. Well suck it up, you’ll soon be out of debt and you can buy your family a jet ski. Everyone loves a jet ski.

Try the Peanut Butter and Jelly Theory

If you want to save THOUSANDS on food budgets, you should try the Peanut Butter and Jelly Theory! Meals cost less than $1 to make, you’ll save time and money. Most importantly, you’ll have a secret stash of PBJs to make and everyone is a stack of cash saved from eating out!

You’re welcome.

Disclaimer: Wallet Squirrel did not invent the Peanut Butter and Jelly sandwich, just an advocate of saving money. Wallet Squirrel was not sponsored by big PBJ corporations to promote their superior and delicious product.

Wallet Squirrel is a personal finance blog by best friends Andrew & Adam on how money works, building side-hustles, and the benefits of cleverly investing the profits. Featured on MSN Money, AOL Finance, and more!